Those of you counting on getting your old union assembly line job back in Detroit can forget it.

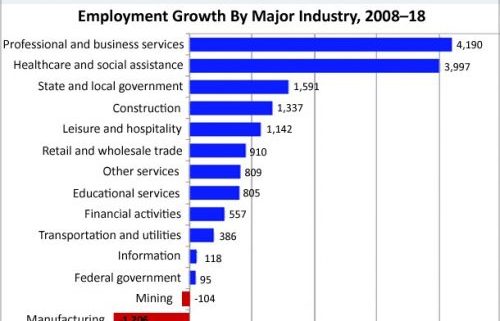

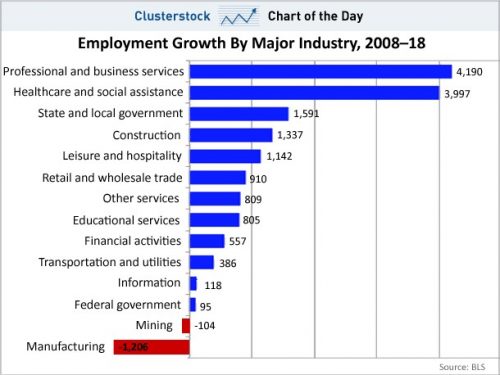

The eight-year forecast published by the Bureau of Labor Statistics shows that 4.19 million jobs will be gained in the U.S. in professional and business services, followed by 4 million health care and social assistance jobs, while 1.2 million will be lost in manufacturing.

This is great news for website designers, Internet entrepreneurs, registered nurses, and masseuses in California, but grim tidings for traditional metal bashers in the rust belt manufacturing states such as Michigan, Indiana, and Ohio.

I’m so old now that I am no longer asked for a driver’s license to get into a nightclub. Instead, they ask for carbon dating.

The real challenge for us aged career advisors is that probably half of these new service jobs haven’t even been invented yet, and if they can be described, it is only in a cheesy science fiction paperback with a half-dressed blond on the front cover.

After all, who heard of a webmaster, a cell phone contract sales person, or a blogger 40 years ago?

Where are all these jobs going to? You guessed it, China, which by my calculation has imported 25 million jobs from the U.S. over the past decade.

You can also blame other lower waged, upstream manufacturing countries such as Vietnam, where the Middle Kingdom is increasingly subcontracting its own offshoring.

These forecasts may be optimistic because they assume that Americans can continue to claw their way up the value chain in the global economy, and not get stuck along the way, as the Japanese did in the 90s.

The U.S. desperately needs no less than 27 million new jobs to soak up natural population and immigration growth and get us back to a traditional 5% unemployment rate.

The only way that is going to happen is for America to invent something new, big, and fast.

Personal computers achieved this during the 80s, and the Internet did the trick in the 90s. The fact that we’ve done squat since 2000 but create a giant paper chase of subprime loans and derivatives explains why job growth since then has been zero, real wage growth has been negative, and American standards of living are falling.

While the current crop of politicians extols the virtues of education, the reality is that we are dumbing down our public education system. How do we invent the next “new” thing, while shrinking the University of California’s budget by 25% two years in a row?

If my local high school can’t afford new computers, how is it going to feed Silicon Valley with a computer literate workforce? The U.S. has a “Michael Jackson” economy. It’s still living like a rock star but hasn’t had a hit in 20 years.

China can have all the $20 a day jobs it wants. But if it accelerates its move up the value chain as it clearly aspires to do, then America is in for even harder times.

I’ll be hoping for the best but preparing for the worst. How do you say “unemployment check” in Mandarin?

Is This Your Future?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Employment-growth-chart-story-2-image-1-e1526422265887.jpg375500MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-05-29 01:02:142019-07-09 03:41:43Kiss That Union Job Goodbye

We are now in the throes of a market correction that could last anywhere from a couple of more week to a couple of months. So, generational opportunities are starting to open up in some of the best long term market sectors.

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California’s largest export (it’s not grapes). But such a fund DOES exist.

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a golden opportunity into investors’ laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.2 billion in assets under management.

The universal trend of preferring automation over human labor is spreading with each passing day. Suffice to say there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don’t complain, don’t fall ill, don’t join unions, or don’t ask for pay rises. It’s all very much a capitalist’s dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it’s not online dating, gambling, or bitcoin. It’s Artificial Intelligence.

Selecting individual stocks that are purely exposed to AI is a challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure AI plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated AI play out there. A real diamond in the rough.

The best way to expose yourself to this AI trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit at the forefront of the AI and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and AI walk hand in hand, and robotics are entirely dependent on the germination prospects of AI. Without AI, robots are just a clunk of heavy metal.

Robots require a high level of AI to meld seamlessly into our workforce. The stronger the AI functions, the stronger the robot’s ability, filtering down to the bottom line.

AI-embedded robots are especially prevalent in military, car manufacturing, and heavy machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotic industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let’s get the ball rolling and familiarize readers of the Global Trading Dispatch with the top 5 weightings in the underlying ETF (BOTZ).

