Global Market Comments

April 17, 2019

Fiat Lux

Featured Trade:

(DECODING THE GREENBACK),

(WHAT ABOUT ASSET ALLOCATION?)

(TESTIMONIAL),

Global Market Comments

April 17, 2019

Fiat Lux

Featured Trade:

(DECODING THE GREENBACK),

(WHAT ABOUT ASSET ALLOCATION?)

(TESTIMONIAL),

Mad Hedge Technology Letter

April 17, 2019

Fiat Lux

Featured Trade:

(ALPHABET DOMINATES WITH GOOGLE MAPS)

(GOOGL), (AMZN), (YELP), (UBER)

Asset allocation is the one question that I get every day, which I absolutely cannot answer.

The reason is simple: no two investors are alike. The answer varies whether you are young or old, have $1,000 in the bank or $1 billion, are a sophisticated investor or an average Joe, in the top or the bottom tax bracket, and so on.

This is something you should ask your financial advisor, if you haven’t fired him already, which you probably should.

Having said all that, there is one old hard and fast rule which you should probably dump. It used to be prudent to own your age in bonds. So if you were 70, you should have had 70% of your assets in fixed income instruments and 30% in equities.

Given the extreme over valuation of all bonds today, and that we probably just entered a 30-year bear market, I would completely ignore this rule and own no bonds.

Instead you should substitute high dividend paying stocks for bonds. You can get 4% a year or more in yields these days, and get a great inflation hedge, to boot. You will also own what everyone else in the world is trying to buy right now, high yield US stocks.

Remember Google Maps?

Google will start monetizing it, let me tell you about it.

The web mapping service developed by Google gifting access to satellite imagery, aerial photography, street maps, 360° panoramic views of streets has been around since the beginning of this generation of big tech and is what I would consider legacy technology.

Legacy technology is often associated with failure as the out of date nature isn’t applicable to the tech scene and the commercialization of it today.

In a candid letter, Jeff Bezos wrote to shareholders that Amazon will “occasionally have multibillion-dollar failures.”

Silicon Valley tech will have its share of implosions stemming from ill-fated industry decisions correlating to heavy losses.

Google Maps won’t be one of these slip-ups.

However, a whole catalog of instances can be chronicled from Microsoft’s purchase of Nokia’s handset division to Google’s social media foray in Google Plus.

It hasn’t gone all pear-shaped for Alphabet in 2019. I strongly believe they are one of the companies of the year harnessing YouTube in ways consumers never imagined.

Adding color to the story, any remnant of apprehension to any bearish feelings about Alphabet should vanish once investors understand how lucrative Google Maps will become.

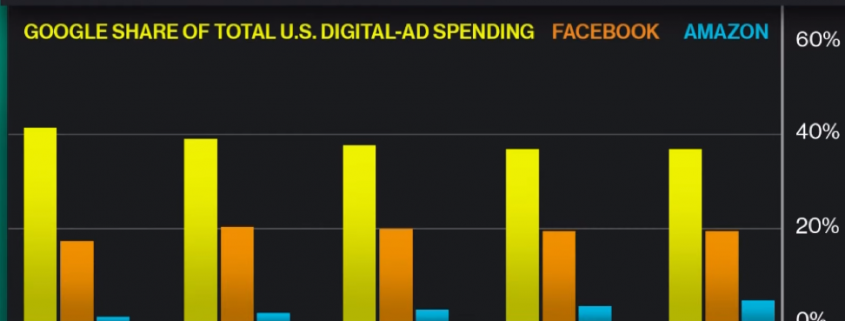

Google has spent decades and billions of capital honing the application and in terms of market share they have cultivated a monopoly.

Uber’s S-1 filing shined some light on Google Maps characterizing it as a must-have input into their business saying, “We do not believe that an alternative mapping solution exists that can provide the global functionality that we require to offer our platform in all of the markets in which we operate.”

Uber sunk $58 million integrating Google Maps into its services from 2016-2018 along with continuous payments to its Google Cloud arm to host Uber’s data.

The strong relationship with Uber shows how Alphabet is adept at milking 3rd party apps for what they are worth.

Alphabet’s stake in Uber is projected to be $5 billion from the $250 million investment in Uber in 2013.

The party doesn’t stop there with Uber paying Alphabet $631 million from 2016-2018 in digital marketing services and another $70 million for technology infrastructure.

To say that Google firmly has its tribal marks tattooed into Uber’s skin is an understatement.

