So far in 2015 the Indian stock market has handily beaten that of the US, by 10.6% compared to 5.3%.

?The India election result is the biggest development to affect emerging markets over the last 30 years.? That is what retired chairman of Goldman Sachs Asset Management and originator of the ?BRIC? term, Jim O?Neal, told me last week.

Indeed, the stunning news has sent long term country specialists scampering. In my long term strategy lectures I have been titillating listeners for years with predictions that India was about to become the next China.

With half the per capita income of the Middle Kingdom, India was lacking the infrastructure needed to compete in the global marketplace. All that was needed was the trigger.

This is the trigger.

With a new party taking control of the government for the first time in 50 years, the way is now clear to carry out desperately needed sweeping political and economic reforms. At the top of the list is a clean sweep of corruption, long endemic to the subcontinent. I once spent four months traveling around India on the Indian railway system, and the demand for ?bakshish? was ever present.

A reviving and reborn India has massive implications for the global economy, which could see growth accelerate as much at 0.50% a year for the next 30 years. This will be great news for stocks everywhere. It will help offset flagging demand for commodities from China, like coal (KOL), iron ore (BHP), and the base metals (CU).

Demand for oil (USO) grows, as energy starved India is one of the world?s largest importers.

A strengthening Rupee, higher standards of living, and relaxed import duties should give a much needed boost for gold (GLD). India has always been the world?s largest buyer.

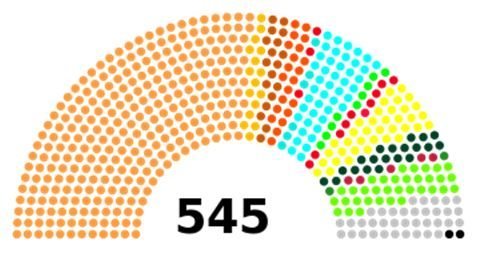

The world?s largest democracy certainly delivers the most unusual of elections, a blend of practices from today?.and a thousand years ago. It was carried out over five weeks, and a stunning 541 million voted, out of an eligible 815 million, a turnout of 66.4%. That is far higher than elections seen here in the United States.

Of the 552 members in the Lok Sabha, the lower house (or their House of Representatives), a specific number of seats are reserved for scheduled castes, scheduled tribes, and women. Gee, I wonder which one of these I would fit in?

Important issues during the campaign included rising prices, the economy, security, and infrastructure such as roads, electricity and water. About 14% of voters cited corruption as the main issue.

Some 12 political parties ran candidates. The winner was Hindu Nationalist Narendra Modi of the Bharatiya Janata Party (BJP), who led a diverse collection of lesser parties to take an overwhelming majority. For more details on this fascinating election, please click here at http://www.ndtv.com/elections.

It is still early days for the Bombay stock market, which has already rocketed by a stunning 20% since the election results became obvious last week.

This could be the beginning of a ten-bagger move over coming decades. Managers are hurriedly pawing through stacks of research on the subcontinent they have been ignoring for the past four years, the last time emerging markets peaked.

In the meantime, the action has spilled over into other emerging markets (EEM), their currencies (CEW), and their bonds (ELD), which have all punched through to new highs for the year.

I?ll be knocking out research o specific names when I find them. Until then, use any dip to pick up the Indian ETF?s (INP), (PIN), and (EPI).

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/India-Election-Results.jpg254477Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-24 01:03:152015-02-24 01:03:15The Game Changer in India

We have several options positions that expire on Friday, and I just want to explain to the newbies how to best maximize their profits.

These include:

The Currency Shares Japanese Yen Trust (FXY) February $84-$87 vertical bear put spread

The Gilead Sciences (GILD) February $87.50-$92.50 vertical bull call spread

The S&P 500 (SPY) February $199-$202 vertical bull call spread

My bets that (GILD) and the (SPY) would rise, and that the (FXY) would fall during January and February proved dead on accurate. We got a further kicker with the two stock positions in that we captured a dramatic plunge in volatility (VIX).

Provided that some 9/11 type event doesn?t occur today, all three positions should expire at their maximum profit point. In that case, your profits on these positions will amount to 13% for the (FXY), 19% for (GILD) and 20% for the (SPY).

This will bring us a fabulous 5.58% profit so far for February, and a market beating 6.11% for year-to-date 2015.

Many of you have already emailed me asking what to do with these winning positions. The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck and pat yourself on the back for a job well done. You don?t have to do anything.

Your broker (are they still called that?) will automatically use your long put position to cover the short put position, cancelling out the total holding. Ditto for the call spreads. The profit will be credited to your account on Monday morning, and he margin freed up.

If you don?t see the cash show up in you account on Monday, get on the blower immediately. Although the expiration process is now supposed to be fully automated, occasionally mistakes do occur. Better to sort out any confusion before losses ensue.

I don?t usually run positions into expiration like this, preferring to take profits two weeks ahead of time, as the risk reward is no longer that favorable.

But we have a ton of cash right now, and I don?t see any other great entry points for the moment. Better to keep the cash working and duck the double commissions. This time being a pig paid off handsomely.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. Keep in mind that the liquidity in the options market disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration. This is known in the trade as the ?expiration risk.?

One way or the other, I?m sure you?ll do OK, as long as I am looking over your shoulder, as I will be.

This expiration will leave me with a very rare 100% cash position. I am going to hang back and wait for good entry points before jumping back in. It?s all about getting that ?buy low, sell high? thing going again.

There are already interesting trades setting up in bonds (TLT), the (SPY), the Russell 2000 (IWM), NASDAQ (QQQ), solar stocks (SCTY), oil (USO), and gold (GLD).

The currencies seem to have gone dead for the time being, so I?ll stay away.

Well done, and on to the next trade.

Pat Yourself on the Back

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Pat-on-the-back-e1424375419249.jpg259400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-20 01:04:322015-02-20 01:04:32A Note on the Friday Options Expiration

For the last few months, I have leapt off my biweekly global strategy webinars to check the weekly crude inventories announced minutes before. This week?s figures absolutely blew me away.

The American Petroleum Institute reported that crude stocks rose a staggering 14.3 million barrels over the past week. This is the biggest weekly build that I can remember after covering the industry for 45 years.

This comes on the heels of a breathtaking build of 6.1 million barrels the previous week.

Will someone please text me when the numbers come out during my next webinar? I hate being in the dark, even when it is just for 20 minutes.

Needless to say, crude prices (USO) fell like a stone, giving up 5.5% in hours. Prices are still plunging as I write this. It confirms my suspicion, voiced assiduously in the earlier webinar, that Texas tea has another run to the downside in store.

The 500,000 barrels a day of new production coming on line over the next four months make this a virtual certainty.

The implications for your investment portfolio are legion.

It means that a new leg down in the oil collapse is now unfolding. We may be in the process of taking another shot at the $43 low in January. Best case, this sets up the double bottom where you should buy the entire energy and commodity sectors. Worse case, we break to a new low in the $30?s.

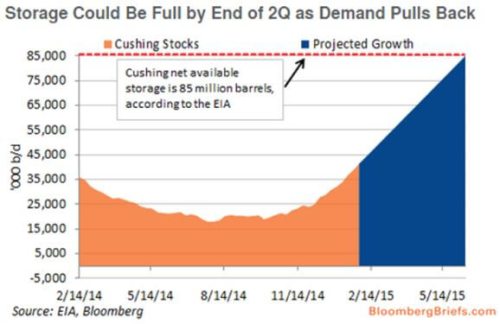

Industry experts are keeping a laser like focus on the storage facilities at Cushing, Oklahoma. They are rapidly filling up, and will be full at 85 million barrels by June. Today?s numbers bring that day dramatically forward.

