The probability of a recession taking place over the next 12 months is now low ranging as high as 20%. If it reaccelerates, not an impossibility, you can take that up to 100%.

And here’s the scary part. Bear markets front-run recessions by 6-12 months, i.e. now.

We’ll get a better read on the inflation numbers over the coming months. If inflation turns hot again, the Fed will be forced to raise rates to once unimagined levels.

So, it’s time to start asking the question of what the next recession will look like. Are we in for another 2008-2009 meltdown, when friends and relatives lost homes, jobs, and their entire net worth? Or can we look forward to a mild pullback that only economists and data junkies like myself will notice?

I’ll paraphrase one of my favorite Russian authors, Fyodor Dostoevsky, who in Anna Karenina might have said, “All economic expansions are all alike, while recessions are all miserable in their own way.”

Let’s look at some major pillars of the economy. A hallmark of the 2008 recession was the near collapse of the financial system, where the ATMs were probably within a week of shutting down nationally. The government had to step in with the TARP, and mandatory 5% equity ownership in the country’s 20 largest banks.

Back then, banks were leveraged 40:1 in the case of Morgan Stanley (MS) and Goldman Sachs (GS), while Lehman Brothers and Bear Stearns were leveraged 100:1. In that case the most heavily borrowed companies only needed markets to move 1% against them to wipe out their entire capital. That is exactly what happened. (MS) and (GS) came within a hair’s breadth of going the same way.

Thanks to the Dodd Frank financial regulation bill, banks cannot leverage themselves more than 10:1. They have spent a decade rebuilding balance sheets and reserves. They are now among the healthiest in the world, having become low-margin, very low-risk utilities. It is now European and Chinese banks that are going down the tubes.

How about real estate, another major cause of angst in the last recession? The market couldn’t be any more different today. There is a structural shortage of housing, especially at entry level affordable prices. While liar loans and house flipping are starting to make a comeback, they are nowhere near as prevalent as a decade ago. And the mis-rating of mortgage-backed securities from single “C” to triple “A” is now a distant memory. (I still can’t believe no one ever went to jail for that!).

And interest rates? We went into the last recession with a 6% overnight rate and a 7% 30-year fixed rate mortgage. Here we are once again.

The auto industry has been in a mild recession for the past two years, with annual production stalling at 15 million units, versus a 2009 low of 9 million units. In any, case the challenges to the industry are now more structural than cyclical, with new buyers decamping en masse to electric vehicles made on the west coast.

Of far greater concern are industries that are already in recession now. Energy has been flagging since oil prices peaked 18 months ago, despite massive tax subsidies. It is suffering from a structural oversupply and falling demand.

Retailers have been in a Great Depression for five years, squeezed on one side by Amazon and the other by China. A decade into store closings and the US is STILL over-stored. However, many of these shares are already so close to zero that the marginal impact on the major indexes will be small.

Financials and legacy banks are also facing a double squeeze from Fintech innovation and collapsing interest rates. All of those expensive national networks with branches on every street corner will be gone later in the 2020s.

And no matter how bad the coming recession gets technology, now 30% of the S&P 500, will keep powering on. Combined revenues of the “Magnificent Seven” in Q1 are at records. That leaves a mighty big cushion for any slowdown. That’s a lot more than the “eyeballs” and market shares they possessed a decade ago.

So, netting all this out, how bad will the next recession be? Not bad at all. I’m looking at a couple of quarters' small negative numbers, like two back-to-back -0.1%’s. Then we’ll see a recovery and probably another decade of decent US growth.

The stock market, however, is another kettle of fish. While the economy may slow from a 2.2% annual rate to -0.1% or -0.2%, the major indexes could fall much more than that, say 30% to 40%.

Earnings multiples are still at a 19X high compared to a 9X low in 2009. Shares would have to drop 53% just to match the last low. Equity weightings in portfolios are low. Money is pouring out of stock funds into bond ones.

Corporations buying back their own shares have been the principal prop from the market for the past three years. Some large companies, like Kohls (KSS), have retired as much as 50% of their outstanding equity in ten years.

The Next Bear Market is Not Far Off

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/What-the-Next-Recession-Will-Look-Like.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-21 09:04:122023-07-21 15:33:10What the Next Recession Will Look Like

Mad Hedge Biotech & Healthcare Letter April 28, 2020 Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE) (GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/jt101.jpg400400JPhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngJP2020-05-12 17:34:012021-04-05 14:00:23The Five Frontrunners in the Race for a COVID-19 VACCINE

Just as every cloud has a silver lining, every stock market crash offers generational opportunities.

In a month or two, there will be spectacular trades to be had with LEAPS. What are LEAPS, you may ask?

This is the best strategy with which to cash in on the gigantic market swoons, which have become a regular feature of our markets.

Since the advent of the recent incredible market volatility, I have been asked one question.

What do you think about LEAPS?

LEAPS, or Long Term Equity AnticiPation Securities, is just a fancy name for a stock option spread with a maturity of more than one year.

You execute orders for these securities on your options online trading platform, pay options commissions, and endure option like volatility.

