Thanks to COVID-19, a new generation of biotechnology players are gaining more traction in the market these days.

For decades, the biotech industry has been notoriously difficult to break into.

However, the pandemic has served to level the playing field—and the small-cap biotechs are definitely taking advantage of the opening.

The latest to cash in on the opportunity is Ocugen (OCGN).

Founded in 2013, this Pennsylvania-based biotechnology company attracted media attention when it announced its partnership with India’s Bharat Biotech earlier this month.

The agreement between the two companies centered on Bharat’s COVID-19 vaccine candidate, Covaxin, which Ocugen plans to bring to the United States as soon as possible.

Ocugen will hold the US rights to Covaxin and be in charge of the development, regulation, and even commercialization within that market.

Even without any upfront payment, Ocugen will get 45% of the profits from the US markets in return.

While the news only broke this year, the partnership between the two has been months in the making, with Ocugen reaching a tipping point in December 2020 when it recorded a jaw-dropping 800% rise.

When this deal was announced, Ocugen shares were projected to rise from $4.50 to $8, showing off an already impressive increase from its measly 29 cents valuation less than a year ago.

Ocugen blew past those projections though as it’s now trading at $15 per share.

The kicker? The stock still has room to grow.

Realistically speaking, Ocugen shares can reach $20 to $25 after FDA approval this year. If its other candidates in the pipeline work out, then we can even see it hit $50 at some point.

Considering that Ocugen was able to sell 3 million common shares at a price that’s 46% higher than where the stock was when it closed last Friday, it’s clear that there’s a lot of optimism on the company these days.

The next question is this: Will Covaxin even gain approval in the US?

It can.

If it’s any indication, Covaxin has already been granted emergency use authorization in India.

Moreover, Covaxin was developed by Bharat, which is a highly reputable biotechnology company in India with 25 years of experience in the vaccine-making industry.

In fact, Bharat has developed over 16 vaccines and four bio-therapeutics, so it’s safe to say that the company knows its way around the business.

More than that, Bharat is confident that Covaxin can be effective against the new UK and South African variants of the coronavirus, making this vaccine candidate more potent than the other products under development today.

Unlike the vaccines of Pfizer (PFE) and Moderna (MRNA), Covaxin does not need ultra-cold freezers for storage. It can simply be stored at room temperature, making it a convenient option for a lot of distributors.

Prior to its deal with Bharat, Ocugen has been focused on its gene therapy which carries the potential to treat multiple retinal diseases with just one drug.

They call their breakthrough technology “one to many,” meaning the product could be the answer to several eye-related diseases.

Some of the rare conditions Ocugen has been working on are wet age-related macular degeneration, diabetic macular edema, and diabetic retinopathy.

Ocugen’s growth prospects, especially in 2021, heavily relies on the company’s ability to get an emergency use authorization for Covaxin in the US.

This means that investors should brace themselves for volatility in the next months as the vaccine candidate moves forward with the clinical trials.

In terms of long-term prospects, it remains to be seen how Ocugen will take advantage of the momentum it gained from the COVID-19 partnership with Bharat.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-09 14:00:112021-02-14 15:05:09New Generation of Biotech Players

Below please find subscribers’ Q&A for the February 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Is there a big difference between COVID-19 vaccines?

A: The best vaccine is the one you can get. It’s better than being dead. But there are important differences. The Pfizer (PFE) and Moderna (MRNA) vaccines are RNA vaccines, they’re very safe, and getting similar results. But the evidence shows that about 15% of Moderna recipients are coming down with flu-like symptoms on their second shot. Nobody knows why, as the two are almost biochemically identical. AstraZeneca is a killed virus type vaccine, which means if they have a manufacturing error, you end up giving the disease to people by accident, as with the original polio vaccine. So that's the less safe vaccine. So far, that one has only been used in Europe and Australia, as it is made in England. There isn’t enough data about the John & Johnson (JNJ) single-shot vaccine.