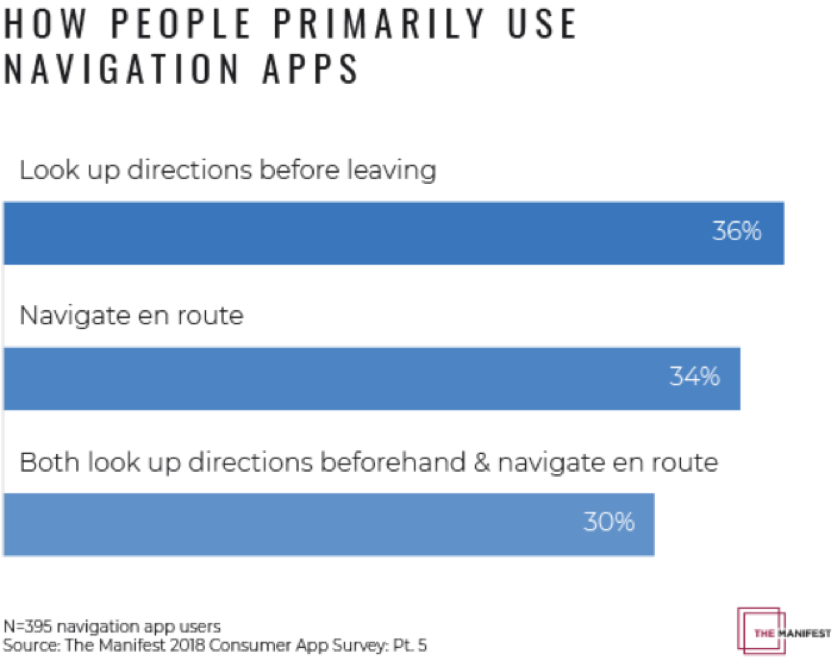

Almost 80% of smartphone users regularly use navigation apps.

Google Maps is the most popular navigation app by a country mile with 67% of market share.

One billion people consistently use Google Maps.

It is the go-to navigation app for nearly 6x more people compared to the runner up app Waze with 12% market share.

The superior performance of the app has allowed it to branch off into a Yelp-like hybrid app accumulating reviews of businesses and institutions that are conveniently dotted around its map.

Multi-functional terrain was integrated to make the maps more 3D and route navigation from point A to B routes has steadily improved since its inception.

The increasing detail showing even roofs of sheds and the Google street view offering a point of view vantage point boosting the reliability of the app.

The result of making the app better is that navigators can easily discern locations and follow routes clearly.

Most would concede that they use the app to look up specific street routes.

By implementing digital ads into the experience, product and service offers will possibly populate in real time as the user glances at the app’s directions.

A vast amount of services such from food to personal grooming to even cannabis club ads could be applicable and ad companies will pay top dollar to post on Google Maps.

Google could also offer personalized recommendations to users and collect an affiliate fee if the user clicks on an attached link transferring the customer to a 3rd party landing page.

They already benefit from this strategy on Google Flights.

Google might even be tempted to implement a Groupon model with group discounts on services positioned on Google Maps.

Google Maps is hands down the most underappreciated app and most under monetized tech asset in the world.

Another possible revenue generation avenue would be the advent of Google Maps voice ads en route to a destination that would promote a 5 or 10 second voice commercial of a businesses that the user is physically passing by.

The unintended effects of Google’s audacious transformation of their proprietary Map service spells doom for Yelp’s business model.

Google’s move into digital ads of maps effectively means that Yelp will be relegated to an inferior version of Google Maps without the map technology.

Google has accumulated enough personal data to draw up any type of profile for particularly Android users voraciously consuming data on Gmail, Google Maps, Google Search and Google Chrome.

These four data generators will allow Google to formulate a shadow profile based on individual tastes with daily use of these four Google properties.

Alphabet has a time-honored model of building assets that become utilities and once they monopolize the utility, they sprinkle the digital ad pixie-dust effectively monetizing the asset that was once free of charge.

They have followed the same road map for Gmail, Google Search, YouTube, and if Waymo can become a utility, prepare from Google digital ads inside the screens of Waymo autonomous cars.

When many sulked that this could be one of those billion-dollar failures that Bezos whined about, Google has decided to supercharge Google Maps by cross-pollinating the power of Google maps with its digital advertising knowhow.

