Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)

Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

Mad Hedge Technology Letter

January 7, 2019

Fiat Lux

Featured Trade:

(NOT TOO GOOD TO BE TRUE),

(SCHW), (FB), (SQ), (WMT), (AMZN), (FFIDX), (BOX)

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

Mad Hedge Technology Letter

November 28, 2018

Fiat Lux

Featured Trade:

(TRUMP'S TARIFF THREAT FOR APPLE))

(AAPL), (BABA), (EBAY), (WMT), (FB), (MSFT), (AMZN)

The administration’s threat of levying 10% on iPhones is a great sign for the technology sector as a whole.

The short-term media sensationalism has flipped this story the other way around crying about this as if it is a major penalty to Apple (AAPL).

Don’t get me wrong, these potential stiff tariffs have the possibility of triggering a $1 billion loss on Apple’s revenue, but this is all about protecting American technology long term.

This is not like taking a sledgehammer and ruining their business model, and it will not strip away this brilliant wealth creation vehicle.

Apple remains a cheap stock to buy for patient long-term holders and is one of the best run companies in the world with an operating maestro executing the roll-out of premium products named Tim Cook, the CEO of Apple.

The administration might not like some of technology firms’ tactics, but in reality, they are a pivotal reason why the economy has been humming along in the longest bull-market ever.

Effectively, the administration has put Apple and its peers up on a pedestal and is defending them from Chinese competition.

What industry wouldn’t want this?

Most of 2018, the current administration presided over a stock market that was going up in a straight line and the bulk of those gains were harvested by the major tech companies, mainly the FANGs.

The administration was quick to take credit for a strengthening stock market and would like to see rates suppressed to engineer more upside.

The FANGs are going through a reversion to the mean after 100% gains and giving back 20% or 30% of profits offer opportune entry point for long-term investors.

The only FANG that needs a structural change is Facebook (FB) and has the funds to do it. The other three plus Microsoft (MSFT) will lead the tech charge when the short-term weakness subsides.

If you think Chinese consumers would bail on Apple products because of the trade war, then you are wrong.

Apple has been grandfathered into Chinese society and it is one of the few iconic American products that can boast this achievement.

Apple is a luxury brand produced by an epochal superpower.

The presence of Apple products reverberates around China’s economic landscape, and even if Chinese people do not like America, they respect its economic prowess and wish to learn from its capitalistic ways.

This is the main reason they send their kids to American universities.

Historically, China was once entirely dependent on Russia to fill in its economic and social vision with the communist party sending its best and brightest to Moscow to study the Soviet Union’s secret sauce.

If you go to Beijing now, most of the second ring road of flats conspicuously remind me of Khrushchyovkas, the unofficial name of a type of low-cost, concrete-paneled or brick three- to five-storied apartment building which was developed in the Soviet Union during the early 1960s.

During this time, its namesake Nikita Khrushchev directed the Soviet government.

Pre-Deng Xiaoping Soviet influences can still be found everywhere in central Beijing.

Once the Chinese communist government realized that the Soviet model impoverished large swaths of society, they went on the open market to find a more optimal method to run their economy that could take advantage of their monstrous man power.

The model they decided on was a fusion of communism and capitalism, and for 30 years, this system fueled Chinese peasants out of poverty and to the promenades of Saint-Tropez.

Because of Chinese laser-like obsession on social status, material possessions are the most important way for them to differentiate against each other.

For Chinese women, the x-factor is skin tone, but for Chinese men, it is the brand, quality, and volume of possessions.

Even if rich Chinese hate Apple and their iPhones, they are permanently married to this product because owning a Chinese smartphone would be a monumental faux pas on the same level as American First Lady Melania Trump shopping for her new clothes at Walmart (WMT).

This is the same reason why every political who’s who in China drives an Audi A6, and every successful Chinese business executive drives a BMW.

Luxury brands are closely associated to the person’s social status in China and these unwritten rules have even more weight than the official rules in China partly because most Chinese over 40 are uneducated, plus China’s lack of public trust.

Apple’s tentacles reaching deep into Chinese society have in fact led to a situation where Apple-related jobs for Chinese citizens add up to over 5 million jobs which is over double the number of jobs Apple supports in America.