Q: Is Moderna (MRNA) a long term buy?

A: The trouble with all the vaccine plays is that we’re heading for a global vaccine glut in about 4 months when we’ll have something like 12 companies around the world making them. The rush for everyone to get a vaccination as soon as possible is leading to inevitable overproduction and falling stock prices. Moderna is already a 12 bagger for us. I’m not really looking to overstay my welcome, so to speak. Time to cash in and say, “Thank you very much, Mr. Market.” There will be another cycle down the road for (MRNA) as its technology is used to cure cancer, but not yet.

Q: Would you recommend a silver (SLV) LEAP?

A: Yes, silver was run up 35% for a day by the GameStop (GME) crowd and crashed the next day, which was to be expected because there are no short positions in silver. Everything was just hedged to look like there were short positions because the big banks had huge open short options positions that were public and hedges in the futures and silver bars that were private. The (GME) people only saw the public short positions. Long term, I would go for a $30-$32 vertical call spread expiring in 2023. Go out 2 years, and I think you could get silver at $50. So, a good LEAP might get you a 1000% return in two years. Those are the kinds of trades I like to do.

Q: What do you think of Amazon now that Jeff Bezos is retiring?

A: Buy the daylights out of it. That was the great unknown overhanging the stock for years, Jeff’s potential retirement. Now it's no longer unknown, you want to buy (AMZN). Even before the retirement, I was targeting $5,000 a share in two years. Now we have everybody under the sun raising their targets to $5,000 or more— we even had one upgrade today to $5,200. There are at least half a dozen businesses that Amazon can expand into, like healthcare, which will be multibillion-dollar earners. And then if you break it up because of antitrust, it doubles in value again, so that's a screaming buy here. We have flatlined for six months, so this could be a trigger for a long-term breakout.

Q: Is there anything else left after GameStop? Another short play?

A: Well, this was the worst short squeeze in 25 years, and everyone else covered their other shorts because they don't want to get wiped out like the one Melvin Capital. There were only around a dozen potential single-digit heavily shorted stocks out there, and those are mostly gone. So, the GameStop crowd will have to roll up their sleeves and do some hard work finding stocks the old fashion way—by doing research. I’m guessing that GameStop was a one-hit-wonder; we probably won’t be surprised again. At the same time, you should never underestimate the stupidity of other investors.

Q: What do you think of the cloud plays like Cloudera and Snowflake?

A: I love cloud plays and there will be more coming. The entire US economy is moving on to the cloud. But everyone else loves them too. Snowflake (SNOW) doubled on its first day, and Cloudera (CLDR) doubled over the last three months, so they're incredibly expensive and high risk. But you can't argue with their business models going forward—the cloud is here to stay.

Q: Would you buy LEAPS in financials?

A: Absolutely yes; go out two years for your maturity and 30% on your strike prices, you will get a ten bagger on the trade. If I’m wrong, it only goes to zero.

Q: Is US Steel (X) a buy?

A: Yes. They are being dragged up by the global commodity boom triggered by the global synchronized recovery. (X) took a hit today because they just priced a $700 million secondary share issue which the flippers dumped like a hot potato. If given the choice, I’d rather do a copper play with Freeport McMoRan (FCX) which is seeing much more buying from China. I bought it on Monday.

Q: Any chance you can include one-, three-, and five-year price targets?

A: No chance whatsoever. I’ve never heard of a fund manager that could do that and be right. Stocks are just too imprecise an instrument with all the emotion that’s involved. But for the better stocks, you can with confidence predict at least a double. And by the way, all my predictions for the last 13 years have been way, way on the low side, so I tend to be conservative. Like, remember when Amazon was at $10? I said it would go to $20. Boy was I right!

Q: How can you say the next four years will be good for the stock market?