Once topped up, the industry could be facing a price Armageddon, and newly produced crude will have nowhere to go.

That will bring widespread capping of producing wells, which are never able to recover production when restored. This will be a terrible outcome for the producing companies and oil lease investors.

Consumers aren?t the only ones who are celebrating.

Oil traders are enjoying their best year since 2009, cashing in on the sky high volatility. Front month volatility is gyrating around the 55% levels. This compares to only 15.45% for the S&P 500.

Traders, eat your hearts out.

Big players like Glencore, Gunvor and Mercuria are cashing in with lower prices vastly offset by much greater turnover. Specialized energy hedge funds are also doing well.

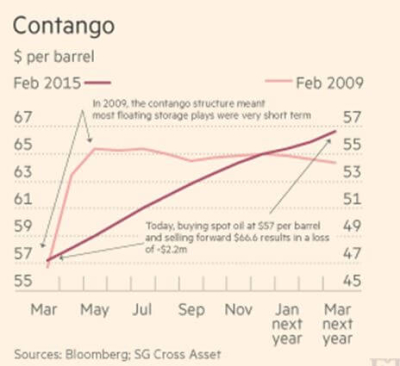

The contango, whereby futures contracts for far month delivery are trading at huge premiums to front month ones, is also generating enormous trading opportunities.

The last time I checked, oil one-year out was trading at a 25% premium. This means you can buy a few hundred thousand barrels, charter a rusted out old tanker, and store it for future sale.

Ultra low interest rates to finance the position provide an additional kicker. Hedge funds with the right credit lines are pouring into the field.

OK, so you?re not set up to borrow billions, charter ships, and swing around huge amounts of crude. Nor am I, for that matter. However, the next best thing is also setting up.

When oil completes its next swan dive, there will be great opportunities in the options market.

One year dated calls on oil majors like Exxon (XOM), Conoco Phillips (COP) and Occidental Petroleum (OXY) and the oil ETF (USO) should rise tenfold in the next recovery if you are able to buy anywhere close to the bottom.

I?ll send out a Trade Alert when I see it.

I Think I See a Spot Over There

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Oil-Storage-e1424354835281.jpg249400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-19 09:20:352015-02-19 09:20:35The Best is yet to Come in Crude

I?m really glad I watched the Super Bowl yesterday. Not only was it a great warm-up for next year?s championship game, which will be in my hometown of San Francisco. I also witnessed the worst coaching call in football history.

The Seattle Seahawks had the game in the bag. All they had to do was move the ball one foot over two tries at the goal line. Instead, they passed? Too bad I wasn?t able to find a bookie to take a last minute six-figure bet. I expected New England to win.

I have to tell you that I sympathize with Seahawks Coach Peter Carroll. For I sent out one of the worst recommendations in trading history with my BUY of master limited partnership Linn Energy (LINE) on December 1.

I then proceeded to break every rule in the trader?s handbook on how to manage this position. The errors were so many that I have to list them:

1) I scored the instant profit I was looking for, making 80 basis points within two days. I didn?t take it. Instead I got greedy, hanging on for more. It never showed.

2) I then ignored my own stop loss at $15, even though most of you bailed out then and there.

3) I then committed anther sin, waiting for the units to get back to my cost to get out, even though I constantly admonish followers never to do this. The market doesn?t care what your cost is. The market is the market. It has zero memory, and could care less who you are.

4) There were several substantial rallies that I could have sold into for a much smaller loss, to $14.80, $11.90 and $11.70. I didn?t. The ?getting out for even? syndrome strikes again.

5) I expected oil to bottom out in the low $60?s, which was much lower than most people?s targets. It didn?t. Instead, it dropped another $20 to the $43 handle. Once there is a glut of oil, there is no place to put it, as all storage is full, so it always plunges lower than you expect. With more oil industry experience than most traders, I already knew this. But I ignored the writing on the wall.

6) I waited for a yearend short covering rally to take me out of the position. It never showed. Instead, it went down faster, hitting a new five year low of $9.30.

7) I waited for a New Year rally to take me out. Ditto.

At this point, (LINN) is acting like a classic busted stock. Even though oil has bounced back by a hefty 15% in recent days, (LINN) has barely moved. If you throw good news on a stock and it doesn?t move, it is time to say hasta la vista baby.

For more depth on the grim outlook for Texas tea, please read my recent piece, ?More Pain to Come in Oil? by clicking here. Now is not the time to maintain an aggressive long in energy.

I?m sure (LINN) will come back some day, as it is well managed. In fact, it might even be the big trade of the year. But this could happen in months, or even years. And if you haven?t noticed, the name of this service is the Diary of a Mad Hedge Fund Trader, not the Diary of a Mad Long Term Investor.

Where I live, long-term is a long-winded way of saying "wrong".

Can I Interest You in Some Linn Energy?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Pete-Carroll-e1422911237298.jpg400279Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-03 01:05:132015-02-03 01:05:13How to Lose Money

There are very few people I will drop everything to listen to. One of the handful is Daniel Yergin, the bookish founder and CEO of Cambridge Energy Research Associates, the must-go-to source for all things energy.

Daniel received a Pulitzer Prize for The Prize: The Epic Quest for Oil, Money, and Power, a rare feat for a non-fiction book (I?ve never been able to get one).

Suffice it to say that every professional in the oil industry, and not a few hedge fund traders, have devoured this riveting book and based their investment decisions upon it.

Yergin thinks that the fracking and horizontal drilling revolutions have made the United States the new swing producer of oil. There is so much money in the investment pipeline that American oil production will continue to increase for the next six months, by some 500,000 barrels a day.

This new supply will run head on into the seasonal drop in demand for energy, when spring ritually reduces heating bills, but the need for air-conditioning has not yet kicked in.

The net net could be a further drop in the price for Texas tea from the present $45 a barrel, possibly a dramatic one.

Yergin isn?t predicting any specific oil price as a potential floor, as it is an impossible task. While OPEC was a monolithic cartel, the US fracking industry is made up of thousands of mom and pop operators, and no one knows what anyone else is doing. However, he is willing to bet that the price of oil will be higher in a year.

Currently, the 91 million barrel global market for oil is oversupplied with 1 million barrels a day. That includes the 2 million b/d that has been lost from disruptions in Libya, Syria and Iraq.

If the International Monetary Fund is right, and the world adds 3.8% in economic growth this year, we will soak up 1.1 million b/d of that with new demand. In the end, the oil price collapse is a self-solving problem. The new economic growth engendered by ultra low fuel prices eventually drives prices higher.

Where we reach the tipping point, and the oil market comes back into balance, is anyone?s guess. But when it does, prices will go substantially higher. The cure for low prices is low prices.

The bottom line is that there will be a great time to buy oil companies, but it is not yet.

What we are witnessing now is the worst energy crash since the 1980?s, when new supplies from the North Sea, Mexico and Alaska all hit at the same time. The price of oil eventually crashed from $42 to $8.

I remember it well, because Morgan Stanley then set up a private partnership that bought commercial real estate in Houston for ten cents on the dollar. The eventual return on this fund was over 1,000%.

This time it is more complicated. Prices lived over $100 for so long that it sucked in an unprecedented amount of capital into new drilling, some $100 billion worth. As a result, sources were brought online from parts of the world as diverse as Russia, the Arctic, Central Asia, Africa, the Canadian tar sands and remote and very expensive offshore platforms.

Yergin believes that Saudi Arabia can survive for three years with prices at current levels. After that, it will burn through its $150 billion of foreign exchange reserves, and could face a crisis. Clearly, the Kingdom is betting that prices will recover with its market share based strategy before then. They are playing for the long haul.