Another way of describing LEAPS is that they offer a way to rent stocks instead of buying them, with the prospect of enjoying years’ worth of stock gains for a fraction of the price.

While these are highly leveraged instruments, you can’t lose any more money than you put into them. Your risk is well defined.

And there are many companies in the market where LEAPs are a very good idea, especially on those gut-wrenching 1,000-point down days.

Interested?

Currently, LEAPS are listed all the way out until January 2022, some 695 days away.

However, the further expiration dates will have far less liquidity than near month options, so they are not a great short-term trading vehicle. That is why limit orders in LEAPS, as opposed to market orders, are crucial.

These are really for your buy-and-forget investment portfolio, defined benefit plan, 401k, or IRA.

Because of the long maturities, premiums can be enormous. However, there is more than one way to skin a cat, and the profit opportunities here can be astronomical.

Like all options contracts, a LEAP gives its owner the right to "exercise" the option to buy or sell 100 shares of stock at a set price for a given time.

LEAPS have been around since 1990, and traded on the Chicago Board Options Exchange (CBOE).

To participate, you need an options account with a brokerage house, an easy process that mainly involves acknowledging the risk disclosures that no one ever reads.

If a LEAP expires "out-of-the-money" – when exercising, you can lose all the money that was spent on the premium to buy it. There's no toughing it out waiting for a recovery as with actual shares of stock. Poof, and your money is gone.

LEAPS are also offered on exchange-traded funds (ETFs) that track indices like the Standard & Poor's 500 index (SPY) and the Dow Jones Industrial Average (INDU), so you could bet on up or down moves of the broad market.

Not all stocks have options, and not all stocks with ordinary options also offer LEAPS.

Note that a LEAPS owner does not vote proxies or receive dividends because the underlying stock is owned by the seller, or "writer," of the LEAP contract until the LEAP owner exercises.

Despite the Wild West image of options, LEAPS are actually ideal for the right type of conservative investor.

They offer more margin and more efficient use of capital than traditional broker margin accounts. And you don’t have to pay the usurious interest rates that margin accounts usually charge.

And for a moderate increase in risk, they present outsized profit opportunities.

For the right investor, they are the ideal instrument.

Let me go through some examples to show you their inner beauty.

By now, you should all know what vertical bull call spreads are. If you don’t, then please click their link for a quickie video tutorial. You must be logged in to your account.

Let’s go back to February 9, 2018 when the Dow Average plunged to its 23,800 low for the year. I then begged you to buy the Apple (AAPL) June, 2018 $130-$140 call spread at $8.10, which most of you did. A month later, that position is worth $9.40, up some 16.04%. Not bad.

Now let’s say that instead buying a spread four months out, you went for the full year and three months, to June 2019.

That identical (AAPL) $130-$140 would have cost $5.50 on February 9. The spread would be worth $9.40 today, up 70.90%, and worth $10 on June 21, 2019, up 81.81%.

So, by holding a 15-month to expiration position for only a month, you get to collect 86.67% of the maximum potential profit of the position.

So, now you know why we leap into LEAPS.

When the meltdown comes, and that could be as soon as today, use this strategy to jump into longer-term positions in the names we have been recommending and you should be able to retire early.

What’s out there today? Take a look at Boeing (BA), one of the most undervalued companies in the market, thanks to their 737 MAX woes.

Today, (BA) shares were trading at a lowly $305. Let say that Boeing shares recover to $350 by the end of 2020. You can buy a January 2021 $340-$350 vertical bull call spread for $3.00. If Boeing makes it back up to $350 by the January 15, 2021 option expiration, the LEAP will expire worth $10, an increase of 233%.

It gets better. You can buy a (BA) January 2022 $370-$380 call spread for $2.15. If Boeing recovers to $380 by the January 21, 2022 expiration it will expire worth $10, giving you a gain of 365%!

What if you think that Boeing is overdue for a monster rally back to its old all-time high of $450?

You can buy a (BA) January 2022 $420-$430 calls spread for $0.90. If Boeing makes it all the way back to $430 by the January 21, 2022 expiration, it will expire worth $10, giving you a gain of 1,011%! Caution: If the shares only make it back up to $429, the position becomes worthless.

Now you know why I like LEAPS so much. Play around with the names and the numbers and I’m sure you will find something you like. But remember one thing. Buying LEAPS is only a trade to consider at long time market bottoms, not tops!

