Mad Hedge Biotech & Healthcare Letter

October 5, 2021

Fiat Lux

FEATURED TRADE:

(A BIOTECH STOCK THAT LETS YOU SLEEP THROUGH THE NIGHT)

(AMGN), (AZN), (GSK), (REGN), (SNY), (MRK)

Mad Hedge Biotech & Healthcare Letter

October 5, 2021

Fiat Lux

FEATURED TRADE:

(A BIOTECH STOCK THAT LETS YOU SLEEP THROUGH THE NIGHT)

(AMGN), (AZN), (GSK), (REGN), (SNY), (MRK)

Great investors have learned that the critical element when it comes to long-term investing is concentrating on stocks that hold a profound presence in their fields and that will continue to grow in the decades to come.

In terms of trends, the best thing to do is to determine something that will affect the world by generating millions—if not billions—of steady customers.

Among the stocks in the biotech industry today, one stands out to benefit from solid future demand for its products: Amgen (AMGN).

Amgen is one of the biggest biopharmaceutical companies across the globe, holding an equity market capitalization of roughly $127 billion. Despite its size, it simply can’t quite catch a break, with its share price continuing to slide in the past week.

While short-term investors may see this as a weakness, it’s moments like these that distinguish genuine value investors from the rest.

Let’s take a look at a company that has been thrown in the bargain bin for no apparent reason, and understand why this could be our opportunity.

A recent promising addition to Amgen’s pipeline is its experimental asthma drug, Tezepelumab, which it’s co-developing with AstraZeneca (AZN).

There are approximately 2.5 million patients worldwide who suffer from severe, uncontrolled asthma, accounting for almost 50% of all asthma-related expenses in the healthcare system.

This is because the majority of the 439,000 asthma-related hospitalizations, as well as 1.3 million emergency room visits annually in the US alone, are caused by severe, uncontrolled asthma.

Moreover, it was found that 1 in 5 severe asthma patients tend to develop a benign growth called nasal polyps in the sinuses of their noses. These can end up blocking their nasal passages, worsening their breathing problems, and diminishing their sense of smell.

This is the very market that Amgen’s Tezepelumab targets to help.

Tezepelumab is the first and only treatment that focuses on the symptoms of severe, uncontrolled asthma patients.

Considering the positive results of its late-stage trials, Amgen and AstraZeneca are confident that Tezepelumab will receive regulatory approval from the US FDA by the first quarter of 2022.

When that happens, this will mark Amgen’s first-ever foray into the asthma treatment sector—and it’s entering the market with a potential blockbuster to boot.

The global asthma market is projected to grow from $20.6 billion in 2020 to $37.3 billion in revenue by 2030.

So far, the other names aiming to dominate this segment include GlaxoSmithKline (GSK), Regeneron (REGN), and Sanofi (SNY).

Considering the competition, a modest estimate is to expect Tezepelumab to seize at least 5% of the market share following its approval.

That would work out to roughly $1.9 billion in yearly revenue, divided between AstraZeneca and Amgen.

Taking into account that Amgen is forecasting its 2021 revenue to be within the range of $25.8 billion and $26.6 billion, the addition of $1 billion annually would surely move the needle.

Moreover, the cherry on top is that Tezepelumab is a clear indicator of the company’s efforts to diversify its revenue base and enter a market that it has yet to establish its presence.

Apart from Tezepelumab, Amgen has also been working on expanding its blockbuster lung cancer drug Lumakras, which generated $2.5 billion in annual sales.

To date, Lumakras is expected to emerge as a solid contender to unseat Merck’s (MRK) Keytruda in the lung cancer segment.

In addition, the company is studying how to utilize Lumakras as a potential treatment for colorectal cancer.

Amgen has also been expanding its pipeline of biosimilar candidates.

The most exciting candidates include its biologic version of Johnson & Johnson’s (JNJ) psoriatic arthritis and psoriasis medication Stelara, Regeneron’s chronic eye disease drug Eylea, and AstraZeneca’s rare disease treatment Soliris.

Even AbbVie’s (ABBV) impending loss of exclusivity for its top-selling rheumatoid arthritis drug Humira is under the company’s radar, with Amgen already prepared to launch its own biosimilar domestically in the form of Amjevita by 2023.

Getting the regulatory green light for these treatments would allow Amgen to poach on hundreds of millions, if not billions, in annual revenue from its competitors.

Apart from its pipeline candidates and strong performance in niche segments, Amgen has demonstrated a solid track record when it comes to capital returns via share buybacks.

In the second quarter of 2021 alone, the company has splurged on 6.5 million in shares repurchases. Amgen expects to reach a total of $3 billion to $5 billion in total repurchases throughout the year.