The transition of power to the new King Salman was engineered by a committee of senior family members, and has been very orderly. However, King Salman, a Sunni, will have his hands full. The current takeover of Yemen by a hostile Shiite minority, the Houthis, is a major concern. Yemen shares a 1,100 mile border with Saudi Arabia.

Daniel says that a year ago, there was a lot of geopolitical risk priced into oil, with multiple crises in the Ukraine, Syria, Libya and Iraq frightening consumers, so trading levitated over $100 for years. Delta Airlines Inc. (DAL) even went to the length of buying its own refiner to keep fuel prices from rising further.

US oil producers have a unique advantage over competitors in that they can cut costs faster than any other competitors in the world. On the other hand, they are eventually going head to head against the Saudis, whose average cost of production is a mere $5/barrel.

A native of my own hometown of Los Angeles, Yergin started his professional career as a lecturer at Harvard University. He founded Cambridge Energy in 1982 with a $7.00 investment in a file cabinet at the Good Will. He later sold Cambridge Energy to the consulting group IHS Inc. for a small fortune.

To buy The Prize at discount Amazon pricing, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/The-Prize-e1422373144707.jpg480320Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-27 10:53:482015-01-27 10:53:48More Pain to Come in Oil

Mad Day Trader Jim Parker is expecting the first quarter of 2015 to offer plenty of volatility and loads of great trading opportunities. He thinks the scariest moves may already be behind us.

After a ferocious week of decidedly ?RISK OFF? markets, the sweet spots going forward will be of the ?RISK ON? variety. Sector leadership could change daily, with a brutal rotation, depending on whether the price of oil is up, down, or sideways.

The market is paying the price of having pulled forward too much performance from 2015 back into the final month of 2014, when we all watched the December melt up slack jawed.

Jim is a 40-year veteran of the financial markets and has long made a living as an independent trader in the pits at the Chicago Mercantile Exchange. He worked his way up from a junior floor runner to advisor to some of the world?s largest hedge funds. We are lucky to have him on our team and gain access to his experience, knowledge and expertise.

Jim uses a dozen proprietary short-term technical and momentum indicators to generate buy and sell signals. Below are his specific views for the new quarter according to each asset class.

Stocks

The S&P 500 (SPY) and NASDAQ have met all of Jim?s short-term downside targets, and a sustainable move up from here is in the cards. But if NASDAQ breaks 4,100 to the downside, all bets are off.

His favorite sector is health care (XLV), which seems immune to all troubles, and may have already seen its low for the year. Jim is also enamored with technology stocks (XLK).

The coming year will be a great one for single stock pickers. Priceline (PCLN) is a great short, dragged down by the weak Euro, where they get much of their business. Ford Motors (F) probably bottomed yesterday, and is a good offsetting long.

Bonds

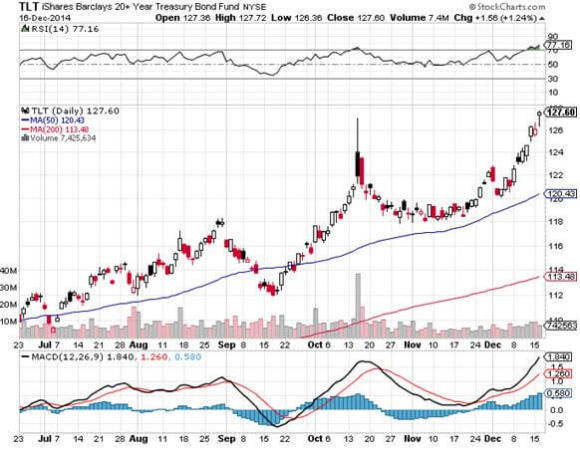

Jim is not inclined to stand in front of a moving train, so he likes the Treasury bond market (TLT), (TBT). He thinks the 30-year yield could reach an eye popping 2.25%. A break there is worth another 10 basis points. Bonds are getting a strong push from a flight to safety, huge US capital inflows, and an endlessly strong dollar.

Foreign Currencies

A short position in the Euro (FXE), (EUO) is the no brainer here. The problem is one of good new entry points. Real traders always have trouble selling into a free fall. But you might see profit taking as we approach $1.16 in the cash market.

The Aussie (FXA) is being dragged down by the commodity collapse and an indifferent government. The British pound (FXB) is has yet to recover from the erosion of confidence ignited by the Scotland independence vote and has further mud splattered upon it by the weak Euro.

Precious Metals

GOLD (GLD) could be in a good range pivoting off of the recent $1,140 bottom. The gold miners (GDX) present the best opportunity at catching some volatility. The barbarous relic is pulling up the price of silver (SLV) as well. Buy the hard breaks, and then take quick profits. In a deflationary world, there is no long-term trade here. It is a real field of broken dreams.

Energy

Jim is not willing to catch a falling knife in the oil space (USO). He has too few fingers as it is. It has become too difficult to trade, as the algorithms are now in charge, and a lot of gap moves take place in the overnight markets. Don?t bother with fundamentals as they are irrelevant. No one really knows where the bottom in oil is.

Agriculturals

Jim is friendly to the ags (CORN), (SOYB), (DBA), but only on sudden pullbacks. However, there are no new immediate signals here. So he is just going to wait. The next directional guidance will come with the big USDA report at the end of January. The ags are further clouded by a murky international picture, with the collapse of the Russian ruble allowing the rogue nation to undercut prices on the international market.

Volatility

Volatility (VIX), (VXX) is probably going to peak out her soon in the $23-$25 range. The next week or so will tell for sure. A lot hangs on Friday?s December nonfarm payroll report. Every trader out there remembers that the last three visits to this level were all great shorts. However, the next bottom will be higher, probably around the $16 handle.

If you are not already getting Jim?s dynamite Mad Day Trader service, please get yourself the unfair advantage you deserve. Just email Nancy in customer support at support@madhedgefundtrader.com and ask for the $1,500 a year upgrade to your existing Global Trading Dispatch service.

Volatility Weekly

Volatility Monthly

Euro to the Dollar

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/Volatility-Weekly.jpg325579Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-08 09:44:082015-01-08 09:44:08Mad Day Trader Jim Parker?s Q1, 2015 Views

I am once again writing this report from a first class sleeping cabin on Amtrak?s California Zephyr. By day, I have two comfortable seats facing each other next to a broad window. At night, they fold into bunk beds, a single and a double. There is a shower, but only Houdini could get in and out of it.

We are now pulling away from Chicago?s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I am headed for Emeryville, California, just across the bay from San Francisco. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure, and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Spellchecker can catch most of the mistakes, but not all of them. Thank goodness for small algorithms.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied searches during stops at major stations along the way to chase down data points.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS. Who knew that 95% of America is off the grid? That explains a lot about our politics today. I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone.

After making the rounds with strategists, portfolio managers, and hedge fund traders, I can confirm that 2014 was one of the toughest to trade for careers lasting 30, 40, or 50 years. Yet again, the stay at home index players have defeated the best and the brightest.

With the Dow gaining a modest 8% in 2014, and S&P 500 up a more virile 14.2%, this was a year of endless frustration. Volatility fell to the floor, staying at a monotonous 12% for seven boring consecutive months. Most hedge funds lagged the index by miles.

My Trade Alert Service, hauled in an astounding 30.3% profit, at the high was up 42.7%, and has become the talk of the hedge fund industry. That was double the S&P 500 index gain.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

The Ten Highlights of 2015

1) Stocks will finish 2015 higher, almost certainly more than the previous year, somewhere in the 10-15% range. Cheap energy, ultra low interest rates, and 3-4% GDP growth, will expand multiples. It?s Goldilocks with a turbocharger.