Time to Leap Into LEAPS

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/leap-of-faith.jpg400400Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2020-02-27 08:04:432020-05-12 22:29:43Get Ready to Take a Leap Back into Leaps

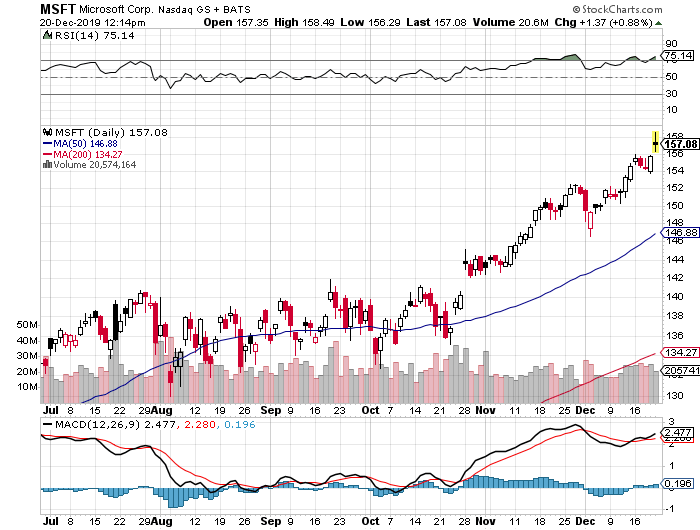

EXPIRATION of the Microsoft (MSFT) December 2019 $134-$137 in-the-money vertical BULL CALL spread at $3.00

Closing Trade

12-20-2019

expiration date: December 20, 2019

Portfolio weighting: 10%

Number of Contracts = 38 contracts

Provided that (MSFT) does not fall $20.08, or 12.73% by the close today, our position in the Microsoft (MSFT) December 2019 $134-$137 in-the-money vertical BULL CALL spread will expire at its maximum profit at $3.00.

As a result, you have earned $1,520, or 15.38% in 22 trading days. If you bought the shares instead, keep them. They are going much higher.

You don’t get any better quality than Microsoft (MSFT) in the tech world. It is the safest stock in which to invest today. This is a stock that you want to hide behind the radiator and keep forever. It is also one of the great turnaround stories of the decade.

In addition, this particular combination of strikes prices gave you huge support at the 50-day moving average at $140.67. Please note this option spread will be profitable whether the market goes up, sideways, or down small over the next four weeks.

This was a bet that Microsoft shares would NOT fall below $137.00 by the December 20 option expiration date in 22 trading days.

This was also a bet that we are not already in a recession, which I believe is still at least 12 months off.

You don’t need to do anything, as the expiration process is now fully automated. The profit will be deposited into your account and the margin freed up on Monday morning.

Well done, and on to the next trade!

EXPIRATION 38 December 2019 (MSFT) $134 calls at…….……$23.08 EXPIRATION short 38 December 2019 (MSFT) $137 calls at…….$20.08 Net Cost:………………………….…………..…..….….....$3.00

Profit: $3.00 - $2.60 = $0.40

(38 X 100 X $0.40) = $1,520 or 15.38% in 22 trading days.

The optics today look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter, and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possible destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business. Microsoft Azure grew 87% YOY last quarter.

To see how to enter this trade in your online platform, please look at the order ticket above, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Spread” by clicking here at http://www.madhedgefundtrader.com/ltt-vbpds/

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Keep in mind that these are ballpark prices at best. After the alerts go out, prices can be all over the map.

As you are all well aware, I have long been a history buff. I am particularly fond of studying the history of my own avocation, trading, in the hope that the past errors of others will provide insights for the future.

History doesn’t repeat itself, but it certainly rhymes.

So after decades of research on the topic, I thought I would provide you with a list of the eight worst trades in history. Some of these are subjective, some are judgment calls, but all are educational. And I do personally know many of the individuals involved.

Here they are for your edification, in no particular order. You will notice a constantly recurring theme of hubris.

1) Ron Wayne’s sales of 10% of Apple (AAPL) for $800 in 1976

Say you owned 10% of Apple (AAPL) and you sold it for $800 in 1976. What would that stake be worth today? Try $120 billion, making it undoubtedly one of the history's worst trades. That is the harsh reality that Ron Wayne, 78, faces every morning when he wakes up, one of the three original founders of the consumer electronics giant.

Ron first met Steve Jobs when he was a spritely 21-year-old marketing guy at Atari, the inventor of the hugely successful “Pong” video arcade game.

Ron dumped his shares when he became convinced that Steve Jobs’ reckless spending was going to drive the nascent startup into the ground and he wanted to protect his own assets in a future bankruptcy.

Co-founders Jobs and Steve Wozniak each kept their original 45% ownership. Today, Jobs’s widow, Laurene Powel Jobs, has a 0.5% ownership in Apple worth $4 billion, while the value of Woz’s share remains undisclosed.

Today, Ron is living off of a meager monthly Social Security check in remote Pahrump, Nevada, about as far out in the middle of nowhere as you can get, where he can occasionally be seen playing the penny slots.

2) AOL's 2001 Takeover of Time Warner

Seeking to gain dominance in the brave new online world, Gerald Levin pushed old-line cable TV and magazine conglomerate, Time Warner, to pay $164 billion to buy upstart America Online in 2001. AOL CEO, Steve Case, became chairman of the new entity. Blinded by greed, Levin was lured by the prospect of 130 million big spending new customers.

It was not meant to be.

The wheels fell off almost immediately. The promised synergies never materialized. The Dotcom Crash vaporized AOL’s business the second the ink was dry. Then came a big recession and the Second Gulf War. By 2002, the value of the firm’s shares cratered from $226 billion to $20 billion.