This strategy has pushed Amgen in its goal to continuously deliver market-beating returns in the past decade, as shown by its 451% total—overtaking the 384% return of the S&P 500.

Buying shares of a company when it’s declining can be an excellent step to set yourself up for future gains when the stock bounces back.

However, not all struggling stocks can recover.

So, it’s crucial to determine the reason for their fall. If the business itself is stable and solid, a decline in value might just be the opportunity you need to invest.

The truth is, nothing has actually changed when it comes to Amgen’s long-term stock growth prospects. It's still the company with a slew of top-selling products and more pipeline candidates expected to become blockbusters in the coming years.

All told, Amgen holds roughly 20 revenue-generating products in its diverse portfolio, and not a single drug accounts for over 20% of the company’s continuously rising top line.

Overall, I think Amgen is an A-rated company with a reasonable yield and a promising upside.

Mad Hedge Bitcoin Letter

October 5, 2021

Fiat Lux

Featured Trade:

(ARE ALTCOINS RELEVANT?)

(BTC), (ETH)

“Bitcoin is a swarm of cyber hornets serving the goddess of wisdom, feeding on the fire of truth, exponentially growing ever smarter, faster, and stronger behind a wall of encrypted energy.” – Said CEO of MicroStrategy Michael Saylor

Global Market Comments

October 5, 2021

Fiat Lux

Featured Trade:

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)

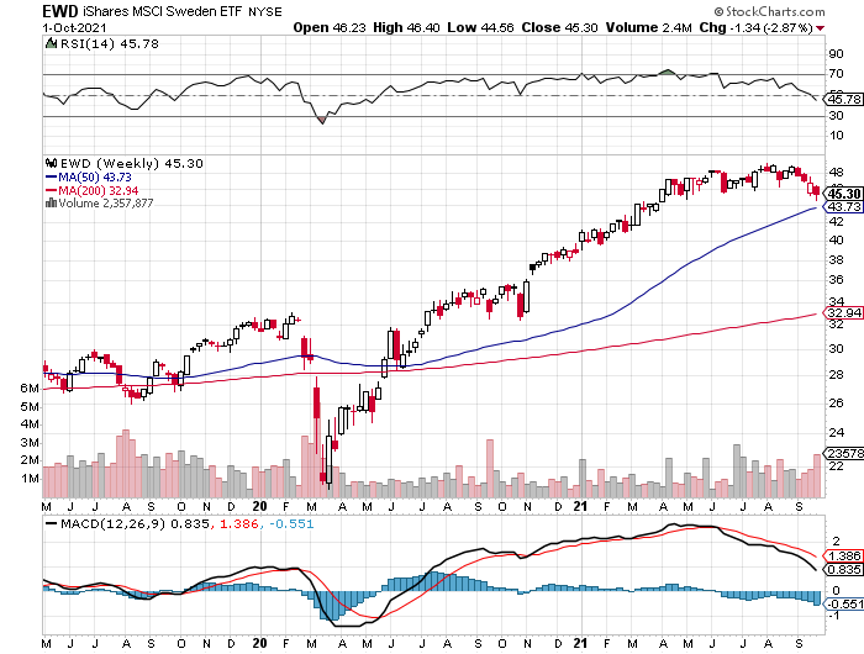

(THANK GOODNESS, I DON’T LIVE IN SWEDEN)

(EWD)

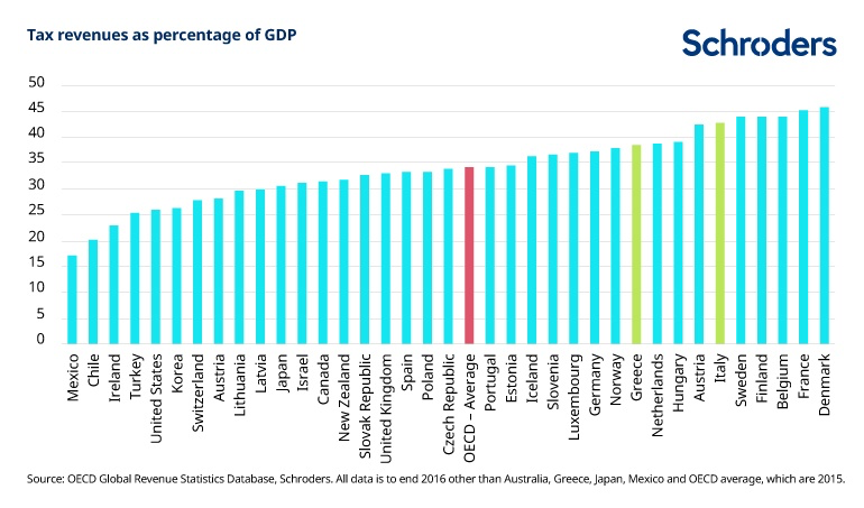

I recently found the chart below showing world tax rates as a percentage of GDP for the past 40 years. Sweden suffers the world's heaviest tax burden at 51%, compared to only 27% in the US.