2) Performance this year will be back-end loaded into the fourth quarter, as it was in 2014. The path forward became so clear, that some of 2015?s performance was pulled forward into November, 2014.

3) The Treasury bond market will modestly grind down, anticipating the inevitable rate rise from the Federal Reserve.

4) The yen will lose another 10%-20% against the dollar.

5) The Euro will fall another 10%, doing its best to hit parity with the greenback, with the assistance of beleaguered continental governments.

6) Oil stays in a $50-$80 range, showering the economy with hundreds of billions of dollars worth of de facto tax cuts.

7) Gold finally bottoms at $1,000 after one more final flush, then rallies (My jeweler was right, again).

8) Commodities finally bottom out, thanks to new found strength in the global economy, and begin a modest recovery.

9) Residential real estate has made its big recovery, and will grind up slowly from here.

10) After a tumultuous 2014, international political surprises disappear, the primary instigators of trouble becalmed by collapsed oil revenues.

The Thumbnail Portfolio

Equities - Long. A rising but low volatility year takes the S&P 500 up to 2,350. This year we really will get another 10% correction. Technology, biotech, energy, solar, and financials lead.

Bonds - Short. Down for the entire year with long periods of stagnation.

Foreign Currencies - Short. The US dollar maintains its bull trend, especially against the Yen and the Euro.

Commodities - Long. A China recovery takes them up eventually.

Precious Metals - Stand aside. We get the final capitulation selloff, then a rally.

Agriculture - Long. Up, because we can?t keep getting perfect weather forever.

Real estate - Long. Multifamily up, commercial up, single family homes sideways to up small.

1) The Economy - Fortress America

This year, it?s all about oil, whether it stays low, shoots back up, or falls lower. The global crude market is so big, so diverse, and subject to so many variables, that it is essentially unpredictable.

No one has an edge, not the major producers, consumers, or the myriad middlemen. For proof, look at how the crash hit so many ?experts? out of the blue.

This means that most economic forecasts for the coming year are on the low side, as they tend to be insular and only examine their own back yard, with most predictions still carrying a 2% handle.

I think the US will come in at the 3%-4% range, and the global recovery spawns a cross leveraged, hockey stick effect to the upside. This will be the best performance in a decade. Most company earnings forecasts are low as well.

There is one big positive that we can count on in the New Year. Corporate earnings will probably come in at $130 a share for the S&P 500, a gain of 10% over the previous year. During the last five years, we have seen the most dramatic increase in earnings in history, taking them to all-time highs.

This is set to continue. Furthermore, this growth will be front end loaded into Q1. The ?tell? was the blistering 5% growth rate we saw in Q3, 2014.

Cost cutting through layoffs is reaching an end, as there is no one left to fire. That leaves hyper accelerating technology and dramatically lower energy costs the remaining sources of margin increases, which will continue their inexorable improvements. Think of more machines and software replacing people.

You know all of those hundreds of billions raised from technology IPO?s in 2014. Most of that is getting plowed right back into new start ups, accelerating the rate of technology improvements even further, and the productivity gains that come with it.

You can count on demographics to be a major drag on this economy for the rest of the decade. Big spenders, those in the 46-50 age group, don?t return in large numbers until 2022.

But this negative will be offset by a plethora of positives, like technology, global expansion, and the lingering effects of Ben Bernanke?s massive five year quantitative easing. A time to pay the piper for all of this largess will come. But it could be a decade off.

I believe that the US has entered a period of long-term structural unemployment similar to what Germany saw in the 1990?s. Yes, we may grind down to 5%, but no lower than that. Keep close tabs on the weekly jobless claims that come out at 8:30 AM Eastern every Thursday for a good read as to whether the financial markets will head in a ?RISK ON? or ?RISK OFF? direction.

Most of the disaster scenarios predicted for the economy this year were based on the one off black swans that never amounted to anything, like the Ebola virus, ISIS, and the Ukraine.

With the economy going gangbusters, and corporate earnings reaching $130 a share, those with a traditional ?buy and hold? approach to the stock market will do alright, provided they are willing to sleep through some gut churning volatility. A Costco sized bottle of Jack Daniels and some tranquillizers might help too.

Earnings multiples will increase as well, as much as 10%, from the current 17X to 18.5X, thanks to a prolonged zero interest rate regime from the Fed, a massive tax cut in the form of cheap oil, unemployment at a ten year low, and a paucity of attractive alternative investments.

This is not an outrageous expectation, given the 10-22 earnings multiple range that we have enjoyed during the last 30 years. If anything, it is amazing how low multiples are, given the strong tailwinds the economy is enjoying.

The market currently trades around fair value, and no market in history ever peaked out here. An overshoot to the upside, often a big one, is mandatory. After all, my friend, Janet Yellen, is paying you to buy stock with cheap money, so why not?

This is how the S&P 500 will claw its way up to 2,350 by yearend, a gain of about 12.2% from here. Throw in dividends, and you should pick up 14.2% on your stock investments in 2015.

This does not represent a new view for me. It is simply a continuation of the strategy I outlined again in October, 2014 (click here for ?Why US Stocks Are Dirt Cheap?).

Technology will be the top-performing sector once again this year. They will be joined by consumer cyclicals (XLV), industrials (XLI), and financials (XLF).

The new members in the ?Stocks of the Month Club? will come from newly discounted and now high yielding stocks in the energy sector (XLE).

There is also a rare opportunity to buy solar stocks on the cheap after they have been unfairly dragged down by cheap oil like Solar City (SCTY) and the solar basket ETF (TAN). Revenues are rocketing and costs are falling.

After spending a year in the penalty box, look for small cap stocks to outperform. These are the biggest beneficiaries of cheap energy and low interest rates, and also have minimal exposure to the weak European and Asian markets.

Share prices will deliver anything but a straight-line move. We finally got our 10% correction in 2014, after a three-year hiatus. Expect a couple more in 2015. The higher prices rise, the more common these will become.

We will start with a grinding, protesting rally that takes us up to new highs, as the market climbs the proverbial wall of worry. Then we will suffer a heart stopping summer selloff, followed by another aggressive yearend rally.

Cheap money creates a huge incentive for companies to buy back their own stock. They divert money from their $3 trillion cash hoard, which earns nothing, retire shares paying dividends of 3% or more, and boost earnings per share without creating any new business. Call it financial engineering, but the market loves it.

Companies are also retiring stock through takeovers, some $2 trillion worth last year. Expect more of this to continue in the New Year, with a major focus on energy. Certainly, every hedge fund and activist investor out there is undergoing a crash course on oil fundamentals. After a 13-year bull market in energy, the industry is ripe for a cleanout.

This is happening in the face of both an individual and institutional base that is woefully underweight equities.

The net net of all of this is to create a systemic shortage of US equities. That makes possible simultaneous rising prices and earnings multiples that have taken us to investor heaven.

Amtrak needs to fill every seat in the dining car, so you never know who you will get paired with.

There was the Vietnam vet Phantom jet pilot who now refused to fly because he was treated so badly at airports. A young couple desperate to get out of Omaha could only afford seats as far as Salt Lake City, sitting up all night. I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a ?See America Pass.? Mennonites returning home by train because their religion forbade airplanes.

