Global Market Comments

November 19, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

(SPY), (WMT), (NVDA), (EEM), (FCX), (AMZN), (AAPL), (FCX), (USO), (TLT), (TSLA), (CRM), (SQ)

Global Market Comments

November 19, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

(SPY), (WMT), (NVDA), (EEM), (FCX), (AMZN), (AAPL), (FCX), (USO), (TLT), (TSLA), (CRM), (SQ)

I will be evacuating the City of San Francisco upon the completion of this newsletter.

The smoke from the wildfires has rendered the air here so thick that it has become unbreathable. It reminds me of the smog in Los Angeles I endured during the 1960s before all the environmental regulation kicked in. All Bay Area schools are now closed and anyone who gets out of town will do so.

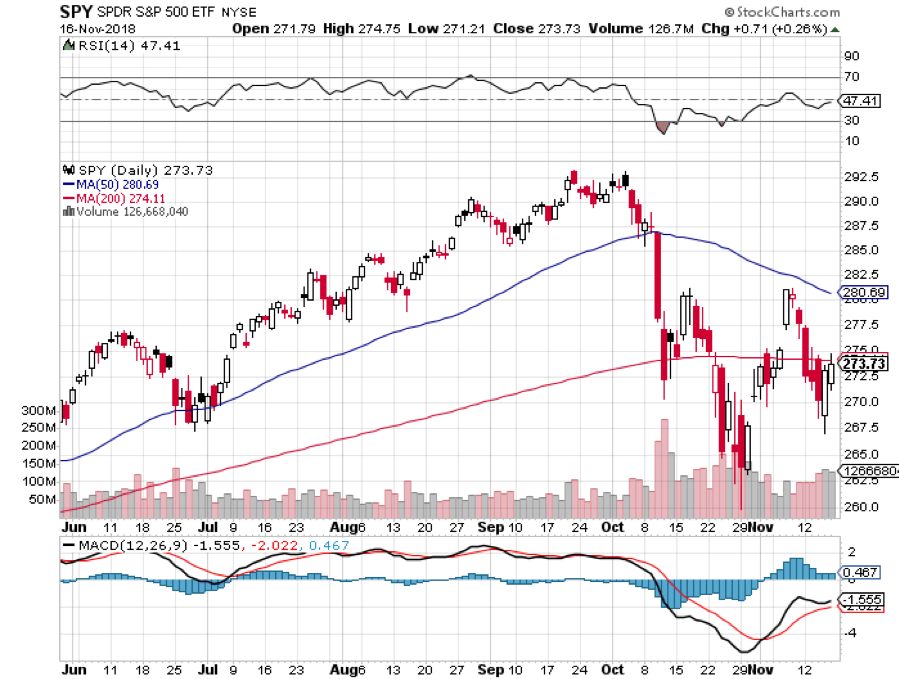

There has been a mass evacuation going on of a different sort and that has been investors fleeing the stock market. Twice last week we saw major swoons, one for 900 points and another for 600. Look at your daily bar chart for the year and the bars are tiny until October when they suddenly become huge. It’s really quite impressive.

Concerns for stocks are mounting everywhere. Big chunks of the economy are already in recession, including autos, real estate, semiconductors, agricultural, and banking. The FANGs provided the sole support in the market….until they didn’t. Most are down 30% from their tops, or more.

In fact, the charts show that we may have forged an inverse head and shoulders for the (SPY) last week, presaging greater gains in the weeks ahead.

The timeframe for the post-midterm election yearend rally is getting shorter by the day. What’s the worst case scenario? That we get a sideways range trade instead which, by the way, we are perfectly positioned to capture with our model trading portfolio.

There are a lot of hopes hanging on the November 29 G-20 Summit which could hatch a surprise China trade deal when the leaders of the two great countries meet. Daily leaks are hitting the markets that something might be in the works. In the old days, I used to attend every one of these until they got boring.

You’ll know when a deal is about to get done with China when hardline trade advisor Peter Navarro suddenly and out of the blue gets fired. That would be worth 1,000 Dow points alone.

It was a week when the good were punished and the bad were taken out and shot. Wal-Mart (WMT) saw a 4% hickey after a fabulous earnings report. NVIDIA (NVDA) was drawn and quartered with a 20% plunge after they disappointed only slightly because their crypto mining business fell off, thanks to the Bitcoin crash.