This powerful cocktail of forces working in tandem will accelerate its revenue growth along with the resurgence of its YouTube digital ad revenue.

I believe this new lever of revenue growth isn’t priced into Alphabet shares yet, and withstanding any random black swan shocks to the broader economy, Alphabet is poised to outperform the rest of the trading year.

Short Yelp on any and every rally - Google has made their business model redundant.

“If you step back and take a holistic look, I think any reasonable person would say Android is innovating at a pretty fast pace and getting it to users.” – Said CEO of Google Sundar Pichai

Mad Hedge Hot Tips

April 16, 2019

Fiat Lux

The Five Most Important Things That Happened Today

(and what to do about them)

1) Netflix’s Big Day, with the company reporting Q1 earnings after the close. Fears they will get run over by the new Disney juggernaut at one third of the (NFLX) monthly price are running rampant. If they don’t beat on new subscribers look out below. Click here.

2) Manufacturing Output Was Flat, in March says the Fed, thanks to a big drop off in auto production. It’s consistent with the rest of the poor data we have received in recent months. Click here.

3) Citibank Beats in Investment Banking Boost, but the stock market doesn’t buy it. Avoid banks like last year’s buggy maker. Click here.

4) Goldman Sachs to Lay Off 100, in the wake of disappointing Q1 earnings and collapsing trading volumes. Avoid this dying sector. Click here.

5) Goodbye to Notre Dame Cathedral. It really is like saying goodbye to an only friend. I first walked its stone-paved isles in 1968, fleeing riot police from the demonstration out front. Some 50 years later, I guided my wide-eyed kids through its medieval spires. All of Silicon Valley big tech is lining up to help finance the rebuild which will cost hundreds of millions. See you again in 20 years when the job is done.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS, AND WHAT TO DO ABOUT IT),

(BLK)

(UBER’S DARK AND DIRTY SECRETS)

(UBER), (LYFT)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

April 16, 2019

Fiat Lux

Featured Trade:

(UBER’S DARK AND DIRTY SECRETS)

(UBER), (LYFT)

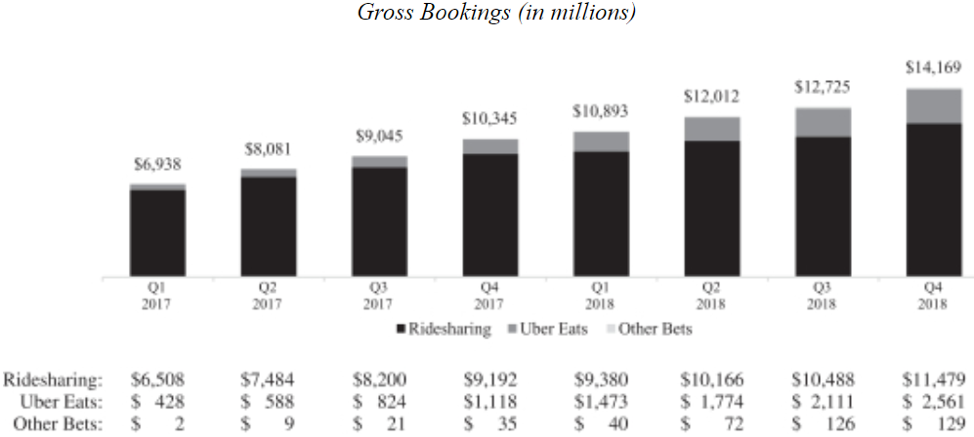

The granddaddy of IPOs awaits us – Uber has filed an S-1 with the SEC detailing plans to go public.

Uber can’t do this any sooner as they preside over a decelerating ride-share operation and its high margin Uber eats division, food delivery business, that has experienced slowing margins.

Once helmed by swashbuckling entrepreneur Travis Kalanick, Uber was infamous for its cultural problems that played out in real time in the media with sexual harassment accusations amongst other things.

They were castigated for its environment of testosterone overload that current CEO Dara Khosrowshahi has rooted out.

Khosrowshahi is pinning the blame on the past leadership in the S-1 filing explaining they are still fine-tuning these problems and its inherent risk could be detrimental to the growth model.

The Iranian-American CEO needs as many outs as he can find because Uber is a high-risk, high-reward model that has revealed no possible way to becoming profitable.

Sequentially, Uber’s core growth has stagnated with revenues last quarter of 2018 coming in at $2.314 billion, decelerating from $2.315 billion in the third quarter.