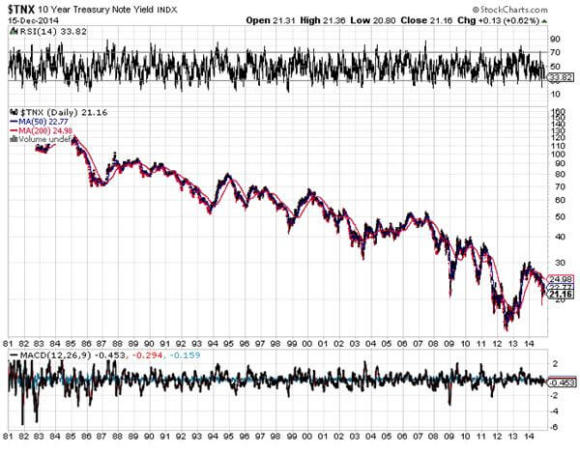

If you told me that US GDP growth was 5%, unemployment was at a ten year low at 5.8%, and energy prices had just halved, I would have pegged the ten-year Treasury bond yield at 6.0%. Yet here we are at 2.10%.

Virtually every hedge fund manager and institutional investor got bonds wrong last year, expecting rates to rise. I was among them, but that is no excuse. At least I have good company.

You might as well take your traditional economic books and throw them in the trash. Apologies to John Maynard Keynes, John Kenneth Galbraith, and Paul Samuelson.

The reasons for the debacle are myriad, but global deflation is the big one. With ten year German bunds yielding a paltry 50 basis points, and Japanese bonds paying a paltry 30 basis points, US Treasuries are looking like a bargain.

To this, you can add the greater institutional bond holding requirements of Dodd-Frank, a balancing US budget deficit, a virile US dollar, the commodity price collapse, and an enormous embedded preference for investors to keep buying whatever worked yesterday.

For more depth on the perennial strength of bonds, please click here for ?Ten Reasons Why I?m Wrong on Bonds?.

Bond investors today get an unbelievable bad deal. If they hang on to the longer maturities, they will get back only 80 cents worth of purchasing power at maturity for every dollar they invest.

But institutions and individuals will grudgingly lock in these appalling returns because they believe that the potential losses in any other asset class will be worse. The problem is that driving eighty miles per hour while only looking in the rear view mirror can be hazardous to your financial health.

While much of the current political debate centers around excessive government borrowing, the markets are telling us the exact opposite. A 2%, ten-year yield is proof to me that there is a Treasury bond shortage, and that the government is not borrowing too much money, but not enough.

There is another factor supporting bonds that no one is looking at. The concentration of wealth with the 1% has a side effect of pouring money into bonds and keeping it there. Their goal is asset protection and nothing else.

These people never sell for tax reasons, so the money stays there for generations. It is not recycled into the rest of the economy, as conservative economists insist. As this class controls the bulk of investable assets, this forestalls any real bond market crash, possibly for decades.

So what will 2015 bring us? I think that the erroneous forecast of higher yields I made last year will finally occur this year, and we will start to chip away at the bond market bubble?s granite edifice. I am not looking for a free fall in price and a spike up in rates, just a move to a new higher trading range.

The high and low for ten year paper for the past nine months has been 1.86% to 3.05%. We could ratchet back up to the top end of that range, but not much higher than that. This would enable the inverse Treasury bond bear ETF (TBT) to reverse its dismal 2014 performance, taking it from $46 back up to $76.

You might have to wait for your grandchildren to start trading before we see a return of 12% Treasuries, last seen in the early eighties. I probably won?t live that long.

Reaching for yield will continue to be a popular strategy among many investors, which is typical at market tops. That focuses buying on junk bonds (JNK) and (HYG), REITS (HCP), and master limited partnerships (KMP), (LINE).

There is also emerging market sovereign debt to consider (PCY). At least there, you have the tailwinds of long term strong economies, little outstanding debt, appreciating currencies, and higher interest rates than those found at home. This asset class was hammered last year, so we are now facing a rare entry point. However, keep in mind, that if you reach too far, your fingers get chopped off.

There is a good case for sticking with munis. No matter what anyone says, taxes are going up, and when they do, this will increase tax free muni values. So if you hate paying taxes, go ahead and buy this exempt paper, but only with the expectation of holding it to maturity. Liquidity could get pretty thin along the way, and mark to markets could be shocking. Be sure to consult with a local financial advisor to max out the state, county, and city tax benefits.

There are only three things you need to know about trading foreign currencies in 2015: the dollar, the dollar, and the dollar. The decade long bull market in the greenback continues.

The chip shot here is still to play the Japanese yen from the short side. Japan?s Ministry of Finance is now, far and away, the most ambitious central bank hell bent on crushing the yen to rescue its dying economy.

The problems in the Land of the Rising Sun are almost too numerous to count: the world?s highest debt to GDP ratio, a horrific demographic problem, flagging export competitiveness against neighboring China and South Korea, and the world?s lowest developed country economic growth rate.

The dramatic sell off we saw in the Japanese currency since December, 2012 is the beginning of what I believe will be a multi decade, move down. Look for ?125 to the dollar sometime in 2015, and ?150 further down the road. I have many friends in Japan looking for and overshoot to ?200. Take every 3% pullback in the greenback as a gift to sell again.

With the US having the world?s strongest major economy, its central bank is, therefore, most likely to raise interest rates first. That translates into a strong dollar, as interest rate differentials are far and away the biggest decider of the direction in currencies. So the dollar will remain strong against the Australian and Canadian dollars as well.

The Euro looks almost as bad. While European Central Bank president, Mario Draghi, has talked a lot about monetary easing, he now appears on the verge of taking decisive action.

Recurring financial crisis on the continent is forcing him into a massive round of Fed style quantitative easing through the buying of bonds issued by countless European entities. The eventual goal is to push the Euro down to parity with the buck and beyond.

For a sleeper, use the next plunge in emerging markets to buy the Chinese Yuan ETF (CYB) for your back book, but don?t expect more than single digit returns. The Middle Kingdom will move heaven and earth in order to keep its appreciation modest to maintain their crucial export competitiveness.

There isn?t a strategist out there not giving thanks for not loading up on commodities in 2014, the preeminent investment disaster of 2015. Those who did are now looking for jobs on Craig?s List.

2014 was the year that overwhelming supply met flagging demand, both in Europe and Asia. Blame China, the big swing factor in the global commodity.

The Middle Kingdom is currently changing drivers of its economy, from foreign exports to domestic consumption. This will be a multi decade process, and they have $4 trillion in reserves to finance it.

It will still demand prodigious amounts of imported commodities, especially, oil, copper, iron ore, and coal, all of which we sell. But not as much as in the past. The derivative equity plays here, Freeport McMoRan (FCX) and Companhia Vale do Rio Doce (VALE), have all taken an absolute pasting.

The food commodities were certainly the asset class to forget about in 2014, as perfect weather conditions and over planting produced record crops for the second year in a row, demolishing prices. The associated equity plays took the swan dive with them.

However, the ags are still a tremendous long term Malthusian play. The harsh reality here is that the world is making people faster than the food to feed them, the global population jumping from 7 billion to 9 billion by 2050.

Half of that increase comes in countries unable to feed themselves today, largely in the Middle East. The idea here is to use any substantial weakness, as we are seeing now, to build long positions that will double again if global warming returns in the summer, or if the Chinese get hungry.

The easy entry points here are with the corn (CORN), wheat (WEAT), and soybeans (SOYB) ETF?s. You can also play through (MOO) and (DBA), and the stocks Mosaic (MOS), Monsanto (MON), Potash (POT), and Agrium (AGU).

The grain ETF (JJG) is another handy fund. Though an unconventional commodity play, the impending shortage of water will make the energy crisis look like a cakewalk. You can participate in this most liquid of assets with the ETF?s (PHO) and (FIW).

Yikes! What a disaster! Energy in 2014 suffered price drops of biblical proportions. Oil lost the $30 risk premium it has enjoyed for the last ten years. Natural gas got hammered. Coal disappeared down a black hole.