Apple (AAPL) fell $39 from its October highs, on a report that demand for facial recognition chips is fading, evaporating $170 billion in market capitalization. Some technology stocks have fallen so much they already have the next recession baked in the price. That makes them a steal at present levels for long term players.

The US dollar surged to an 18-month high. Look for more gains with interest rates hikes continuing unabated. Avoid emerging markets (EEM) and commodities (FCX) like the plague.

After a two-year search, Amazon (AMZN) picked New York and Virginia for HQ 2 and 3 in a prelude to the breakup of the once trillion-dollar company. The stock held up well in the wake of another administration antitrust attack.

Oil crashed too, hitting a lowly $55 a barrel, on oversupply concerns. What else would you expect with China slowing down, the world’s largest marginal new buyer of Texas tea? Are all these crashes telling us we are already in a recession or is it just the Fed’s shrinkage of the money supply?

The British government seemed on the verge of collapse over a Brexit battle taking the stuffing out of the pound. A new election could be imminent. I never thought Brexit would happen. It would mean Britain committing economic suicide.

US Retails Sales soared in October, up a red hot 0.8% versus 0.5% expected, proving that the main economy remains strong. Don’t tell the stock market or oil which think we are already in recession.

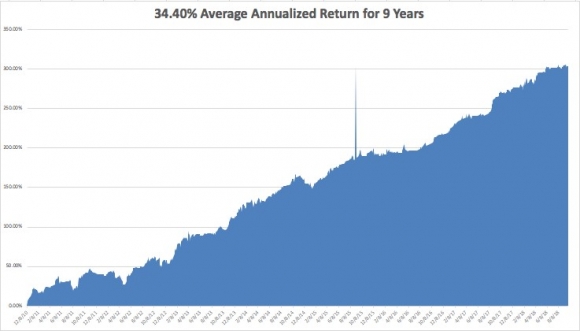

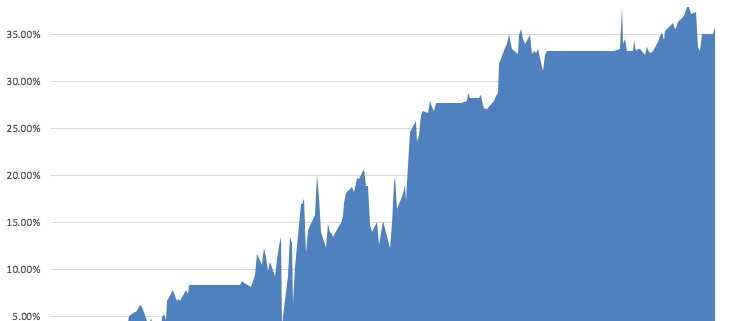

My year-to-date performance rocketed to a new all-time high of +33.71%, and my trailing one-year return stands at 35.89%. November so far stands at +4.08%. And this is against a Dow Average that is up a miniscule 2.41% so far in 2018.

My nine-year return ballooned to 310.18%. The average annualized return stands at 34.46%. 2018 is turning into a perfect trading year for me, as I’m sure it is for you.

I used every stock market meltdown to add aggressively to my December long positions, betting that share prices go up, sideways, or down small by then.

The new names I picked up this week include Amazon (AMZN), Apple (AAPL), Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and a short position in Tesla (TSLA). I also doubled up my short position in the United States US Treasury Bond Fund (TLT).

I caught the absolute bottom after the October meltdown. Will lightning strike twice in the same place? One can only hope. One hedge fund friend said I was up so much this year it would be stupid NOT to bet big now.

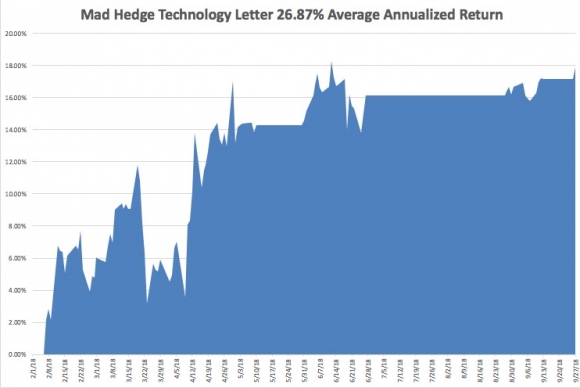

The Mad Hedge Technology Letter is really shooting the lights out the month, up 8.63%. It picked up Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and Apple (AAPL) last week, all right at market bottoms.