This is a sensitive spot for Uber because it correlates to 91% of its revenue.

Its Uber Eats division has also presided over two sequential quarters of deceleration indicating the low-hanging fruit has been picked.

The company is shifting towards higher volume, lower margin restaurants in more competitive locations hinting that the gangbuster years of high margin food delivery service growth is over.

The proposed $90 billion IPO also marks the high-water mark to the Silicon Valley IPO parade with only smaller fish from the sea debuting after them.

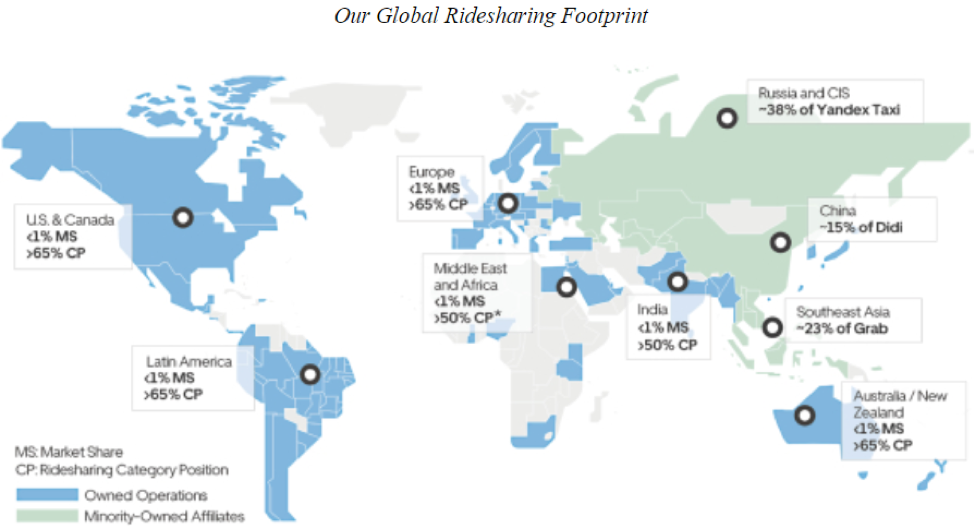

Uber has altered economic and consumer habits as we know it and the size of the business means it’s no Lyft (LYFT) – Uber is global, and its revenues are six times larger than its American competitor.

Becoming an enormous start-up also means heavier losses, the company had $3 billion in operating losses last year while its smaller competitor Lyft had only $911 million.

Lyft is solely focused on the ride-share industry capping upside potential while Uber has more gunpowder to load if it wants to ammo up in the business world.

One direction Uber hopes to explore is under the banner of Uber Freight which plans to monetize the deeply fragmented logistic industry.

It can take sometimes days for suppliers to deliver shipments with most of the process conducted over the phone or by fax.

Uber Freight mitigates logistical risks by providing an on-demand platform to automate and accelerate logistics transactions end-to-end.

The software smoothly connects carriers with the most appropriate shipments available, and offers carriers upfront, transparent pricing and the ability to book a shipment with the touch of a button.

As of the end of 2018, Uber Freight delivered $125 million in annual revenue and they hope to ameliorate many of the same logistical pain points that occur around the world.

This division of Uber is one that Lyft lacks, thus Uber should be granted a higher multiple when shares go public.

A huge addressable market awaits Uber Freight, but as many know, logistic routes have been formed over many years, and disruptors won’t be able to come in overnight and sign up new contracts.

Revenue should be slow but steady, and not the sugar high rush of revenue management is wishing for.

Uber’s heavy cash burning enterprise needs to offer some glimmer of hope of becoming profitable in the future whether it's five or twenty years out.

Without this x-factor of potential profitability, committed capital could become strained as investor will shy away knowing that a solid balance sheet might be a pie in the sky.

Since 2015, Uber has paid drivers $78.2 billion in renumeration - Uber will need to curtail heavy costs like these to raise operating margins.

One upside to its model is that its software platform possesses synergetic effects cutting costs for rolling out newer software for Uber Freight and Uber Eats.