Energy prices did this in the face of an American economy that is absolutely rampaging, its largest consumer. Our train has moved over to a siding to permit a freight train to pass, as it has priority on the Amtrak system. Three Burlington Northern engines are heaving to pull over 100 black, brand new tank cars, each carrying 30,000 gallons of oil from the fracking fields in North Dakota.

There is another tank car train right behind it. No wonder Warren Buffett tap dances to work every day, as he owns the road. US Steel (X) also does the two-step, since they provide immense amounts of steel to build these massive cars.

The US energy boom sparked by fracking will be the biggest factor altering the American economic landscape for the next two decades. It will flip us from a net energy importer to an exporter within two years, allowing a faster than expected reduction in military spending in the Middle East.

Cheaper energy will bestow new found competitiveness on US companies that will enable them to claw back millions of jobs from China in dozens of industries. This will end our structural unemployment faster than demographic realities would otherwise permit.

We have a major new factor this year in considering the price of energy. Peace in the Middle East, especially with Iran, always threatened to chop $30 off the price of Texas tea. But it was a pie-in-the-sky hope. Now there are active negotiations underway in Geneva for Iran to curtail or end its nuclear program. This could be one of the black swans of 2015, and would be hugely positive for risk assets everywhere.

Enjoy cheap oil while it lasts because it won?t last forever. American rig counts are already falling off a cliff and will eventually engineer a price recovery.

Add the energies of oil (DIG), Cheniere Energy (LNG), the energy sector ETF (XLE), Conoco Phillips (COP), and Occidental Petroleum (OXY). Skip natural gas (UNG) price plays and only go after volume plays, because the discovery of a new 100-year supply from ?fracking? and horizontal drilling in shale formations is going to overhang this subsector for a very long time.

It is a basic law of economics that cheaper prices bring greater demand and growing volumes, which have to be transported. However, major reforms are required in Washington before use of this molecule goes mainstream.

These could be your big trades of 2015, but expect to endure some pain first.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders. The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a train over on to its side.

In the snow filled canyons we sight a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It?s a good omen for the coming year. We also see countless abandoned gold mines and the broken down wooden trestles leading to them, so it is timely here to speak about precious metals.

As long as the world is clamoring for paper assets like stocks and bonds, gold is just another shiny rock. After all, who needs an insurance policy if you are going to live forever?

We have already broken $1,200 once, and a test of $1,000 seems in the cards before a turnaround ensues. There are more hedge fund redemptions and stop losses to go. The bear case has the barbarous relic plunging all the way down to $700.

But the long-term bull case is still there. Someday, we are going to have to pay the piper for the $4.5 trillion expansion in the Fed?s balance sheet over the past five years, and inflation will return. Gold is not dead; it is just resting. I believe that the monetary expansion arguments to buy gold prompted by massive quantitative easing are still valid.

If you forgot to buy gold at $35, $300, or $800, another entry point is setting up for those who, so far, have missed the gravy train. The precious metals have to work off a severely, decade old overbought condition before we make substantial new highs. Remember, this is the asset class that takes the escalator up and the elevator down, and sometimes the window.

If the institutional world devotes just 5% of their assets to a weighting in gold, and an emerging market central bank bidding war for gold reserves continues, it has to fly to at least $2,300, the inflation adjusted all-time high, or more.

This is why emerging market central banks step in as large buyers every time we probe lower prices. For me, that pegs the range for 2015 at $1,000-$1,400. ETF players can look at the 1X (GLD) or the 2X leveraged gold (DGP).

I would also be using the next bout of weakness to pick up the high beta, more volatile precious metal, silver (SLV), which I think could hit $50 once more, and eventually $100.

What will be the metals to own in 2015? Palladium (PALL) and platinum (PPLT), which have their own auto related long term fundamentals working on their behalf, would be something to consider on a dip. With US auto production at 17 million units a year and climbing, up from a 9 million low in 2009, any inventory problems will easily get sorted out.

Would You Believe This is a Blue State?

8) Real Estate (ITB)

The majestic snow covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write. My apologies to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebears in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80.

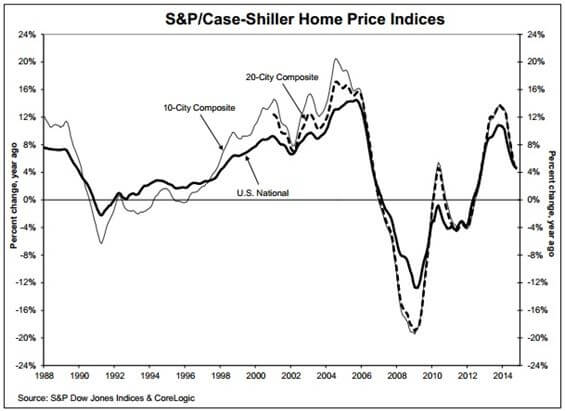

There is no doubt that there is a long-term recovery in real estate underway. We are probably 8 years into an 18-year run at the next peak in 2024.

But the big money has been made here over the past two years, with some red hot markets, like San Francisco, soaring. If you live within commuting distance of Apple (AAPL), Google (GOOG), or Facebook (FB) headquarters in California, you are looking at multiple offers, bidding wars, and prices at all time highs.

From here on, I expect a slow grind up well into the 2020?s. If you live in the rest of the country, we are talking about small, single digit gains. The consequence of pernicious deflation is that home prices appreciate at a glacial pace. At least, it has stopped going down, which has been great news for the financial industry.

There are only three numbers you need to know in the housing market: there are 80 million baby boomers, 65 million Generation Xer?s who follow them, and 85 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xer?s since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made.

If they have prospered, banks won?t lend to them. Brokers used to say that their market was all about ?location, location, location?. Now it is ?financing, financing, financing?. Banks have gone back to the old standard of only lending money to people who don?t need it.

Consider the coming changes that will affect this market. The home mortgage deduction is unlikely to survive any real attempt to balance the budget. And why should renters be subsidizing homeowners anyway? Nor is the government likely to spend billions keeping Fannie Mae and Freddie Mac alive, which now account for 95% of home mortgages.

That means the home loan market will be privatized, leading to mortgage rates higher than today. It is already bereft of government subsidies, so loans of this size are priced at premiums. This also means that the fixed rate 30-year loan will go the way of the dodo, as banks seek to offload duration risk to consumers. This happened long ago in the rest of the developed world.

There is a happy ending to this story. By 2022 the Millennials will start to kick in as the dominant buyers in the market. Some 85 million Millennials will be chasing the homes of only 65 Gen Xer?s, causing housing shortages and rising prices.

This will happen in the context of a labor shortfall and rising standards of living. Remember too, that by then, the US will not have built any new houses in large numbers in 15 years.

The best-case scenario for residential real estate is that it gradually moves up for another decade, unless you live in Cupertino or Mountain View. We won?t see sustainable double-digit gains in home prices until America returns to the Golden Age in the 2020?s, when it goes hyperbolic.

But expect to put up your first-born child as collateral, and bring your entire extended family in as cosigners if you want to get a bank loan.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with. This is especially true if you lock up today?s giveaway interest rates with a 30 year fixed rate loan. At 3.3% this is less than the long-term inflation rate.

You will boast about it to your grandchildren, as my grandparents once did to me.

Crossing the Bridge to Home Sweet Home

9) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff have made the 20 mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

Well, that?s all for now. We?ve just passed the Pacific mothball fleet moored in the Sacramento River Delta and we?re crossing the Benicia Bridge. The pressure increase caused by an 8,200 foot descent from Donner Pass has crushed my water bottle. The Golden Gate Bridge and the soaring spire of the Transamerica Building are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 6, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten mile night hike up Grizzly Peak and still get home in time to watch the season opener for Downton Abbey season five. I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I?ll shoot you a Trade Alert whenever I see a window open on any of the trades above.