The result of Apple morphing into a pseudo-Chinese company is that pain for Apple means a loss of Chinese jobs on a large scale at a time when the Chinese economy is becoming more precarious by the day.

The Chinese economy is softening under a massive burden of crippling public and private debt that is putting the cap on growth.

As a result of the trade skirmish, China has temporarily halted its deleveraging effort that was intended to remedy the health of the economy and has reverted back to the China of old, low-quality infrastructure projects and heavily polluted coal production.

China’s rapid ascent to prosperity could also mean the Chinese consumer and economy could go through a reversion to the mean scenario with private and public companies loaded to their eyeballs with debt going bust and a looming economic stimulus in the cards if this plays out.

All this means is that Apple is too big to fail in China and CEO of Apple Tim Cook absolutely knows this.

Theoretically, Chinese consumers absolutely have access to local smartphone substitutes for $200 that would do the same job as a $1,000 iPhone.

I have tested out Huawei and Xiaomi premium smartphones costing $400, and they have more than enough firepower to be a reliable everyday smartphone and some.

The fact is that Chinese consumers intentionally choose not to substitute Apple products.

And I would go deeper than that by saying Steve Jobs is revered in China like a demigod and his passing turned him into a sort of tech martyr with a level of status that not even Alibaba (BABA) originator Jack Ma can touch.

Jack Ma performed miracles by copying eBay’s (EBAY) blueprint of e-commerce from a shabby Hangzhou flat ditching his former job as an English teacher then copying Amazon (AMZN) to juice up growth.

But Jack Ma never created the iPhone, iPod, tablet, or Apple app store from thin air. That he never did.

Making matters even more ironic is that most Chinese communist members actually use an Apple iPhone for the same reasons I mentioned earlier.

Not only that, the children of Chinese communist politicians take lavish vacations to Silicon Valley to take selfie’s in front of Apple’s spaceship headquarters in Cupertino and upload them onto social media.

They then proceed to visit the nearest Apple store right next door at the Apple Park visitor center which is essentially an Apple store on steroids to make bulk purchases of Apple tablets, watches, computers, iPhones for their extended circle of friends and distant relatives because they are “cheaper in America than in China” mainly due to the heavy import duties levied on Apple products in China.

As for tech equities, what this does is blunt short-term positive sentiment for tech stocks and particularly chip stocks that I have told readers to stay away from like the plague.

Apple’s supply chain frenemies don’t have the luxury of selling 80 million luxury phones at $1,000 per quarter and are often the recipient of indiscriminate sell-offs shellacking shares.

Even with the overhanging issue of rising tariffs, tech stocks should produce great earnings next year.

Look at Apple and the consensus EPS outlook for next quarter comes in at $4.73 and that is after EPS increasing 41% sequentially from the quarter before.

Apple will soon become a $300 billion of sales per year company with profitability expanding at a rapid clip.

They are a company that prints money then buys back their own stock profusely. Not many companies can do that.

These negative reports that have been coming fast and furious don’t help the momentum, but the share’s weakness solely means that better entry points are available for investors before Apple launches over $200 again.

There is a high chance that the administration is using Apple as a bargaining chip and nothing will come of it.

Think about it, after all this commotion about the trade war with China, revenue was up almost 20% last quarter in greater China, so what gives?

It means that things aren’t as dire as it seems. A lot of hot steam over nothing is a gift to long-term investors, but short-term traders will feel the pain of the temporarily elevated headline risk.

At our weekly Monday staff meeting, coworkers were griping and grimacing about their failed internet connections and annoying glitches to their favorite e-commerce sites during the mad rush to find the best deal during Black Friday and Cyber Monday.

Internet traffic was that torrential when sites were driven offline for minutes and some, hours by a bombardment of gleeful shoppers hoping to splash their credit card numbers all over the web on sweet discounts.

The crashing of system servers epitomizes the robust transition to online commerce that has most of us pinned to our devices surfing our go-to platforms all day long.

According to data from Adobe (ADBE) analytics, Black Friday sales jumped 23.6% YOY to $6.22 billion, and it was the first time in history that mobile sales broke the $2 billion threshold.

It is a clear victory for e-commerce and, in particular, mobile shopping that has become more integrated into modern tech DNA.