The shareholders got wiped out, including “Mouth of the South” Ted Turner. That year, the firm announced a $99 billion loss as the goodwill from the merger was written off, the largest such loss in corporate history. Time Warner finally spun off AOL in 2009, ending the agony.

Steve Case walked away with billions, and is now an active venture capitalist. Gerald Levin left a pauper, and is occasionally seen as a forlorn guest on talk shows. The deal is widely perceived to be the worst corporate merger in history.

Buy High, Sell Low?

3) Bank of America's Purchase of Countrywide Savings in 2008

Bank of America’s CEO Ken Lewis thought he was getting the deal of the century picking up aggressive subprime lender, Countrywide Savings, for a bargain $4.1 billion, a “rare opportunity.” Little did he know he would make it on the worst trades in history list.

Because unfortunately, as a result, Countrywide CEO Angelo Mozilo pocketed several hundred million dollars. Then the financial system collapsed, and suddenly we learned about liar loans, zero money down, and robo-signing of loan documents.

Bank of America’s shares plunged by 95%, wiping out $500 billion in market capitalization. The deal saddled (BAC) with liability for Countrywide’s many sins, ultimately, paying out $40 billion in endless fines and settlements to aggrieved regulators and shareholders.

Ken Lewis was quickly put out to pasture, cashing in on an $83 million golden parachute, and is now working on his golf swing. Mozilo had to pay a number of out-of-court settlements, but was able to retain a substantial fortune, and is still walking around free.

The nicely tanned Mozilo is also working on his golf swing.

4) The 1973 Sale of All Star Wars Licensing and Merchandising Rights by 20th Century Fox for Free

In 1973, my former neighbor George Lucas approached 20th Century Fox Studios with the idea for the blockbuster film, Star Wars. It was going to be his next film after American Graffiti which had been a big hit earlier that year.

While Lucas was set for a large raise for his directing services – from $150,000 for American Graffiti to potentially $500,000 for Star Wars – he had a different twist ending in mind. Instead of asking for the full $500,000 directing fee, he offered a discount: $350,000 off in return for the unlimited rights to merchandising and any sequels.

Fox executives agreed, figuring that the rights were worthless, and fearing that the timing might not be right for a science fiction film. In hindsight, their decision seems ridiculously short-sighted.

Since 1977, the Star Wars franchise has generated about $27 billion in revenue, leaving George Lucas with a net worth of over $3 billion by 2012. In 2012, Disney paid Lucas an additional $4 billion to buy the rights to the franchise.

The initial budget for Star Wars was a pittance at $8 million, a big sum for an unproven film. So, saving $150,000 on production costs was no small matter, and Fox thought it was hedging its bets. They certainly never imagined they were making one of the worst trades in history.

George once told me that he had a problem with depressed actors on the set while filming. Harrison Ford and Carrie Fisher thought the plot was stupid and the costumes silly.

Today, it is George Lucas who is laughing all the way to the bank.

$150,000 for What?

5) Lehman Brothers Entry Into the Bond Derivatives Market in the 2000s

I hated the 2000s because it was clear that men with lesser intelligence were using other people’s money to hyper leverage their own personal net worth. The money wasn’t the point. The quantities of cash involved were so enormous they could never be spent. It was all about winning points in a game with the CEOs of the other big Wall Street institutions.

CEO Richard Fuld could have come out of central casting as a stereotypical bad guy. He even once offered me a job which I wisely turned down. Fuld took his firm’s leverage ratio up to 100 times in an extended reach for obscene profits. This meant that a 1% drop in the underlying securities would entirely wipe out its capital.

That’s exactly what happened, and 10,000 employees lost their jobs, sent packing with their cardboard boxes with no notice. It was a classic case of a company piling on more risk to compensate for the lack of experience and intelligence. This only ends one way.

Morgan Stanley (MS) and Goldman Sachs (GS) drew the line at 40 times leverage and are still around today but just by the skin of their teeth, thanks to the TARP.

Fuld has spent much of the last five years ducking in and out of depositions in protracted litigation. Lehman issued public bonds only months before the final debacle, and how he has stayed out of jail has amazed me. Today he works as an independent consultant. On what I have no idea.

Out of Central Casting

6) The Manhasset Indians' Sale of Manhattan to the Dutch in 1626

Only a single original period document mentions anything about the purchase of Manhattan. This letter states that the island was bought from the Native Americans for 60 Dutch guilders worth of trade goods which would consist of axes, iron kettles, beads, and wool clothing.

No record exists of exactly what the mix was. Native Americans were notoriously shrewd traders and would not have been fooled by worthless trinkets.

The original letter outlining the deal is today kept at a museum in the Netherlands. It was written by a merchant, Pieter Schagen, to the directors of the West India Company (owners of New Netherlands) and is dated 5 November 1626.

He mentions that the settlers “have bought the island of Manhattes from the savages for a value of 60 guilders.” That’s it. It doesn’t say who purchased the island or from whom they purchased it, although it was probably the local Lenape tribe.