Good trading in 2015!

John Thomas The Mad Hedge Fund Trader

The Omens Are Good for 2015!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Zephyr.jpg342451Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-06 01:02:142015-01-06 01:02:142015 Annual Asset Class Review

After the market closes every night, I usually don a 60 pound backpack and climb the 2,000 foot mountain in my back yard.

To pass the time, I listen to audio books on financial and historical topics, about 200 a year (I?ve really got President Grover Cleveland nailed!). That?s if the howling packs of coyotes don?t bother me too much.

I also engage in mental calisthenics, engaging in complex mathematical calculations. How many grains of sand would you have to pile up to reach from the earth to the moon? How many matchsticks to circle the earth?

For last night?s exercise, I decided to quantify the impact of this year?s oil price crash on the global economy.

The world is currently consuming about 92 million barrels a day of Texas tea, or 33.6 billion barrels a year. In May, at the $107.50 high, that much oil cost $3.6 trillion. At today?s $53.60 low you could buy that quantity of oil for a bargain $1.8 trillion.

Buy a barrel of crude, and you get one for free!

This means that $1.8 trillion has suddenly been taken out of the pockets of oil producers, and put into the pockets of oil consumers. Over the medium term, this is fantastic news for oil consumers. But for the short term, things could get very scary.

$1.8 trillion is a lot of money. If you had that amount in hundred dollar bills, it would rise to 180 million inches, 15 million feet, or 2,840 miles, or 1.2% of the way to the moon (another mental exercise).

The global financial system cannot move this amount of money around on short notice without causing some pretty severe disruptions.

For a start, there is suddenly a lot less demand for dollars with which to buy oil. This has triggered short covering rallies in the long beleaguered Japanese Yen (FXY) and the Euro (FXE), which are just now backing off of long downtrends. The fundamentals for these currencies are still dire. But the short term trend now appears to be an upward one.

The US Federal Reserve certainly sees the oil crash as an enormously deflationary event. The use of energy is so widespread that it feeds into the cost of everything. That firmly takes the chance of any interest rate rise off the table for 2015. The Treasury bond market (TLT) has figured this out and launched on a monster rally.

Traders are also afraid that the disinflationary disease will spread, so they have been taking down the price of virtually all other hard commodities as well, like coal (KOL), iron ore (BHP), and copper (CU). For more depth on this, see yesterday?s piece on ?The End of the Commodity Super Cycle?.

The precipitous fall in energy investments everywhere will be felt principally in the 15 US states involved in energy production (Texas, Oklahoma, Louisiana, and North Dakota, etc.). So, the consumers in the other 35 states should be thrilled.

However, the plunge in energy stocks is getting so severe, that it is dragging down everything else with it. ALL shares are effectively oil shares right now. In fact, all asset classes are now moving tic for tic with the price of oil.

Throw on top of that the systemic risk presented by the ongoing collapse of the Russian economy. The Ruble has now fallen a staggering 70% in six months, and there is panic buying of everything going on in Moscow stores. The means that the dollar denominated debt owed by local firms has just risen by 70%. Any foreign banks holding this debt are now probably regretting ever watching the film, Dr. Zhivago.

Russian interest rates were just skyrocketed from 10.50% to 17%. The Russian stock market (RSX) is the world?s worst performing bourse this year. How do you spell ?depression? in the Cyrillic alphabet?

And guess what the new Russian currency is?

IPhone 6.0?s, of which Apple is now totally sold out in Alexander Putin?s domain!

Thankfully, this is more of a European than an American problem. But nobody likes systemic risks, especially going into illiquid yearend trading conditions. It?s a classic case of being careful what you wish for.

Of the $1.8 trillion today, about $430 billion is shifting between American pockets. That amounts to a hefty 2.5% of GDP.

Money spent on oil is burned. However, money spent by newly enriched consumers has a multiplier effect. Spend a dollar at Wal-Mart, and the company has to hire more workers, who then have more money to spend, and so on. So a shifting of funds of this magnitude will probably add 1% to U.S. economic growth next year.

Unfortunately, we will lose a piece of this from the obvious slowdown in housing. Deflation means that home prices will stagnate, or even fall. This is a major portion of the US economy which, for the most part, has been missing in action for most of this recovery.

Ultimately, cheap energy as far as the eye can see is a key element of my ?Golden Age? scenario for the 2020?s (click here for ?Get Ready for the Coming Golden Age? ).

But you may have to get there by riding a roller coaster first.

Oil at $53?

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/roller_coaster_monks-e1479779374563.jpg306300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-17 09:42:222014-12-17 09:42:22Why All Shares Are Now Oil Shares

When the Trade Alerts quit working. I stop sending them out. That?s my trading strategy right now. It?s as simple as that.

So when I received a dozen emails this morning asking if it is time to double up on Linn Energy (LINE), I shot back ?Not yet!? There is no point until oil puts in a convincing bottom, and that may be 2015 business.

Traders have been watching in complete awe the rapid decent the price of Linn Energy, which is emerging as the most despised asset of 2014, after commodity producer Russia (RSX).

But it is becoming increasingly apparent that the collapse of prices for the many commodities is part of a much larger, longer-term macro trend.

(LINN) is doing the best impersonation of a company going chapter 11 I have ever seen, without actually going through with it. Only last Thursday, it paid out a dividend, which at today?s low, works out to a mind numbing 30% yield.

I tried calling the company, but they aren?t picking up, as they are inundated with inquires from investors. Search the Internet, and you find absolutely nothing. What you do find are the following reasons not to buy Linn Energy today:

1) Falling oil revenue is causing Venezuela to go bankrupt. 2) Large layoffs have started in the US oil industry. 3) The Houston real estate industry has gone zero bid. 4) Midwestern banks are either calling in oil patch loans, or not renewing them. 5) Hedge Funds have gone catatonic, their hands tied until new investor funds come in during the New Year. 6) Every oil storage facility in the world is now filled to the brim, including many of the largest tankers.

Let me tell you how insanely cheap (LINN) has gotten. In 2009, when the financial system was imploding and the global economy was thought to be entering a prolonged Great Depression, oil dropped to $30, and (LINN) to $7.50. Today, the US economy is booming, interest rates are scraping the bottom, employment is at an eight year high, and (LINE) hit $9.70, down $70 in six months.

Go figure.

My colleague, Mad Day Trader, Jim Parker, says this could all end on Thursday, when the front month oil futures contract expires. It could.

It isn?t just the oil that is hurting. So are the rest of the precious and semi precious metals (SLV), (PPLT), (PALL), base metals (CU), (BHP), oil (USO), and food (CORN), (WEAT), (SOYB), (DBA).

Many senior hedge fund managers are now implementing strategies assuming that the commodity super cycle, which ran like a horse with the bit between its teeth for ten years, is over, done, and kaput.

Former George Soros partner, hedge fund legend Paul Tudor Jones, has been leading the intellectual charge since last year for this concept. Many major funds have joined him.

Launching at the end of 2001, when gold, silver, copper, iron ore, and other base metals, hit bottom after a 21 year bear market, it is looking like the sector reached a multi decade peak in 2011.

Commodities have long been a leading source of profits for investors of every persuasion. During the 1970?s, when president Richard Nixon took the US off of the gold standard and inflation soared into double digits, commodities were everybody?s best friend. Then, Federal Reserve governor, Paul Volker, killed them off en masse by raising the federal funds rate up to a nosebleed 18.5%.

Commodities died a long slow and painful death. I joined Morgan Stanley about that time with the mandate to build an international equities business from scratch. In those days, the most commonly traded foreign securities were gold stocks. For years, I watched long-suffering clients buy every dip until they no longer ceased to exist.