The US has among the world's lowest tax burdens in terms of actual taxes paid which has been falling for the last 15 years.

Listening to TV pundits, you would think we had the world's highest tax rates. They are dead wrong.

Germany, home to some of the world's best-run and most profitable companies which make the Fatherland a major exporter, has one of the lowest tax bills.

Iceland sits at the bottom and recently went bankrupt, thanks to an overdose of free-market deregulatory philosophy.

Americans historically have had a very strong resistance to taxation which you can trace back to the libertarian foundations of the country.

The Revolutionary War in which 17 of my known ancestors fought was primarily about taxes.

The top end of the distribution is packed with European nations but you never hear them complain about high tax rates.

Most believe the cost of the social safety net is worth it. Those that don't move to the US, Monte Carlo, Lichtenstein, or the British Virgin Islands.

Of course, having once been a part-owner in a fashion model agency in Stockholm, I can certainly vouch for the advantages of living in the world's most taxed domicile. Hedge fund profits go a long way there.

Suffice to say, you spend a lot of time indoors in the home of the Vikings, especially in the winter.

Things could be worse.

Mad Hedge Technology Letter

October 4, 2021

Fiat Lux

Featured Trade:

(IT WILL JUST TAKE LONGER)

(ROKU), (TSLA), (FB), (AMZN), (AAPL)

The “Buy the Dip” strategy in tech stocks hasn’t failed — it will just take longer than it used to.

Much of this Nasdaq rally has been represented by the resiliency of large cap tech stocks — every mini dip was bought with a vengeance.

This go-to playbook drove tech shares higher after the March 2020 meltdown.

These past 30 days have really tested that thesis and signals that we, as market participants, have arrived at a crossroads because if the dip isn’t bought soon, we could either fall off a ledge and barrel into a harrowing correction or we could initiate a sideways correction and trade in a fixed range.

It’s hard to ignore the near-term weakness in many of the household names like Apple (AAPL), Amazon (AMZN), and Facebook (FB).

The upper echelon of tech leadership is signaling imminent decelerating growth and tightening financial conditions.

I do believe much of it is in the price, yet it’s cognizant to know there could be meaningful spillover from the Evergrande debt implosion in China into other asset classes.

External events are shaping the narrative around the Nasdaq dip buyers.

It also doesn’t help that a Facebook whistleblower came forward to tell the press about its malpractices and less than ideal tendencies to put profit over safety, but everyone already knew that about Facebook.

What I am surprised about is that investors usually look through the bad Facebook press and prioritize the metrics which hasn’t been happening the past month.

Facebook shares are still waiting to be bought after the dip.

The lack of Facebook shoppers on the pullback is definitely one area of concern because the U.S. government still has done very little to stop Facebook in its stubborn practices.

The U.S. government will not crack down through legislation on social media companies in the short term.

Much of the negative Nasdaq price action in the short term can be attributed to the worries about China taking a machete to its susceptible tech sector and crushing it even more.

Many don’t think the cudgeling is over.

In this scenario, a flight to safety could be in the cards, which would suppress interest rates offering an olive branch for the dip-buyers.

Ultimately, I do believe it’s a matter of time before we get some recovery price action in the leadership tech stocks; but yes, it could take 1-3 weeks.

Much of this second half of the year was consolidating tech shares that overshot themselves last year.

That’s why tech firms like Tesla (TSLA) had almost a zero percent chance of repeating last year’s performance.

Take ad tech stock Roku (ROKU) for instance, shares are down 23% YTD and that doesn’t mean it’s a bad stock.

Hardly so.

When one considers that Roku shares ended 2020 up 300%, then giving back 23% or 50% in 2021 is worth the annoyances.

These stocks can’t go up in a straight line even if they almost feel like they can sometimes.

This all sets up for a brilliant 2022, as many of these high-quality names will finally have gotten through the consolidation phase and will be buttered up to initiate their next leg up in early 2022.

In the broad scheme of things, tech won the pandemic over any other sector, and 2021 is turning into a rest year.

Sometimes one needs to go backwards one step to take the next three forward.

“Creativity is just connecting things.” – Said Co-Founder of Apple Steve Jobs

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more