Certainly one of the worst trades in history, though historians often point out that North American Indians had a concept of land ownership different from that of the Europeans. They regarded land, like air and water, as something one could use but not own or sell. So, it has been suggested that the Native Americans thought they were sharing, not selling.

It is anyone’s guess what Manhattan is worth today. Just my old two-bedroom 34th-floor apartment at 400 East 56th Street is now worth $2 million. Better think in the trillions.

7) Napoleon's 1803 Sale of the Louisiana Purchase to the United States

Invading Europe is not cheap, as Napoleon found out, and he needed some quick cash to continue his conquests. What could be more convenient than unloading France’s American colonies to the newly founded United States for a tidy $7 million? A British naval blockade had made them all but inaccessible anyway.

What is amazing is that president Thomas Jefferson agreed to the deal without the authority to do so, lacking permission from Congress, and with no money. What lies beyond the Mississippi River then was unknown.

Many Americans hoped for a waterway across the continent while others thought dinosaurs might still roam there. Jefferson just took a flyer on it. It was up to the intrepid explorers, Lewis and Clark, to find out what we bought.

Sound familiar? Without his bold action, the middle 15 states of the country would still be speaking French, smoking Gitanes, and getting paid in Euros.

After Waterloo in 1815, the British tried to reverse the deal and claim the American Midwest for themselves. It took Andrew Jackson’s (see the $20 bill) surprise win at the Battle of New Orleans to solidify the US claim.

The value of the Louisiana Purchase today is incalculable. But half of a country that creates $17 trillion in GDP per year and is still growing would be worth quite a lot.

Great General, Lousy Trader

8) The John Thomas Family Sale of Nantucket Island in 1740

Yes, the investments of my own ancestors are to be included among the worst trades in history. My great X 12 grandfather, a pioneering venture capitalist investor of the day from England, managed to buy the island of Nantucket off the coast of Massachusetts from the Indians for three ax heads and a sheep in the mid-1600s. Barren, windswept, and distant, it was considered worthless.

Two generations later, my great X 10 grandfather decided to cut his risk and sell the land to local residents just ahead of the Revolutionary War. Some 17 of my ancestors fought in that war including the original John Thomas who served on George Washington’s staff at the harsh winter encampment at Valley Forge during 1777-78. Maybe that’s why I have an obsession with not wasting food?

By the early 19th century, a major whaling industry developed on Nantucket fueling the lamps of the world with smoke-free fuel. By then, our family name was “Coffin,” which is still abundantly found on the headstones of the island’s cemeteries.

One Coffin even saw his ship, the Essex, rammed by a whale and sunk in the Pacific in 1821. He was eaten by fellow crewmembers after spending 99 days adrift in an open lifeboat. Maybe that’s why I have an obsession with not wasting food?

In the 1840s, a young itinerant writer named Herman Melville visited Nantucket and heard the Essex story. He turned it into a massive novel about a mysterious rogue white whale, Moby Dick, which has been torturing English literature students ever since. Our family name, Coffin, is mentioned seven times in the book.

Nantucket is probably worth many tens of billions of dollars today as a playground for the rich and famous. Just a decent beachfront cottage there rents for $50,000 a week in the summer.

The 2015 Ron Howard film, The Heart of the Sea, is breathtaking. Just be happy you never worked on a 19th-century sailing ship.

Yes, it’s all true and documented.

Hi Grandpa!

https://www.madhedgefundtrader.com/wp-content/uploads/2019/12/the-eight-worst-trades-in-history-blog.jpg400400JPhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngJP2019-12-22 21:23:042020-05-11 14:04:03The Eight Worst Trades in History

Not a day goes by when someone doesn’t ask me about what to do about trading Apple (AAPL).

After all, it is the world largest publicly-traded company at a $1.2 trillion market capitalization. It is the planet’s most widely owned stock. Almost everyone uses their products in some form or another. It buys back more of its own stock than any other company on the planet. Oh yes, it is also one of Warren Buffet’s favorite picks.

So, the widespread adulation is totally understandable.

Apple is a company with which I have a very long relationship. During the early 1980s, I was ordered by Morgan Stanley to take Steve Jobs around to the big New York Institutional Investors to pitch a secondary share offering for the sole reason that I was one of three people who worked for the firm who was then from California.

They thought one West Coast hippy would easily get along with another. Boy, were they wrong, me in my three-piece navy blue pinstripe suit and Steve in his work Levi’s. It was the worst day of my life. Steve was not a guy who palled around with anyone. He especially hated investment bankers.

I got into Apple with my personal account when the company only had four weeks of cash flow remaining and was on the verge of bankruptcy. I got in at $7 which, on a split-adjusted basis today, is 50 cents. I still have them. In fact, my cost basis in Apple is less than the 77-cent quarterly dividend now.

Today, some 200 Apple employees subscribe to the Diary of a Mad Hedge Fund Trader looking to diversify their substantial holdings. Many own Apple stock with an adjusted cost basis of under $5. Suffice it to say, they all drive really nice Priuses.