The managing director responsible for covering the copper industry was steadily moved to ever smaller offices, first near the elevators, then the men?s room, and finally out of the building completely. He retired early when the industry consolidated into just two companies, and there was no one left to cover. It was heartbreaking to watch. Warning: we could be in for a repeat.

After two decades of downsizing, rationalization, and bankruptcies, the supply of most commodities shrank to a shadow of its former self by 2000. Then, China suddenly showed up as a voracious consumer of everything. It was off to the races, and hedge fund managers were sent scurrying to look up long forgotten ticker symbols and futures contracts.

By then commodities promoters, especially the gold bugs, had become a pretty scruffy lot. They would show up at conferences with dirt under their fingernails, wearing threadbare shirts and suits that looked like they came from the Salvation Army. As prices steadily rose, the Brioni suits started making appearances, followed by Turnbull & Asser shirts and Gucci loafers.

There was a crucial aspect of the bull case for commodities that made it particularly compelling. While you can simply create more stocks and bonds by running a printing press, or these days, creating digital entries on excel spreadsheets, that is definitely not the case with commodities. To discover deposits, raise the capital, get permits and licenses, pay the bribes, build the infrastructure, and dig the mines and pits for most commodities, takes 5-15 years.

So while demand may soar, supply comes on at a snail pace. Because these markets were so illiquid, a 1% rise in demand would easily crease price hikes of 50%, 100%, and more. That is exactly what happened. Gold soared from $250 to $1,922. This is what a hedge fund manager will tell us is the perfect asymmetric trade. Silver rocketed from $2 to $50. Copper leapt from 80 cents a pound to $4.50. Everyone instantly became commodities experts. An underweight position in the sector left most managers in the dust.

Some 14 years later and now what are we seeing? Many of the gigantic projects that started showing up on drawing boards in 2001 are coming on stream. In the meantime, slowing economic growth in China means their appetite has become less than endless.

Supply and demand fell out of balance. The infinitesimal change in demand that delivered red-hot price gains in the 2000?s is now producing equally impressive price declines. And therein lies the problem. Click here for my piece on the mothballing of brand new Australian iron ore projects, ?BHP Cuts Bode Ill for the Global Economy?.

But this time it may be different. In my discussions with the senior Chinese leadership over the years, there has been one recurring theme. They would love to have America?s service economy.

I always tell them that they have a real beef with their ancient ancestors. When they migrated out of Africa 50,000 years ago, they stopped moving the people exactly where the natural resources aren?t. If they had only continued a little farther across the Bering Straights to North America, they would be drowning in resources, as we are in the US.

By upgrading their economy from a manufacturing, to a services based economy, the Chinese will substantially change the makeup of their GDP growth. Added value will come in the form of intellectual capital, which creates patents, trademarks, copyrights, and brands. The raw material is brainpower, which China already has plenty of.

There will no longer be any need to import massive amounts of commodities from abroad. If I am right, this would explain why prices for many commodities have fallen further that a Middle Kingdom economy growing at a 7.5% annual rate would suggest. This is the heart of the argument that the commodities super cycle is over.

If so, the implications for global assets prices are huge. It is great news for equities, especially for big commod

ity importing countries like the US, Japan, and Europe. This may be why we are seeing such straight line, one way moves up in global equity markets this year.

It is very bad news for commodity exporting countries, like Australia, South America, and the Middle East. This is why a large short position in the Australian dollar is a core position in Tudor-Jones? portfolio. Take a look at the chart for Aussie against the US dollar (FXA) since 2013, and it looks like it has come down with a severe case of Montezuma?s revenge.

The Aussie could hit 80 cents, and eventually 75 cents to the greenback before the crying ends. Australians better pay for their foreign vacations fast before prices go through the roof. It also explains why the route has carried on across such a broad, seemingly unconnected range of commodities.

In the end, my friend at Morgan Stanley had the last laugh.

When the commodity super cycle began, there was almost no one around still working who knew the industry as he did. He was hired by a big hedge fund and earned a $25 million performance bonus in the first year out. And he ended up with the biggest damn office in the whole company, a corner one with a spectacular view of midtown Manhattan.

He is now retired for good, working on his short game at Pebble Beach.

Good for you, John.

Not as Shiny as it Once Was

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Gold-Coins.jpg391380Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-16 01:03:502014-12-16 01:03:50End of the Commodity Super Cycle

You can pay up to $17 a unit for (LINN) and have a good chance of making a quick, snapback profit.

All of a sudden, everyone I know in Texas, and there are quite a few of them, called to tell me to buy Linn Energy, all within the space of one hour. I summarize their diverse comments below.

We have reached a margin call induced capitulation sell off in Linn Energy this morning, when oil was trading as low as $64 a barrel at the European opening.

There were obviously also a couple of leveraged energy and commodity funds that blew up and are undergoing forced liquidation at the market.

Add to that all the individuals who bought (LINN) on margin when the yield was only 8% so they would take 16% home to the bank.

This has taken the price of the units down to an artificial, and hopefully temporary, low of $15.90. At that price, the yield was a mind blowing 17% (after all, this is California).

It was a classic ?Throwing out the baby with the bathwater? moment. (LINN) gets 54% of its $1.6 billion in revenues from natural gas, which has held up remarkably well in the energy melt down, thanks to the early arrival of the polar vortex this winter.

Only 22% of its income derives from oil related projects, and half of this is hedged in the futures market from any downside exposure in the price of oil, according to the company?s recent pronouncements. Linn has actually plunged more than oil from its recent peak.

Does a loss on 10% of its revenues justify a gut wrenching 50% drop in the units? I think not.

But then, I am being rational and analytical, and I can assure you that the energy markets are now anything but rational and analytical.

Its not like oil is going to stay this low forever. Try to buy oil for delivery in the futures market two years out, and it has already recovered to $75/barrel, and there is very little available at that price.

What happens when the price of something goes down? Demand increases, and that will be good for Linn Energy, which is inherently more of a volume play on gas and oil, not a price play.

Keep also in mind that the absurd salaries the company was paying for workers in the Midwest has also vaporized. Roustabouts can now be had for as little as $75,000 a year compared to $200,000 only six months ago. This will cut (LINN)?s costs quickly and flow straight to the bottom line.

Falling costs and rising volumes sound like a winning formula to me.

And if you have the courage to buy the units here on margin, the yield rockets to a breathtaking 34%. It therefore can?t stay this low for long.

Linn Energy, LLC is an independent oil and natural gas company based in Houston, Texas. It holds oil and gas producing assets in many parts of the United States: Mid-Continent, including properties in Texas, Louisiana, and Oklahoma; the Hugoton Basin in Kansas; the Green River Basin in Wyoming; East Texas; California, including the Brea-Olinda Oil Field in Los Angeles and Orange Counties; the Williston/Powder River Basin, which includes a position in the Bakken Formation; Michigan/Illinois; and the Permian Basin in Texas.

At the end of 2012, the firm reported proved reserves of 4,796 bcfe (billion cubic feet equivalent) of oil and gas combined. Of this total, 24% was crude oil, 54% natural gas, and 22% natural gas liquids.

Structured as a master limited partnership for tax purposes, the firm is required to pay out most of its cash reserve to unitholders (stockholders) each quarter as distributions, thereby ducking the double taxation of corporate taxation.

However Linn retains some attributes of a limited liability corporation, including giving voting rights to its unitholders. Linn Energy also operates a subsidiary, LinnCo, a C Corporation, which is subject to different tax rules from its parent company.

All we have to do is survive the near term volatility and Linn Energy will be a winner.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/LINN-Energy.jpg313361Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-02 09:23:062014-12-02 09:23:06Loading Up On Linn Energy

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.