The coming week will be all about October housing data which everyone is expecting to be weak.

Monday, November 19 at 10:00 EST, the Home Builders Index will be out. Will the rot continue? I’ll be condo shopping in Reno this weekend to see how much of the next recession is already priced in.

On Tuesday, November 20 at 8:30 AM, October Housing Starts and Building Permits are released.

On Wednesday, November 21 at 10:00 AM, October Existing Home Sales are published.

At 10:30 AM, the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 22, all market will be closed for Thanksgiving Day.

On Friday, November 23, the stock market will be open only for a half day, closing at 1:00 PM EST. Second string trading will be desultory, and low volume.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I'd be roaming the High Sierras along the Eastern shore of Lake Tahoe looking for a couple of good Christmas trees to chop down. I have two US Forest Service permits in hand at $10 each, so everything will be legit.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 24, 2018

Fiat Lux

Featured Trade:

(HERE'S AN EASY WAY TO PLAY ARTIFICIAL INTELLIGENCE),

(BOTZ), (NVDA), (ISRG)

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California's largest export (it's not grapes). But such a fund DOES exist.

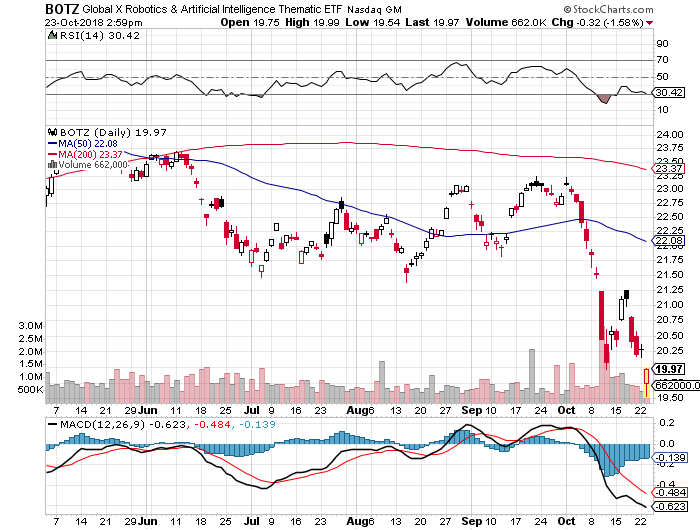

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a gilt-edged opportunity into investors' laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.2 billion in assets under management.

The universal trend of preferring automation over human labor is mushrooming with each passing day. Suffice to say there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don't complain, don't fall ill, don't join unions, or don't ask for pay rises. It's all very much a capitalist's dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it's not online dating, gambling, or bitcoin, it's Artificial Intelligence.

Selecting individual stocks that are purely exposed to AI is a challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure AI plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated AI play out there. A real diamond in the rough.

The best way to expose yourself to this AI trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit on the forefront of the AI and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and AI walk hand in hand, and robotics are entirely dependent on the germination prospects of AI. Without AI, robots are just a clunk of heavy metal.

Robots require a high level of AI to meld seamlessly into our workforce. The stronger the AI functions, the stronger the robot's ability, filtering down to the bottom line.

AI-embedded robots are especially prevalent in the defense industry, automobile manufacturing, and heavy industrial machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotic industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let's get the ball rolling and familiarize readers of the Mad Hedge Technology Letter with the most influential weightings in the underlying ETF (BOTZ).

