Below please find subscribers’ Q&A for the December 13 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: I think it's a good time to buy gold, do you agree? If so, what are your top picks for a long-term hold?

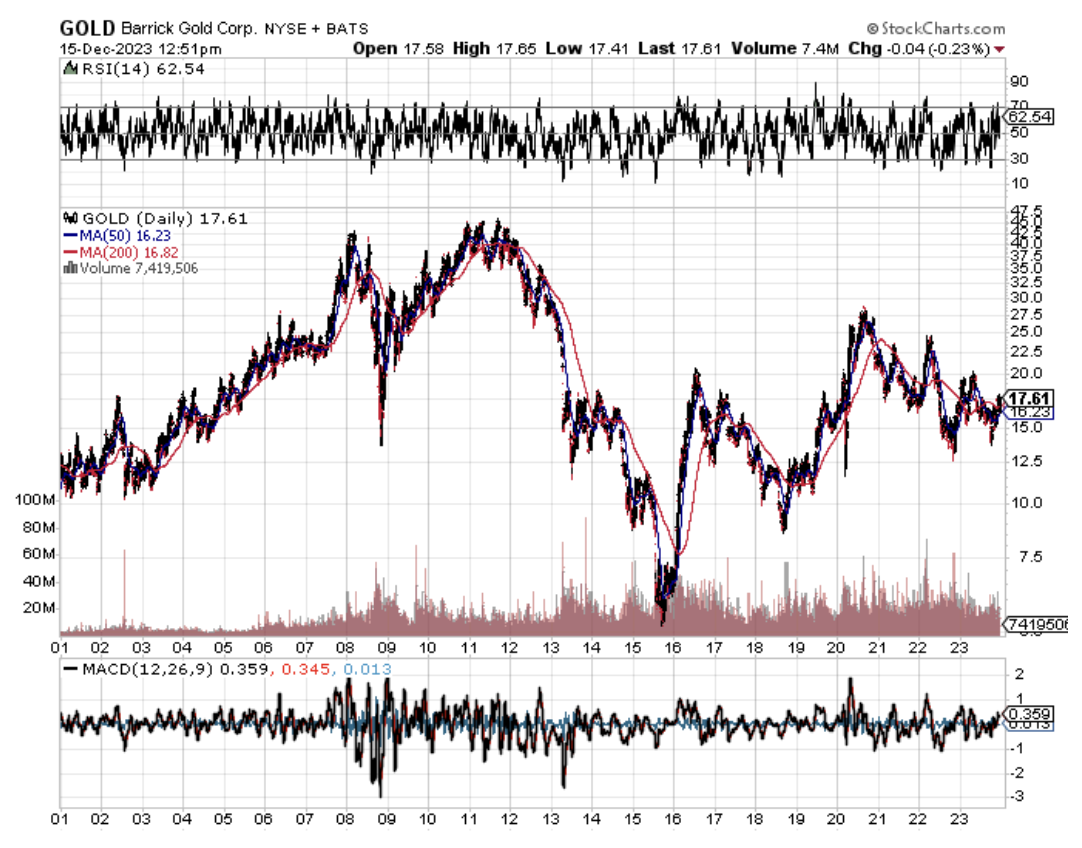

A: I was looking at some very long-term gold charts, and gold tends to have really hot and really cold decades, and we're just finishing a cold decade. In fact, the price of gold today is roughly where it was 12 years ago—it hasn't moved in 12 years. But if you look at the decade before that, it went up ten times from $200 to $2,000, so we're about to enter another hot decade. It may not go up 10X, but 5X is realistic. That would take us up from $2,000 to $10,000, and I think we could see $3,000 as early as 2025.

The best plays are always the gold miners. And my two favorite picks there are Barrick Gold (GOLD) and Newmont Mining (NEM). If you want to be even more aggressive than that, the underlying miners tend to go up at four times the rate of the gold metal. I can also go with junior minors who probably are losing money now, but if gold goes up to $5,000, they'll make money. Those are hugely leveraged, high-risk plays.

Q: Is it time to sell Tesla (TSLA) stock on all long-term accounts?

A: It is not. If you truly are long-term, I think Tesla goes to $10,000 eventually, but we are in the middle of a price war. Price wars are not when you want to be involved in the stock, so I wouldn't be adding to Tesla positions here—I want to see what the final bottom looks like, when the price wars end the prices start to go up, and we'll get that with an economic recovery next year.

Q: Who are Tesla's prime competitors?