So I get a lot of information about the firm far above and beyond the normal effluent of the media and stock analysts. That’s why Apple has become a favorite target of my Trade Alerts over the years.

And here is the great irony: Nobody would touch the stock with a ten-foot pole at the end of 2018. Since then, Apple has rallied 71%, creating more market cap in a year than any company in history.

Here’s why. Apple was all about the iPhone which then accounted for 75% of its total earnings. The TV, the watch, the car, the iPod, the iMac, and Apple Pay were all a waste of time and consumed far more coverage than they are collectively worth.

The good news is that iPhone sales are subject to a fairly predictable cycle. Apple launches a major new iPhone every other fall. The share price peaks shortly after that. The odd years see minor upgrades, not generational changes.

Just like you see a big pullback in the tide before a tsunami hits, iPhone sales are flattening out between major upgrades. This is because consumers start delaying purchases in expectation of the introduction of the new iPhones 7 more power, gadgets, and gizmos.

So during those in-between years, the stock performance was disappointing. 2018 certainly followed this script with Apple down a horrific 30.13% at the lows. Maybe it’s a coincidence, but the previous generation in Apple shares in 2015 brought a decline of, you guessed it, exactly 29.33%.

The coming quarter could bring quite the opposite.

After March, things will start to get interesting, especially post the Q1 earnings report in April. That’s when investors will start to discount the rollout of the new 5G iPhone seven months later. Everyone and their brother is waiting for 5G to purchase their next iPhone, unless it gets lost or stolen first.

The last time this happened, in 2018, Apple stock rocketed by $86, or 55.33%. This time, I expect a minimum rally to $400 high, or much higher. After all, I am such a conservative guy with my predictions (Dow 120,000 by 2030?).

Even at that price, it will still be one of the cheaper stocks in the market on a valuation basis which currently trades at a 20X earnings multiple. This is up from a subterranean multiple of 14X a year ago. The value players will have no choice to join in, if they’re not already there.

But Apple is a much bigger company this time around, and well-established cycles tend to bring in diminishing returns. It’s like watching the declining peaks of a bouncing rubber ball.

This is not your father’s Apple anymore. Services like iTunes and the new Apple+ streaming service are accounting for an even larger share of the company’s profits. And guess what? Services companies command much higher multiples than boring old hardware ones. It’s the old questions of linear versus exponential growth.

A China trade deal will bring a new spring to Apple’s step, where sales have recently been in free fall. Their new membership lease program promises to deliver a faster upgrade cycle that will allow higher premium prices for their products. That will bring larger profits.

It all adds up to keeping Apple as a core to any long term portfolio.

Just thought you’d like to know.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/12/trading-the-new-apple-in-2020-blog.jpg400400JPhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngJP2019-12-22 21:22:442020-05-11 14:03:54Trading the New Apple in 2020

You can count on a bear market hitting sometime in 2038, one falling by at least 25%.

Worse, there is almost a guarantee that a financial crisis, severe bear market, and possibly another Great Depression will take place no later than 2058 that would take the major indexes down by 50% or more.

No, I have not taken to using a Ouija board, reading tea leaves, nor examining animal entrails in order to predict the future. It can be much easier than that.

I simply read the data just released from the National Center for Health Statistics, a subsidiary of the federal Centers for Disease Control and Prevention (click here for their link).

The government agency reported that the US birth rate fell to a new all-time low for the second year in a row, to 60.2 births per 1,000 women of childbearing age. A birth rate of 125 per 1,000 is necessary for a population to break even. The absolute number of births is the lowest since 1987. In 2017, women had 500,000 fewer babies than in 2007.

These are the lowest number since WWII when 17 million men were away in the military, a crucial part of the equation.

The reason the American birth rate is such an important number is that babies grow up, or at least most of them do. In 20 years, they become consumers, earning wages, buying things, paying taxes, and generally contributing to economic growth.

In 45 years, they do so quite substantially, becoming the major drivers of the economy. When these numbers fall, recessions and bear markets occur with absolute certainty.

You have long heard me talk about the coming “Golden Age” of the 2020s. That’s when a two-decade long demographic tailwind ensues because the number of “peak spenders’ in the economy starts to balloon to generational highs. The last time this happened, during the 1980s and 1990s, stocks rose 20-fold.

Right now, we are just coming out of two decades of demographic headwind when the number of big spenders in the economy reached a low ebb. This was the cause of the Great Recession, the stock market crash and the anemic 2% annual growth since then.

The reasons for the maternity ward slowdown are many. The great recession certainly blew a hole in the family plans of many Millennials. Falling incomes always lead to lower birth rates, with many Millennial couples delaying children by five years or more. Millennial mothers are now having children later than at any time in history.

Burgeoning student debt, which just topped $1.5 trillion, is another. Many prospective mothers would rather get out from under substantial debt before they add to the population.

The rising education of women overall, a global trend, also contributes to the lag on having children. And spouses focused on career building often have a delayed interest in starting families.

Women are also delaying having children to postpone the “pay gaps” that always kicks in after they take maternity leave. Many are pegging income targets before they entertain starting families.