A: Well, $10 trillion in fiscal stimulus, $10 trillion in QE; stocks tend to like that. Oh, and technology exponentially accelerating on all fronts and far more broadly than what we saw in the 1990s. Also, there is a certain person who is no longer president, so add about 10-20% on top of all stock valuations. Companies can finally do long term planning again, after being unable to do so for four years because policies were anti-trade, anti-business, and flip-flopping every other day. So yes, I think that's enough to make the next 4 four years good; and actually, I think the next 8 years could be good—I'm predicting Dow 120,000 by 2030, if you recall.

Q: When do you expect the next 5% correction if there is one? February is always very volatile.

A: With an unlimited liquidity market like we have, it is really tough to see negatives of any kind. What kind of negatives are out there? The pandemic doesn’t stop—that's the main one. There’s another one people aren't talking about: the reason we got all these vaccines so fast is they took all regulation and threw it out the window. What if one of these vaccines kill off a million people? That would be pretty negative for the market. Interest rates could rocket faster than expected. But I’m always short there so that would be a moneymaker. But these are pretty out there possibilities, and that is why the market is not backing off, and when it does, it only gives us 5%.

Q: Is the Fed stimulating the economy too much?

A: The bond market says no with a ten-year yield of 1.10%, and the bond market is always the ultimate arbiter of when the stimulus ends. That’s because the Fed can’t directly control bond market interest rates, only overnight rates. But when we get bonds up to, say, a 3% yield (which is probably 2 or 3 years off), that’s when we’re getting too much stimulus, and we’ll probably take our foot off the pedal way before then. I know Janet Yellen and she agrees with me on this point. She’ll be throttling back well before we see a 3% yield in the Treasury market.

Q: Do you manage other people’s money?

A: No, because it costs a million dollars in legal fees to set up even a small fund these days. When I set up my hedge fund 30 years ago, there were no regulatory costs because no one knew what a hedge fund was; they all thought they were doing something illegal, so they didn't have to register for anything. That’s why it’s changed now.

Q: What is your target on NVIDIA (NVDA), and will it split?

A: It’s an easy double, with a global chip shortage running rampant. They make the best graphics cards in the world, bar none. These big tech companies tend not to split until they get share prices into the thousands, which is what Apple (AAPL) and what Tesla (TSLA) did three or four times.

Q: If we get 3.25% in bonds, is that going to hurt gold?

A: Yes, and that’s one of the reasons I bailed on my gold positions a couple of weeks ago. It effectively turned into a bond long. A sharp rise in interest rates is bad for gold because we all know that gold yields to zero.

Q: What about Fireye (FEYE)?

A: Yes, we also love Fireye in addition to Palo Alto Networks (PANW) because there is a near-monopoly—there are only about six players in the entire cybersecurity industry and hacking is getting worse by the day. Look at the Solar Winds (SWI) fiasco and the national Russian hack there.

Q: What about copper as a recovery play?

A: Well, I voted with my feet on Monday when I bought a position in Freeport McMoRan, after it just sold off 15%. I think (FCX) could double at some point in the coming economic recovery. So, copper is an absolute winner, and when having to choose between copper and steel, I’ll pick copper all day long.

Q: What do you recommend for gold (GLD)?

A: Gold is a trading range for the time being. Buy the dips, sell the rallies; you won’t get more than about 10% or 15% range on that. And there are just better fish to fry right now, like financials, which benefit from rising interest rates as opposed to being punished. Bitcoin is stealing gold’s thunder and the markets keep creating more Bitcoins.

Q: Should high-frequency trading be banned?

A: I don’t think it should be. It does create liquidity; the effect on the market is wildly overexaggerated. They’re basically trading for pennies or tenths of pennies, so they do provide buying on selloffs and selling at huge price spikes. They do have a positive effect and they’re probably only taking about $10 or $20 billion in profit a year out of the market.

Q: Should I buy Wynn Resorts (WYNN) here?