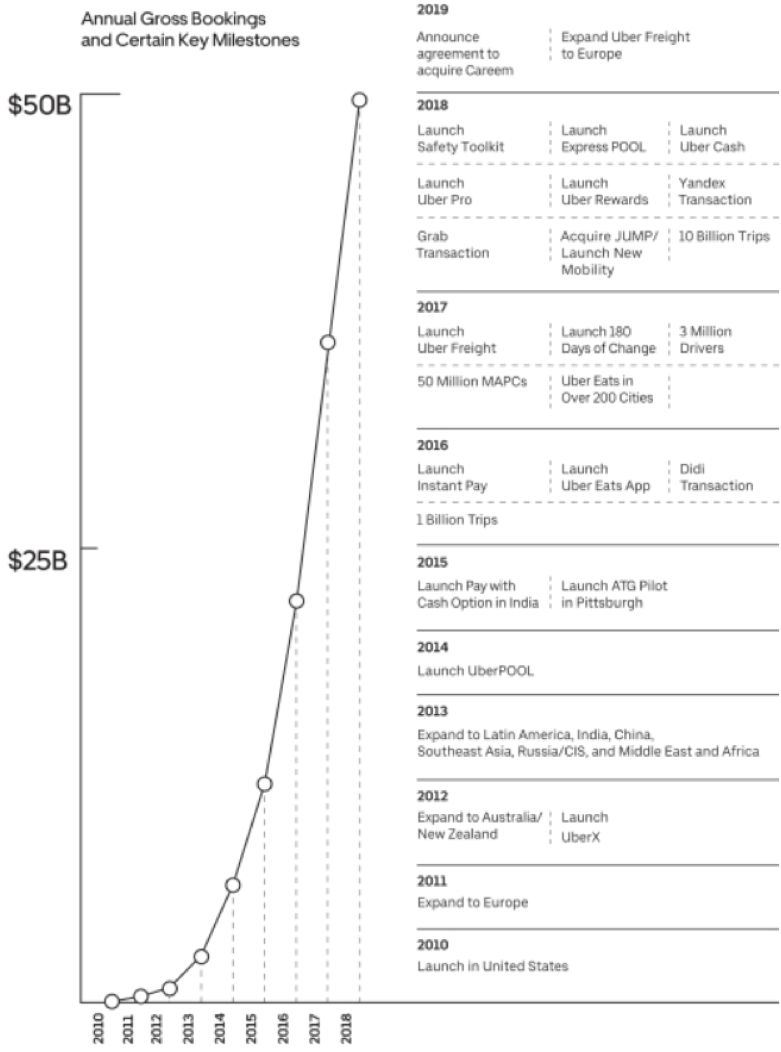

Uber is still growing, albeit at a slower rate, 2018 Gross Bookings grew to $49.8 billion, up 45% from $34.4 billion in 2017.

The growth contributed to revenues of $11.3 billion in 2018. While a mammoth number, Uber still needs to absorb capital hits from M&A when they acquired Careem, the Uber of Middle East, North Africa, and Pakistan, for $3.1 billion last year.

Uber clearly choreographed a future strategy in the S-1 filing saying, “Our strategy is to create the largest network in each market so that we can have the greatest liquidity network effect, which we believe leads to a margin advantage.”

Details of this strategy include more drivers, more riders, more rides per hour, lower fares, and smaller waiting times.

I believe Uber is biting off more than they can chew on this front.

To overcome the regulatory hurdles and the social backlash while offering cheaper fares and simultaneously increasing driver payout will be impossible unless drivers start shuttling around 5 or 6 people in one ride.

I do acknowledge that Uber has massive scale, first move advantage, and a handsome margin advantage working on their side.

But will this be enough if Uber adds more drivers and effectively piles more money into the same strategy?

I would say no and that could mean that growth rates could slip severely which leads me to suggest that Uber has a problem with the quality of growth.

On the bright side, the business model with be compensated by enhancements in the routing algorithms, payment technologies, in-car user experience, and user interface.

These incremental gains won’t help offset the relative weakness in the growth numbers that possess less and less quality in them.

The overarching theme of what to do when the low-hanging fruit is picked off the branch is a tough one, because any further incremental gain is negated by higher costs or competition.

Uber’s get out of jail free card is the eventual paradigm shift to aerial ride sharing, and if they are the leaders in that transition, it could offer another massive pay day and steeper growth trajectory that would propel the company into a realm of many more possibilities.

Whether Uber can complete this tectonic shift is too far away to predict, time could become a significant headwind in this case since mainstream adoption of autonomous driving has been relatively sluggish.

Expect heightened volatility as the main characteristics of Uber’s price action - it’s certain to be a bumpy ride.

Abstaining from Uber shares would be the smart play here while some more detective work can be deployed.