As a result of these trends, one in five children last year were born to women over the age of 35, a new high.

This is how some Latin American countries moved from eight to two-child families in only one generation. The same is about to take place in African countries where standards of living are rising rapidly, thanks to the eradication of several serious diseases.

The sharpest falls in the US have been with minorities. Since 2017, the birthrates for Latinos have dropped by 27% from a very high level, African Americans 11%, whites 5%, and Asian 4%.

Europe has long had the same problem with plunging growth rates but only much worse. Historically, the US has made up for the shortfall with immigration, but that is now falling, thanks the current administration policies. Restricting immigration now is a guaranty of slowing economic growth in the future. It’s just a numbers game.

So watch that growth rate. When it starts to tick up again, it’s time to buy….in about 20 years. I’ll be there to remind you with this newsletter.

As for me, I’ve been doing my part. I have five kids aged 14-34, and my life is only half over. Where did you say they keep the Pampers?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-04.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-24 10:04:382020-04-07 19:49:36They're Not Making Americans Anymore

About one-third of my readers are professional financial advisors who earn their crust of bread telling clients how to invest their retirement assets for a fixed fee.

They used to earn a share of the brokerage fees they generated. After stock commissions went to near zero, they started charging a flat 1.25% a year on the assets they oversaw.

So, it is with some sadness that I have watched this troubled industry enter a long-term secular decline that seems to be worsening by the day.

The final nail in the coffin may be the new regulations announced by the Department of Labor, at the end of the Obama administration, which controls this business.

Brokers, insurance agents, and financial planners were already held to a standard of suitability by the government, based on a client’s financial situation, tax status, investment objectives, risk tolerance, and time horizon.

The DOL proposed raising this bar to the level already required of Registered Investment Advisors, as spelled out by the Investment Company Act of 1940.

This would have required advisors to act only in the best interests of their clients, irrespective of all other factors, including the advisor’s compensation or conflicts of interest.

What this does is increase the costs while also greatly expanding advisor liability. In fact, the cost of malpractice insurance has already started to rise. All in all, it makes the financial advisor industry a much less fun place to be.

As is always the case with new regulations, they were inspired by a tiny handful of bad actors.

Some miscreants steered clients into securities solely based on the commissions they earned, which could reach 8% or more, whether it made any investment sense or not. Some of the instruments they recommended were nothing more than blatant rip-offs.

The DOL thought that the new regulations will save consumers $15 billion a year in excess commissions.

Legal action by industry associations has put the DOL proposals in limbo. Unless it appeals, it is unlikely to become law. So, there will be a respite, at least until the next administration.

Knowing hundreds of financial advisors personally, I can tell you that virtually all are hardworking professionals who go the extra mile to safeguard customer assets while earning incremental positive returns.

That is no easy task given the exponential speed with which the global economy is evolving. Yesterday’s “window and orphans” safe bets can transform overnight into today’s reckless adventure.

Look no further than coal, energy, and the auto industry. Once a mainstay of conservative portfolios, all of these sectors have, or came close to filing for bankruptcy.

Even my own local power utility, Pacific Gas & Electric Company (PGE), filed for chapter 11 in 2001 because they couldn’t game the electric power markets as well as Enron.

Some advisors even go the extent of scouring the Internet for a trade mentoring service that can ease their burden, like the Diary of a Mad Hedge Fund Trader, to get their clients that extra edge.

Traditional financial managers have been under siege for decades.

Commissions have been cut, expenses increased, and mysterious “fees” have started showing up on customer statements.

Those who work for big firms, like UBS, Morgan Stanley, Goldman Sacks, Merrill Lynch, and Charles Schwab, have seen health insurance coverage cut back and deductibles raised.

The safety of custody with big firms has always been a myth. Remember, all of these guys would have gone under during the 2008-09 financial crash if they hadn’t been bailed out by the government. It will happen again.

The quality of the research has taken a nosedive, with sectors like small caps no longer covered.

What remains offers nothing but waffle and indecision. Many analysts are afraid to commit to a real recommendation for fear of getting sued, or worse, scaring away lucrative investment banking business.

And have you noticed that after Dodd-Frank, two-thirds of a brokerage report is made up of disclosures?

Many financial advisors have, in fact, evolved over the decades from money managers to asset gatherers and relationship managers.

Their job is now to steer investors into “safe” funds managed by third parties that have to carry all of the liability for bad decisions (buying energy plays in 2014?).

The firms have effectively become toll-takers, charging a commission for anything that moves.

They have become so risk-averse that they have banned participation in anything exotic, like options, option spreads, (VIX) trading, any 2X leveraged ETF’s, or inverse ETFs of any kind. When dealing in esoterica is permitted, the commissions are doubled.

Even my own newsletter has to get compliance review before it is distributed to clients, often provided by third parties to smaller firms.

“Every year, they try to chip away at something”, one beleaguered advisor confided to me with despair.

Big brokers often hype their own services with expensive advertising campaigns that unrealistically elevate client expectations.

Modern media doesn’t help either.