A: Buy the dips for sure; this is a major recovery play. We here in Nevada are expecting an absolute tidal wave of people to hit the casinos once the pandemic ends, and (WYNN), (MGM), and (LVS) would be a great play in those areas.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/lake-tahoe-sunrise.png460612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-05 09:34:282021-02-05 08:16:16February 3 Biweekly Strategy Webinar Q&A

If you were given the chance to choose, how would you prefer to get vaccinated against COVID-19: by getting an injection or by taking a pill?

For a lot of people, it’s a no-brainer to choose the pill—and one biotechnology company has been working hard to turn that into a reality: Vaxart (VXRT).

Last January 2020, Vaxart was only a micro-cap stock focused on developing a lineup of oral-tablet vaccines as treatments for viral infections.

When news broke that the company has been developing a COVID-19 vaccine in the form of a pill, its shares rocketed by over 1,250% in the past 12 months.

From a micro-cap stock trading for as little as $0.70 last year, Vaxart has been trading somewhere between $21 to $23 per share since 2021 started.

In fact, Vaxart even managed to outpace other biotechs already leading in the coronavirus market like Pfizer’s (PFE) partner BioNTech (BNTX), and Moderna (MRNA).

If Vaxart’s vaccine, VXA-CoV2-1, receives regulatory approval, then its COVID-19 vaccine candidate offers key advantages over its rivals.

The first is that VXA-CoV2-1 comes in the form of pills, making it a more convenient and generally preferable option for a lot of patients.

The second is that VXA-CoV2-1 can be stored at room temperature, which eliminates any type of special handling unlike the vaccines of Pfizer-BioNTech, Moderna, and even AstraZeneca (AZN).

The third is that you can take VXA-CoV2-1 on your own. Since these are pills, there is no need for a healthcare worker to administer the COVID-19 vaccine.

This means that VXA-CoV2-1 can be delivered for at-home use.

These advantages effectively eliminate barriers in the healthcare systems, making it easier and more convenient to purchase and deploy VXA-CoV2-1.

Looking at all potential markets, Vaxart could find a niche in underdeveloped regions.

On top of all these conveniences, the technology used to develop VXA-CoV2-1 can also be utilized in creating an oral vaccine against other diseases.

So far, VXA-CoV2-1 is only in Phase 1 of its clinical trials, with new data expected to be released this February.

Prior to this, results showed that VXA-CoV2-1 eased lung viral load and alleviated lung inflammation in hamsters that were infected with COVID-19.

While all these definitely sound amazing, everything is still in very early stages. Plus, results from hamster studies are a far cry from showing efficacy in human beings.

This makes the Phase 1 data release a sort of make-or-break event for Vaxart.

Other than its COVID-19 vaccine candidate, Vaxart has been working on an oral vaccine for influenza as well.

This product is currently undergoing Phase 2 clinical trials and has so far surpassed the efficacy of Sanofi’s (SNY) Fluzone by 8%.

So, is Vaxart the new darling of the biotech world?

It definitely has the potential.

However, its success hinges on everything aligning perfectly. But as a certain guy named Murphy has pointed out, that oftentimes does not happen.

Vaxart is subject to forces beyond its control.

There’s no absolute guarantee that its COVID-19 vaccine candidate will fare well in all the clinical trials.

Vaxart has a viable path of delivering humongous gains this year. However, this path is also riddled with lots of risks.

It is a highly risky stock and is best left to aggressive investors.

Moreover, Vaxart is in a precarious position right now, wherein a failed clinical result in human studies would be devastating for the shares.

On the other side, a positive human data readout would send the shares soaring in the next months.

Truth be told, sky would be the limit for Vaxart’s stock price if FDA actually approves its oral vaccine candidate.

Undoubtedly, Vaxart will be at the center of debates between short-sellers and passionate bulls throughout 2021. The bottom line is that will always be a trade-off of risk and reward in any type of investing.

If you have faith in Vaxart’s science and are confident that you have the stomach for a crazy roller-coaster ride, then you can give this biotech stock a chance.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-04 14:00:582021-02-08 15:27:03Is This the Next Biotech Darling?