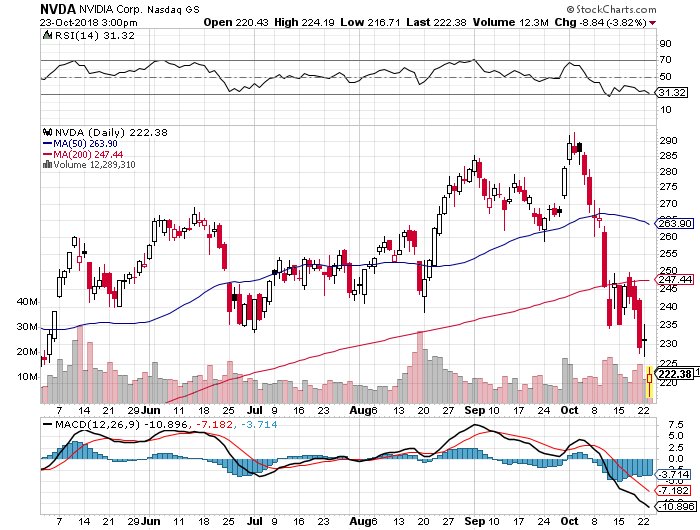

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California based company is spearheading the next wave of AI advancement by focusing on autonomous vehicle technology and AI-integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state of the art IOT products (internet of things), fueled by GPU chips, coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese-American who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Nvidia constitutes a hefty 6.60% of the BOTZ ETF.

To visit their website please click here.

Yaskawa Electric (Japan)

Yaskawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improving global productivity through Automation. Yaskawa was recently switched out of the index in favor of an American newcomer John Bean Technologies specializing in the food processing and air transportation industries. Nevertheless, Yaskawa is still a company to have on your radar screen.

To visit Yaskawa's website, please click here.

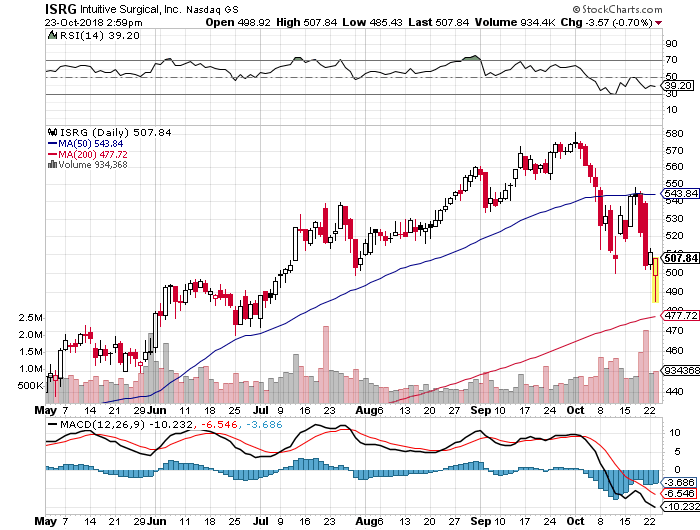

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is industriously focused on the medical industry.

The company's da Vinci Surgical System converts the surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3-D vision systems, da Vinci skills simulators, and da Vinci Xi integrated table motions.

This company comprises 7.71% of BOTZ. To visit their website, please click here.

Fanuc Corp. (Japan)

Fanuc was another one of the hit robotics companies I used to trade in during the 1970s and I have visited their main factory many times.

The 4thlargest portion in the (BOTZ) ETF at 6.11% is Fanuc Corp. This company provides automation products and computer numerical control systems, headquartered in Oshino, Yamanashi.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscopes.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-opening 50% operating margin.

They are headquartered in Osaka, Japan and make up 6.10% of the BOTZ ETF.

To visit their website please click here.

(BOTZ) does has some pros and cons. The best AI plays are either still private at the venture capital level taken over by the SoftBank Vision Fund wielding its war chest of $100 billion or a Silicon Valley mainstay such as Andreessen Horowitz.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many for the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don't own their own robotic led business, pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ) please visit their website by clicking here.

Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

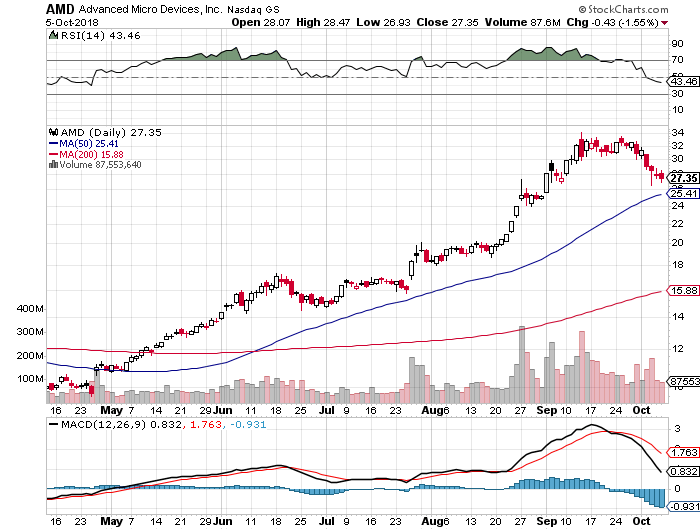

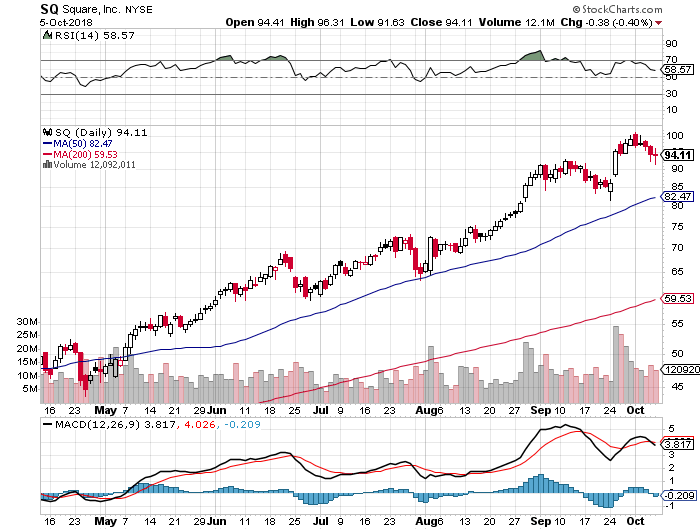

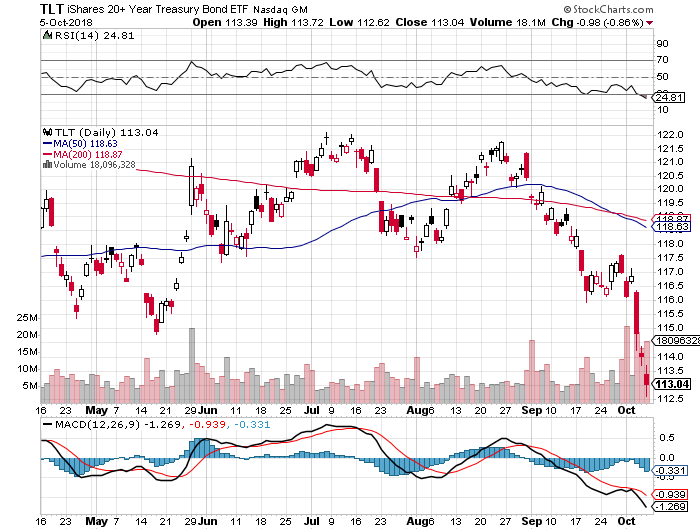

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

Taking profits - it was finally time.

The Nasdaq has been hit in the mouth the last few days and rightly so.

It was the best quarter in equities for five years, and a quarter that saw tech comprise up to a quarter of the S&P demonstrating searing strength.

It would be an understatement to say that tech did its part to drive stocks higher.

Tech shares have pretty much gone up in a straight line this year aside from the February meltdown.

Even that blip only caused Amazon (AMZN) to slide around 10%.

After all the terrible macro news thrown on the market in spades – tech stocks held their own.

Not even a global trade war with the second biggest economy in the world which is critical to exporting products to America was able to knock tech shares off their perch.

At some point, 26% earnings growth cannot sustain itself, and even though the tech narrative is still intact, investors need to breathe.

Let’s get this straight – tech companies are doing great.

They benefit from a secular tailwind with every business pivoting to mobile and software services.

All that new business has infused and invigorated total revenue.

The negative reaction by technology stocks was based on two pieces of news.

Interest rates (TLT) surging to over 3.2% was the first piece of news.

The increase in rates reinforces that the economy is humming along at a breakneck speed.

Yields are going up for the right reasons and this economy is not a sick one indeed.

As rates rise, other asset classes become more attractive such as CD’s and bonds.

The whole world is looking at the pace of rate rises because this will affect the ability for tech behemoths to borrow money to invest in their expensive well-oiled machines.

Three things are certain - the economy is hot, the smart money is buying on the dip now, and Amazon will still take over your home.

Even in a rising rate environment, Amazon is fully positioned to outperform.