Mobile sales comprised 33.5% of total sales and were up from 29.1% last year, signaling that more is yet to come from this transcending movement that is shoving everything from content, digital ads, entertainment, banking and pretty much everything you can think of to your handheld smartphone.

CEO of Kohl’s (KSS) Michelle Gass confirmed the e-commerce strength by saying, “80 percent of traffic online came from mobile devices.”

The beauty of this movement is that it’s not an “Amazon (AMZN) takes all” scenario with other players allowed to feast on a growing size of the e-commerce pie.

“Click and collect” has been a strategy that has paid off handsomely with sales up 73% YOY during the shopping holidays.

This all supports my prior claim that e-commerce is one of the most innovative and dynamic parts of technology especially the grocery space, and the buckets full of capital attempting to reconfigure the e-commerce spectrum is creating an enhanced customer experience for the final buyer resulting in better products, superior delivery methods, and cheaper prices.

Some other retailers spicing up their e-commerce strategy are dinosaur big-box retailer’s intent to defend their business from the Amazon death star.

If you can’t innovate in-house, then “borrow” the innovation from somewhere else.

That is exactly what Target (TGT) has chosen to do announcing last week that it would grant free 2-day shipping with no minimum sale threshold.

The tactic is bent on undercutting Walmart (WMT) who currently operate a 2-day free shipping policy with a minimum order of $35.

Most shoppers will buy in bulk easily eclipsing the $35 per order mark minimizing the rot of small orders.

And if they aren’t eclipsing the $35 per order mark, it demonstrates the firm’s offerings lack the diversity and quality to compete with Amazon.

Capturing the incremental sale squarely rests on the e-tailers ability to coax out the buyers’ impulses to move on the can’t-miss items.

The lesser known retailers fail miserably at matching the lineup of products that Amazon can roll out.

The bountiful product selection at Amazon leads customers to pay for 3, 4, 5, 6 or more items on Amazon.com.

That said, I am bullish on Walmart’s e-commerce strategy. The “click and collect” strategy has shown to be an outsized winner increasing industry sales of this type 120% YOY.

Walmart is at the center of this strategy and they are refurbishing their supercenters to accommodate this growth in collecting from the curb.

Effectively, this gives customers the option to skip the queue instead of bracing the hoards and navigating the crowds of shoppers in the supercenter.

Other changes are minor but will help, such as offering online product location maps to customers beforehand and allowing customers to pay for large items like big-screen televisions on the spot.

The biggest windfall is derived from the cataclysmic demise of Toy “R” Us, giving Walmart a new foothold into the toy business.

Walmart is beefing up toy items by 40% in the stores and layering that addition with another 30% increase in their e-commerce division.

Adobe’s upper management recently said in an interview that interactive toys have been a wildly popular theme this year amid a backdrop of the best holiday shopping season ever recorded.

Another attractive gift selling like hotcakes are video games, titles boding well for sales at Activision (ATVI), EA Sport (EA), and Take-Two Interactive (TTWO).

Reliant IT infrastructure will be a key component to executing these holiday sales bonanzas.

Clothing retailer J. Crew and home improvement chain Lowe's (LOW) were grappling with sudden disruptions to their IT systems before they managed to get back online.

More than 75 million shoppers parade the internet to shop during Black Friday and Cyber Monday, and the opportunity cost swallowed to a tech glitch is a CEO’s worst nightmare.

Ultimately, what does this all mean?

Focusing on the positive side of the surging holiday sales is the right thing to do because the avalanche of momentum will have a knock-on effect on the rest of the economy.

Certain companies are positioned to harvest the benefits more than others.

Amazon guided its 4th quarter estimates conservatively and is in-line to beat top and bottom line forecasts.

Other pockets of strength are Walmart’s tech pivot, albeit from a low base. Walmart still has more room to maneuver and they are in the 2nd inning of their tech transformation snatching the low-hanging fruit for now.

Another interesting e-commerce company swinging its elbows around is Etsy (ETSY).

They sell vintage and handmade craft adding the personalized touch that Amazon can’t destroy.

Margins will be higher than the typical low-cost, value e-commerce platform, but scaling this type of business will be more difficult.

Sales grew 41% sequentially and just in time for a winter holiday blowout.