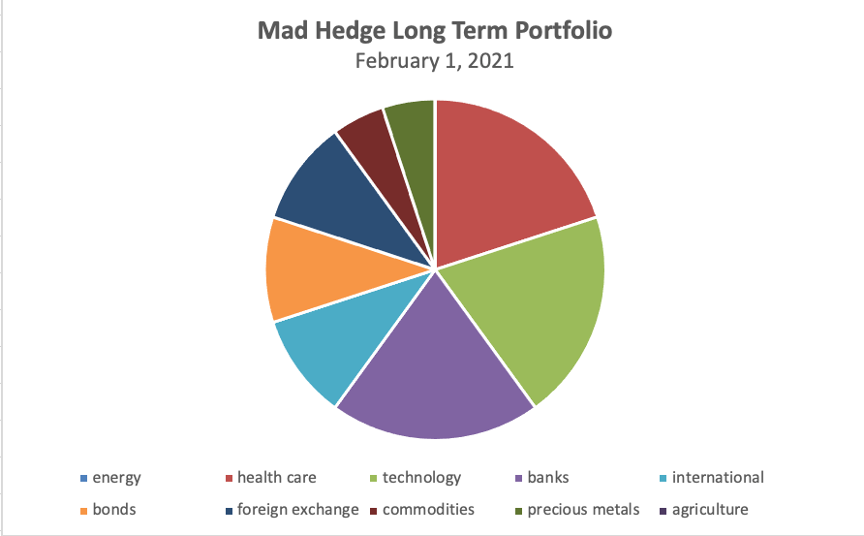

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on July 21, 2020. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted below.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

Changes

I am cutting back my weighting in biotech from 25% to 20% because Celgene (CELG) was taken over by Bristol Myers (BMY) at a 110% profit compared to our original cost. We also earned a spectacular 145% gain on Crisper Therapeutics (CRSP). I’m keeping it because I believe it has more to run.

My 30% weighting in technology also gets pared back to 20% because virtually all of my names have doubled or more. These have been in a sideways correction for the past six months but are still an important part of any barbell portfolio. So, take out Facebook (FB) and PayPal (PYPL) and keep the rest.

I am increasing my weighting in banks from 10% to 20%. Interest rates are finally starting to rise, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, add in Morgan Stanley (MS) and Goldman Sachs (GS), which will profit enormously from a continuing bull market in stocks.

Along the same vein, I am committing 10% of my portfolio to a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis, so go read Global Trading Dispatch.

I am keeping my 10% international exposure in Chinese Internet giant Alibaba (BABA) and the iShares MSCI Emerging Market ETF (EEM). The Biden administration will most likely dial back the recent vociferous anti-Chinese stance, setting these names on fire.

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). The Aussie has been the best performing currency against the US dollar and that should continue.

Australia will be a leveraged beneficiary of the synchronized global economic recovery, both through strong commodity prices and gold which has already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

As for precious metals, I’m baling on my 10% holding in gold (GLD), which delivered a nice 20% gain in 2020. From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

Yes, in this liquidity-driven global bull market, a 20% return is just not enough to keep my interest. Instead, I add a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles.

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/long-term-portfolio.png536864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-02 10:02:032021-02-02 10:37:30My Newly Updated Long-Term Portfolio

Many predictions this 2021 probably won’t pan out. However, here’s a pretty safe bet: we will see a number of biotechnology company acquisitions this year.

Although it’s not easy to accurately forecast which biotechnology companies will be involved in these deals, there is a handful that qualifies as prime acquisition targets.

One of the top biotech buyout candidates in my radar this year is Translate Bio (TBIO).

Thanks to the massive success of the COVID-19 programs of Moderna (MRNA), Pfizer (PFE), and BioNTech (BNTX), a spotlight has been cast on the benefits of the messenger RNA (mRNA) technology.