The second catalyst to this correction was Amazon’s decision to hike its minimum wage to $15 per hour.

This could lay the path for workers around the country to demand higher pay.

The move was a misnomer as it will eliminate stock awards and monthly bonuses lessening the burden that Amazon actually has to dole out.

Call this a push – the rise in expenses won’t be material and realistically, Amazon can afford to push the wage bill by another order of magnitude, even though they will not.

This was also a way for Amazon founder Jeff Bezos to keep Washington off his back for a few months, and his generous decision was praised by government officials.

The wage hike underscores the strength of the ebullient American economy, and the consumer will benefit by recycling their wages back into Amazon and the wider economy.

Amazon makes up 50% of American e-commerce sales, and when workers are buying goods online, a good chance its coming from Amazon.

In an environment of full employment, the natural direction of wages is up, and this was due to happen.

You can also look at wage inflation as employees gaining at the expense of the corporation.

However, the massive deflationary trends of technology will also make this wage hike quite irrelevant over time as Amazon will automate more of their supply chain to make up for any wage hike that could damage revenue.

Amazon’s economies of scale give the Seattle-based company enough levers and buttons to push and pull to dilute expenses to make this a non-issue.

Each earnings call usually involves CFO of Amazon Brian Olsavsky explaining the acceleration of efficiencies in fulfilment centers bolstering the bottom line.

The stellar innovation in operational expertise moves up a level each quarter if not two levels.

Ultimately, though expensive on the surface, this won’t affect Amazon’s numbers at all, but more critically please the lower tier of workers who fight and scratch for their daily crust of bread.

This win-win scenario casts a positive image of Bezos in the public eye at a crucial time when he plans to recruit another legion of Amazon workers, as Amazon will shortly announce the location of their second American-based headquarter.

In fact, this turns the screws on the smaller retailers who must match the $15 per hour wage or confront a potential disaster of an entire workforce walking out and joining Amazon.

The mysterious Amazon-effect works in many shapes and sizes.

Big retailers like Target (TGT) have griped that it’s near impossible to find seasonal workers for the upcoming holiday season.

Moreover, if inflation remains moderate but contained – technology will power on.

And it will take more than a few prints of rising inflation to impress the Fed enough to expedite the raising of rates.

But it is safe to say that investors cannot expect the 100% up moves like in Amazon and Advanced Micro Devices (AMD) in one calendar year moving forward.

Technology has a plate full of challenges facing its share price as we move into the latter part of the fiscal year.

The challenges are two-fold - mid-term elections and navigating a smooth year-end.

Earnings should be good which is already baked into the pie, and the benefits of the tax cut have already worked itself through the system.

The furious pace of share buybacks will eventually subside too.

Management might finally bring out the spin doctors claiming the stronger dollar and worsening trade war is the reason to guide down.

At least tech companies doing business in China might follow this playbook.

Either way, tech shares are demonstrably sensitive right now and while the market needs tech to lead the way, the sector is exhausted from the burden of carrying the bulk of the load.

Freak-outs on rate surges have been a common experience for those old hands presiding over markets for decades.

These are all the staples of a 9th year bull market.

Typical late stage topping action is normal in economic cycles.

After the dust settles, the overreaction will give way to great buying opportunities at great prices, albeit it in the higher quality names.

The chip sector is still one to avoid unless the names are Advanced Micro Devices or Nvidia (NVDA).

Legacy companies have always been a no-go.

If you want hyper-growth, fin-tech name Square (SQ) would be an ideal candidate.

If buy and hold is your cup of tea, any 10% discount would be a great entry point in any of these quality companies.

Global Market Comments

October 5, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Will the market keep increasing for the rest of the year?

A: We haven’t had the pullback yet, so the short answer is yes. My yearend target of and S&P 500 (SPY) for the end of 2018 still stands. You can’t argue with the immediate price action. That said, the market is wildly overbought for the medium term and is approaching valuation levels we haven’t seen since the Dotcom peak in 2000. That why I am running a 70% cash trading book now.

Q: Should I be buying the Volatility Index (VIX) here?