Etsy became profitable in 2017 after three straight loss-making years, and 2018 is poised to become its best year ever.

The profitability bug is hitting Etsy at the perfect time with its EPS growth rate up 36% sequentially.

They report at the end of February and I expect them to smash all estimates.

There are some deep ramifications for the long term of e-commerce that is beginning to suss itself out.

For one, shipping times will continue to be slashed with a machete. If you are enjoying the 2-day free shipping from Amazon and Target now, then wait until 2-day becomes 1-day free shipping.

Then after 1-day free shipping, customers will get 10-hour shipping, and this won’t stop until goods are shipped to the customer’s door in less than 1-hour or less.

This is what the massive $50 billion in logistical investments over the next five years by the likes of Uber and Amazon are telling us.

It will take years for the efficiencies to come to fruition, but it is certainly in the works.

In the next five years, America’s logistics infrastructure will have to accommodate the doubling of e-commerce packages from 2 billion to 4 billion per year.

Another trend is that omnichannel offerings are sticking and won’t go away anytime soon.

It was once premised that online sales would destroy brick and mortar, yet moving forward, a mix of different sales channels will be the most efficient way of moving goods in the future.

Pop-up stores have been an intriguing phenomenon of late, and surprisingly, 60% of consumers still require interaction with the product to be convinced it's worthy of buying.

Certain products such as fashionable dresses and designer shoes must be given a whirl before a decision can be made. This won’t change anytime soon.

The timing of the sales and marketing push has been moved forward as competitors are eager to get a jump on one another.

Management is agnostic to the timing of the sale.

Thus, discounted sales will show up a week before Thanksgiving as pre-Thanksgiving sales in the future elongating the holiday shopping season cycle by starting it early and delaying the finish of it.

Lastly, the record numbers prove that the e-commerce renaissance and the pivot to mobile is not just a flash in the plan.

What does this mean for tech equities?

The temporal tech sell-off of late is largely a result of outside macro forces and is not indicative of the overall health of the tech sector that has experienced record earnings.

If the markets can keep its head above the February lows, it sets up an intriguing December fueled by Americans flashing their digital wallets on online platforms.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

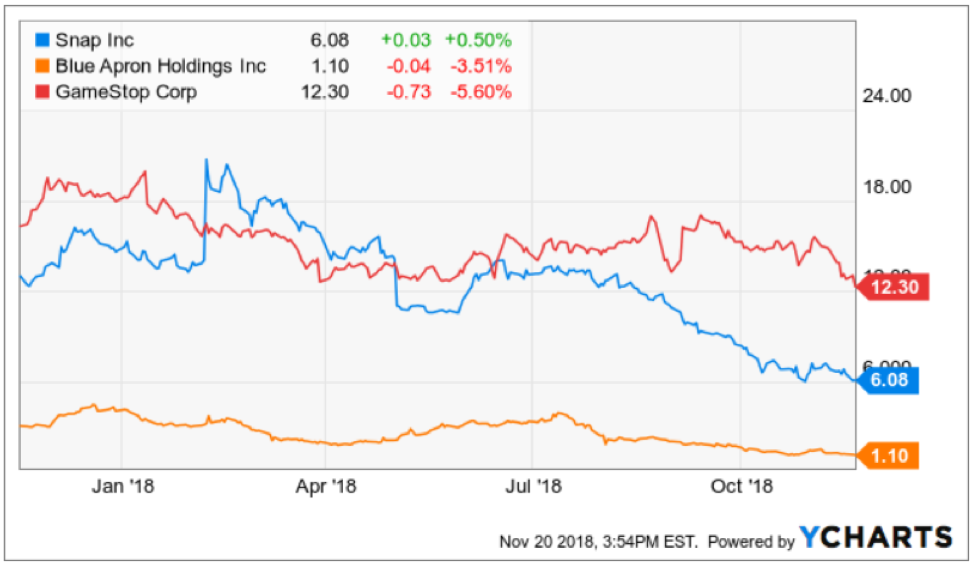

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Global Market Comments

November 19, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

(SPY), (WMT), (NVDA), (EEM), (FCX), (AMZN), (AAPL), (FCX), (USO), (TLT), (TSLA), (CRM), (SQ)