I can’t tell you how many times I have had to convince advisors not to dump all their stocks at a market bottom because of something they heard on TV, saw on the Internet, or read in a competing newsletter warning that financial Armageddon was imminent.

Customers are force-fed the same misinformation. One of my main jobs is to provide advisors with the fodder they need to refute the many “end of the world” scenarios that seem to be in continuous circulation.

In fact, a sudden wave of such calls has proven to be a great “bottoming” indicator for me.

Personally, I don’t expect to see another major financial crisis until 2032 at the earliest, and by then, I’ll probably be dead.

Because of all of the above, about half of my financial advisor readers have confided in me a desire to go independent in the near future, if they are not already.

Sure, they won’t be ducking all these bullets; but at least they will have an independent business they can either sell at a future date, or pass on to a succeeding generation.

Overheads are far easier to control when you own your own business, and the tax advantages can be substantial.

A secular trend away from non-discretionary to discretionary account management is a decisive move in this direction.

There seems to be a great separating of the wheat from the chaff going on in the financial advisory industry.

Those who can stay ahead of the curve, both with the markets and their own business models, are soaking up all the assets. Those who can’t are unable to hold onto enough money to keep their businesses going.

Let’s face it, in the modern age, every industry is being put through a meat grinder. Thanks to hyper accelerating technology, business models are changing by the day.

Just be happy you’re not a doctor trying to figure out Obamacare.

Those individuals who can reinvent themselves quickly will succeed. Those who can't will quickly be confined to the dustbin of history.

It's Not As Easy As It Looks

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-05.jpg400400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-24 10:02:392020-04-07 16:50:45The Death of the Financial Advisor

It looks like the cyber security sector is about to take off like a rocket once again. There could be another 25%-50% in it this year.

The near destruction of Sony (SNE) by North Korean hackers last November has certainly put the fear of God into corporate America. Apparently, they have no sense of humor whatsoever north of the 38th parallel.

As a result, there is a generational upgrade in cyber security underway, with many potential targets boosting spending by multiples.

It's not often that I get a stock recommendation from an army general. However that's exactly what happened the other day when I was speaking to a three star about the long-term implications of the Iran peace deal.

He argued persuasively that the world will probably never again see large-scale armies fielded by major industrial nations. Wars of the future will be fought online, as they have been, silently and invisibly, over the past 15 years.

All of those trillions of dollars spent on big ticket, heavy metal weapons systems are pure pork designed by politicians to buy voters in marginal swing states.

The money would be far better spent where it is most needed, on the cyber warfare front. Needless to say, my friend shall remain anonymous.

The problem is that when wars become cheaper, you fight more of them, as is the case with online combat.

A little known fact is that during the Bush administration, the Chinese military downloaded the entire contents of the Pentagon's mainframe computers at least seven times.

This was a neat trick because these computers were in stand alone, siloed, electromagnetically shielded facilities not connected to the Internet in any way.

In the process, they obtained the designs of all of out most advanced weapons systems, including our best nukes. And what have they done with this top-secret information?

Absolutely nothing.

Like many in senior levels of the US military, the Chinese have concluded that these weapons are a useless waste of valuable resources. Far better value for money are more hackers, coders and servers, which the Chinese have pursued with a vengeance.

You have seen this in the substantial tightening up of the Chinese Internet through the deployment of the Great Firewall, which blocks local access to most foreign websites.

Try sending an email to someone in the middle Kingdom with a gmail address. It is almost impossible. This is why Google (GOOG) closed their offices there years ago.

My awareness of this comes from several Chinese readers complaining to me that they are unable to open my Trade Alerts or access their foreign online brokerage accounts.

As a member of the Joint Chiefs of Staff recently told me, "The greatest threat to national defense is wasting money on national defense."

If wars are now being fought online, then investing in national defense has actually come to mean investing in cyber security.

And although my brass-hatted friend didn't mention the company by name, the implication was that I need to go out and buy Palo Alto Networks (PANW) right now.

Palo Alto Networks, Inc. is an American network security company based in Santa Clara, California just across the water from my Bay Area office. The company's core products are advanced firewalls designed to provide network security, visibility and granular control of network activity based on application, user, and content identification.

Palo Alto Networks competes in the unified threat management and network security industry against Cisco (CSCO), FireEye (FEYE), Fortinet (FTNT), Check Point (CHKP), Juniper Networks (JNPR), and Cyberoam, among others.

The really interesting thing about this industry is that there are no real losers. That's because companies are taking a layered approach to cyber security, parceling out contracts to many of the leading firms at once, looking to hedge their bets.

To say that top management has no idea what these products really do would be a huge understatement. Therefore, they buy all of them.

This makes a basket approach to the industry more feasible than usual. You can do this through buying the $435 million capitalized PureFunds ISE Cyber Security ETF (HACK), which boasts Cyberark Software (CYBR), Infoblox (BLOX) and FireEye (FEYE) as its three largest positions. (HACK) has been a hedge fund favorite since the Sony attack.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/03/john-thomas-01.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-03-24 01:06:432020-04-06 15:28:31Cyber Security is Only Just Getting Started

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.