A: Look at the bottom where we broke back in August, if we go down there and sit for a couple of days, then go out and buy the March 2019 $40 iPath S&P 500 VIX Short-Term Futures ETN (VXX) calls—way out of the money, way far in the future—and that way if you get any bounce in the (VIX) in the next 6 months, you’ll make a ton of money on that. You can buy them today for 50 cents. Plus, we could get one of these situations where there’s a major selloff once we’re into the new year, so a 6-month (VXX) call option would hedge that.

Q: Given the choice of Apple (AAPL) or Google (GOOG), which would you buy?

A: If you’re a conservative, old lady, widow and orphan type, you’d probably want to buy Apple— it’s almost turned into a utility, it’s so reliably safe, going up and has a nice dividend. If you want to be aggressive, swinging for the fences young stud and are looking for a double, I would go with Google—much higher growth pattern, pays no dividend and has had a 3-month consolidation going sideways. The only thing that could hurt this company would be government regulation, but with the Democrats possibly taking control of Congress in November, the prospect of government regulation of the entire technology sector could rapidly fade away.

Q: When should I get into Health Care (XLV)?

A: I think you have to wait at this point. To me, it’s tremendously overbought at the moment, but is still enjoying a long-term bull move. This is one of my two favorite sectors in the entire market. It has been rising for four months now, even though the Trump threat of price cuts are constantly overhanging the market.

Q: Is oil (USO) going to 100?

A: Because of the disruptions caused by the Iran sanctions and the tearing up of the Iran Nuclear Treaty, Trump has created a short squeeze in oil prices. He is threatening to boycott any country that buys oil from Iran, so Iran is shipping their oil through China, which is already under sanctions itself. However, that is easier said than done. The oil business is much more complicated than people realize. For China to take Iranian oil, they literally have to build new refineries from scratch to process the crude from Iran; no two crudes are alike. When you build a major supply, you have to build refineries to match that, and you have to get it there. This market will eventually stabilize, but in the meantime, there is a big short squeeze going on in Europe.

Q: Do you see the economy going strong into the end of the year?

A: Yes, I do—we still have the tax cuts, global liquidity, and deregulation kicking in, and those things will all work until the end of the year. I think we close at the highs of the year, and after that we’re going to have to start to work hard for our money once again in 2019. The US economy is like a supertanker; it takes a long time to turn it around.

Q: Will the interest rate spike kill the market?

You think? Investors are so used to ultra-low interest rates that a transition to normal rates will be traumatic. Next Friday, we get Core CPI, and if that comes in hot we could see another spike to 3.35% in the ten-year US Treasury bond (TLT). There are now a ton of people desperate to get out of their bond holdings at last week’s prices. This is why I have been selling short the bond market for the past three years and selling as recently as Monday. The next leg down in a 30-year bear market has begun.

Q: Advanced Micro Devices (AMD) has shot over $30—would you sell it?

A: We love the company long term but short term it is just way overdone; take the double and run, and then buy back on the next dip.

Q: Are you still bearish on the chip company?

A: Short term yes, long term no. This sector is now totally driven by the trade war with China. This includes NVIDIA (NVDA), Micron Technology (MU) and LAM Research (LRCX). Lam is particularly exposed because they had ordered to sell ten entire chip factories to China which is now on hold. That said, the day the trade way ends these stocks will all start a 50% run up. If China gets the same free pass and symbolic treaty that Canada did, that could happen sooner than later. If you can’t sleep at night until then, cut your position in half. If you still can’t sleep, cut it again.

Q: Do you think Lockheed Martin (LMT) is a buy Here at $350?

A: No, there is a double top risk for the stock right here. And if the Democrats get control of congress, the whole Trump trade could unwind. That would give the opposition the purse strings and the first thing they’ll do is cut defense spending, which Trump bumped up by $50 billion.

Q: Do you have any views on pot stocks like Aurora Cannabis (ACB), Tilray (TLRY) and (WEED)?

Stay away in droves. They’re this year’s bitcoin stocks. It’s still illegal. That’s why these companies are all based in Canada. And after all it’s a weed. How hard is it to grow? The barriers to entry are zero.

Global Market Comments

October 1, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD,

or DON’T NOMINATE ME!),

(AMZN), (NVDA), (AAPL), (MSFT), (GLD), (ABX), (GOLD),

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA,

CONFERENCE, OCTOBER 26-27, 2018)

I have a request for all of you readers. Please do not nominate me for justice of the Supreme Court.