A: I would say it's BYD CO., INC. (BYDDF) in China. BYD, which I visited in China 12 years ago, is actually out selling Tesla in China, and they have the ability to produce a super cheap car. They have a $25,000 car in Europe right now, and the fear is that they will make a $15,000 car, and then flood the United States with it. I doubt that will happen; they've never been able to reach American quality and safety standards, and that's why you don't see Chinese cars here. You do see them in other countries like Australia, Hong Kong, and parts of Africa; and they're currently making a big push in Europe, which certainly has all the German car producers worried. Competition is out there and does pose a risk to Tesla, but I think long-term Tesla still wins anyway. By the way, I hasten to mention there are no American competitors to Tesla. Tesla is so far ahead that the big three will never ever catch up and eventually just be reduced to selling Teslas on license.

Q: Where do you think the bottom in oil is?

A: The consensus in the market right now is $62 a barrel. That's about another $6 or $8 lower than here, and then I think we really do bottom out. Then you want to start piling into oil producers like ExxonMobil (XOM), which we had a position in last week, and Occidental Petroleum (OXY), which is the number one pick by Berkshire Hathaway. So those are two good names to go with. What drives these and all other commodities in the future? The answer is a recovering economy. Let's assume we drop from 5.2% last quarter to maybe 2% this quarter—we will accelerate to 5% next quarter, and that's what takes all of your commodity plays upward.

Q: Would you buy retailers here like Walmart (WMT) or Target (TGT)?

A: No. The time to buy retailers is in the run-up to Christmas. I don't know about you, but I'm finished with all my Christmas shopping! You want to buy in the run-up to Christmas shopping, not when it's peaking. Target on the other hand has done really well, and on a massive cost-cutting effort.

Q: When do you think is the first interest rate cut?

A: Since the market has a consensus of May, with some people saying March, I'll go for June. I think this Fed wants to torture us a little bit more and delay any interest rate cuts, but markets will discount that anyway. So it all sets up a great backdrop to buy stocks now, because markets discount things six months in advance, and six months from now is May. That's why we've had the ballistic moves that we've seen in stocks.

Q: Whatever happened to the natural gas trade United States Natural Gas Fund (UNG)?

A: The problem with all these commodity trades is that they are all in one way or another dependent on the weather, and we are having a warm winter, so you can't fool Mother Nature. Not only is it warm here, but it's warm in China, and in Europe. I think they have this thing called…global warming? It makes you ask yourself if you even want to be near an energy trade during a time of global warming, which is accelerating. So anyway, we had a nice profit on this in October—it completely went away. The (UNG) ETF went from $8 all the way down to $4.50, so we'll just have to wait for the cold weather and for (UNG) to ramp up. If it doesn’t happen soon, we may not have a rally this year in natural gas. Pray for snow!

Q: Is junk the best to buy in bonds?

A: It's the best risk-reward ratio; it has a yield roughly 50% higher than TLT with only slightly more risk. The default ratio on junk bonds is actually quite low. And in fact, before you buy (JNK) (SPDR Bloomberg High Yield Bond ETF) or (HYG) (iShares iBoxx $ High Yield Corporate Bond ETF), go to the website and look at their largest holdings and you’ll see what I mean, it's all airlines and cruise lines which had to load up on debt during the pandemic but are doing great right now.

Q: How can the market still rally if it's time to sell and take profit?

A: We get a round of profit-taking at some point, and there's your entry point. Right now, no professional trader is buying anything right now, they're just holding back and seeing when they take profits. And the way traders think is they don't want to trade anymore until they get paid! The year end is ending shortly and the risk-reward favors taking profits and then sitting on the profits. Guess what I'm doing? I'm taking profits and sitting on the profits because traders have bonuses that tend to get paid in January.

Q: On the (TLT) put trade, should one get out once it hits $95?

A: Yes, I always stop out when we hit the nearest strike on a call spread or a put spread. That's a good discipline to have. 90% of the time, if you hold on to expiration, you make the maximum profit in these, but that 10% of the time it's a total write-off, so you get to choose. I try to keep the volatility of the Mad Hedge service low so I always stop out quickly—easier to dig yourself out of a small hole than a big one.

Q: How do you think the next two government shutdowns in January and February will affect the market? Is this a buying opportunity?

A: Absolutely, yes, it is a buying opportunity. Shutdowns tend to be short, but you may get a lot of political turmoil, especially in the House. After the Long Island by-election to replace the disgraced George Santos the Republican majority is likely to shrink to only two seats. The House could fire another speaker, for example. We're kind of in unprecedented territory here in terms of the US government, but at any stock market decline, you would be a big buyer. That's how to play it. If people want to puke out on what's happening in Washington—thank you very much, I'll take your stock.

Q: Are we still bullish on the Barack Gold (GOLD) LEAPS?

A: Absolutely, especially if you have the 2025 expiration. There is an easy double or triple here.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At BYD in China 2011