That’s why I wouldn’t be surprised if bigger players in the healthcare industry decide to scoop up smaller players to stake a claim in this quickly growing space.

Among all the small-cap biotechs in play, Translate Bio is easily one of the top prospects.

Before Moderna and BioNTech hogged the spotlight with their mRNA-based COVID-19 vaccines, Translate Bio was actually one of the strong contenders in the race. Unfortunately, it failed to keep up with its peers and is now lagging well behind the leaders.

On the flip side, the attention that mRNA technology has been getting these days seemed to have strengthened the confidence of investors in the technology – an effect that Translate Bio greatly benefited from in the past months.

Despite its lagging performance in the COVID-19 race, Translate Bio has been making significant progress with its work with partner Sanofi (SNY) on their own candidate, MRT5500. If all goes well, then the product should be out by the first quarter of 2021.

Apart from that, the two have been focusing on different vaccine candidates for other viral and bacterial diseases.

Translate Bio’s pipeline also includes treatments targeting another lucrative market using the same MRT platform technology as MRT5500: cystic fibrosis (CF).

The company’s CF treatment has been causing excitement among investors because instead of offering invasive therapy, this option offers patients an inhaled version of the mRNA drug as treatment.

Moreover, the MRT platform technology of Translate Bio could be expanded to cover more than just CF – a promising diversification that encouraged big investors like Sanofi to continuously pour money into collaborations with this Massachusetts-based biotech.

As mRNA technology gains more traction, Sanofi might even reevaluate its relationship with Translate Bio and decide that it wants more than just a collaboration.

With the smaller biotech company’s modest market capitalization of only a little over $1.7 billion, an acquisition could be on the table sooner rather than later.

Another potential buyout candidate is Bluebird bio (BLUE).

Unlike its contemporaries in the biotech space, Bluebird shares plunged by nearly 50% in 2020.

Although the company offers a promising upside potential, it can’t seem to generate sufficient enthusiasm to take part in the biotech sector’s rally last year.

In fact, Blue stock continued to hover near its 52-week low despite several gene and cell therapy tickers reaching all-time highs.

While that’s obviously bad news for Bluebird shareholders, I think this makes the company an even more attractive acquisition candidate.

I think it’s important to determine the reasons behind Bluebird’s abysmal 2020 performance.

The stock had a rocky start last year, with the COVID-19 pandemic exacerbating its overall meltdown.

One of Blue’s major roadblock was its failure to secure approval from the FDA for its multiple myeloma treatment, which it has been working on with Bristol Myers Squibb (BMY).

Then, it delayed its submission for approval of its sickle cell disease treatment LentiGlobin. This was initially set for the second half of 2021 but was pushed to late 2022.

The main takeaway from this streak of negative updates is that Blue still doesn’t have its act together when it comes to dealing with regulatory approval processes.

Regardless, the potential of this biotech’s pipeline remains impressive.

Apart from its work with Bristol and LentiGlobin, Bluebird has been working on a late-stage candidate for treatment of a rare metabolic disorder called cerebral adrenoleukodystrophy with Lenti-D.

Prior to its partnership with Bristol, Bluebird was actually partnered with Celgene.

When Celgene was bought by Bristol in 2019, the bigger company continued the collaboration with Blue and expanded the partnership to cover more genetic disorders and extend to oncology treatments.

Due to the setbacks, Bluebird’s market capitalization now hovers somewhere near $3 billion.

Given all these pipeline candidates and its future plans, I suspect it wouldn’t take long before a major player takes notice of this attractive valuation and puts this bird in a cage.

Overall, both Translate Bio and Bluebird are solid companies in the biotechnology space.

While the COVID-19 pandemic slowed down some of their progress, the products in their pipelines could yield substantial value to interested acquisition partners.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-28 13:00:462021-01-30 23:25:21Watch Out for These Buyout Stocks

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-26 12:04:242021-01-26 12:51:27January 26, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.