I have no doubt that I could handle the legal load. A $17 copy of Litigation for Dummies from Amazon would take care of that.

I just don’t think I could get through the approval process. There isn’t a room on Capitol Hill big enough to house all the people who have issues with my high school background.

In 1968, I ran away from home, hitchhiked across the Sahara Desert, was captured by the Russian Army when they invaded Czechoslovakia, and had my front teeth knocked out by a flying cobblestone during a riot in Paris. I pray what went on in Sweden never sees the light of day.

So, I’m afraid you’ll have to look elsewhere to fill a seat in the highest court in the land. Good luck with that.

The most conspicuous market action of the week took place when several broker upgrades of major technology stocks. Amazon (AMZN) was targeted for $2,525, NVIDIA (NVDA) was valued at $400, and JP Morgan, always late to the game (it’s the second mouse that gets the cheese), predicted Apple (AAPL) would hit a lofty $270.

That would make Steve Jobs’ creation worth an eye-popping $1.3 trillion.

The Mad Hedge Market Timing Index dove down to a two-month low at 46. That was enough to prompt me to jump back into the market with a few cautious longs in Amazon and Microsoft (MSFT). The fourth quarter is now upon us and the chase for performance is on. Big, safe tech stocks could well rally well into 2019.

Facebook (FB) announced a major security breach affecting 50 million accounts and the shares tanked by $5. That prompted some to recommend a name change to “Faceplant.”

The economic data is definitely moving from universally strong to mixed, with auto and home sales falling off a cliff. Those are big chunks of the economy that are missing in action. If you’re looking for another reason to lose sleep, oil prices hit a four-year high, topping $80 in Europe.

The trade wars are taking specific bites out of sections of the economy, helping some and damaging others. Expect to pay a lot more for Christmas, and farmers are going to end up with a handful of rotten soybeans in their stockings.

Barrick Gold (ABX) took over Randgold (GOLD) to create the world’s largest gold company. Such activity usually marks long-term bottoms, which has me looking at call spreads in the barbarous relic once again.

With inflation just over the horizon and commodities in general coming out of a six-year bear market, that may not be such a bad idea. Copper (FCX) saw its biggest up day in two years.

The midterms are mercifully only 29 trading days away, and their removal opens the way for a major rally in stocks. It makes no difference who wins. The mere elimination of the uncertainty is worth at least 10% in stock appreciation over the next year.

At this point, the most likely outcome is a gridlocked Congress, with the Republicans holding only two of California’s 52 House seats. And stock markets absolutely LOVE a gridlocked Congress.

Also helping is that company share buybacks are booming, hitting $189 billion in Q2, up 60% YOY, the most in history. At this rate the stock market will completely disappear in 20 years.

On Wednesday, we got our long-expected 25 basis-point interest rate rise from the Federal Reserve. Three more Fed rate hikes are promised in 2019, after a coming December hike, which will take overnight rates up to 3.00% to 3.25%. Wealth is about to transfer from borrowers to savers in a major way.

The performance of the Mad Hedge Fund Trader Alert Service eked out a 0.81% return in the final days of September. My 2018 year-to-date performance has retreated to 27.82%, and my trailing one-year return stands at 35.84%.

My nine-year return appreciated to 304.29%. The average annualized return stands at 34.40%. I hope you all feel like you’re getting your money’s worth.

This coming week will bring the jobspalooza on the data front.

On Monday, October 1, at 9:45 AM, we learn the August PMI Manufacturing Survey.

On Tuesday, October 2, nothing of note takes place.

On Wednesday October 3 at 8:15 AM, the first of the big three jobs numbers is out with the ADP Employment Report of private sector hiring. At 10:00 AM, the August PMI Services is published.

Thursday, October 4 leads with the Weekly Jobless Claims at 8:30 AM EST, which rose 13,000 last week to 214,000. At 10:00 AM, September Factory Orders is released.

On Friday, October 5, at 8:30 AM, we learn the September Nonfarm Payroll Report. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, it’s fire season now, and that can only mean one thing: 1,000 goats have appeared in my front yard.

The country hires them every year to eat the wild grass on the hillside leading up to my house. Five days later there is no grass left, but a mountain of goat poop and a much lesser chance that a wildfire will burn down my house.

Ah, the pleasures of owning a home in California!

Good luck and good trading.