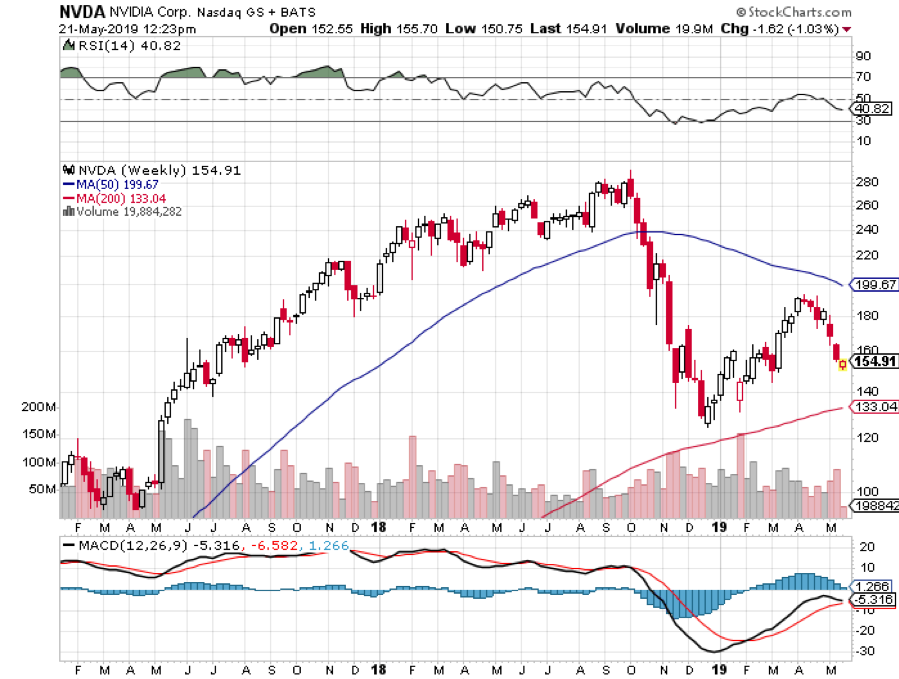

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California-based company is spearheading the next wave of AI advancement by focusing on autonomous vehicle technology and AI-integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state of the art IOT products (internet of things), fueled by GPU chips coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese American, who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Yaskawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improving global productivity through automation. It comprises the 2nd largest portion of BOTZ at 8.35%.

Fanuc was another one of the hot robotics companies I used to trade in during the 1970s, and I have visited their main factory many times.

The 3rd largest portion in the (BOTZ) ETF at 7.78% is Fanuc Corp. This company provides automation products and computer numerical control systems and is headquartered in Oshino, Yamanashi.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is completely industriously focused on the medical industry.

The company's da Vinci Surgical System converts surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3D vision systems, da Vinci skills simulators, da Vinci Xi integrated table motions.

This company comprises 7.60% of BOTZ. To visit their website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscope.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-popping 50% operating margin.

They are headquartered in Osaka, Japan and make up 7.54% of the BOTZ ETF.

(BOTZ) does have some pros and cons. The best AI plays are either still private at the venture capital level or have already been taken over by giant firms like NVIDIA.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many of the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don’t have their own robotic-led business pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ), please visit their website by clicking here.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2019-05-22 01:04:162019-07-09 03:43:12Here's an Easy Way to Play Artificial Intelligence

There is no doubt that the Bellagio Hotel in Las Vegas took on a different character during the first week of May.

Walking out to the pool I ran into David Rubenstein wearing his fancy jogging outfit. He is a co-founder of the Carlyle Group, the world’s preeminent private equity fund.

I listened in on a heated hallway argument between the ever-combative Chris Christie, the former governor of New Jersey, recently retired US attorney general Jeff Sessions, and former New York governor Rudy Giuliani.

The diminutive real estate mogul Sam Zell was holding down a table of admirers for morning coffee.

Oh, and I spent an evening rocking out with legendary venture capitalist Tim Draper, listening to John Fogerty, once of Credence Clearwater Revival. John played his entire set from Woodstock 51 years ago.

The magnet drawing all of these disparate luminaries together was the 2019 SALT conference, assembled by the ever-peripatetic financial entrepreneur and showman Anthony Scaramucci.

I have known Anthony for at least a decade, founder and co-managing director of Skybridge Capital, an allocator of funds to alternative asset management strategies. You may know him as Donald Trump’s press secretary who lasted in the position all of 11 days, depending on how you count.

The mood at the conference was what you might expect in the tenth year of a bull market. Most were bullish, but nervous, as new uncertainties pile up.

As in past years, Anthony delivered a lineup of speakers that was nothing less than blue chip. They included my old friend, USMC general John Kelley, most recently the president’s chief of staff, former Obama advisor Valerie Jarret, artificial intelligence wizard Kai-Fu Lee, Broadcast.com founder and well known “shark” Mark Cuban, and Dr. Nouriel Roubini, otherwise known as “Dr. Doom”, who lived up to his reputation as usual.

Strolling through the coffee lounge between sessions a number of incredibly beautiful young women suddenly found me very attractive. Perhaps they noticed the words “hedge fund” on my name tag. It turned out they were marketing back office services.

Over lunch, I listened to Drs. Bob Hariri and David S. Karow speak of the wonders of placental stem cell technology, which promises to extend our lives by decades. I was an early stem cell user, thanks to my daily hiking regime that wore out my knees. It works.

General David Petraeus and former UN Ambassador Susan Rice discussed solutions for our difficulties in the Middle East. Peter Schiff and Barry Silbert debated the safe haven characteristics of gold versus Bitcoin.

My Incline Village, Nevada neighbor Michael Milken talked about how capital drives rapid technology innovation. I thanked Mike for paying for the town’s annual Fourth of July fireworks budget, which happens to be his birthday.

Anyone with kids knows well Sal Khan, founder of Khan Academy, the renown online tutoring platform. Khan originally started the project in an attempt to help his many relatives with math homework. It now assists millions across 163 countries and is funded by Microsoft founder Bill Gates. By the end of 2018, Khan Academy videos had accumulated over 1.8 billion views on Google’s YouTube.

I ran into another old friend Jon Najarian at one of the nightly pool parties. I have seen former Minnesota Viking Jon reinvent himself over the years more often than I change my socks. Most recently, he is running a family office and marketing various financial products. He still breaks a few bones every time he shakes your hand.

By Friday morning the guests were packing up and heading to McCarran Airport, or to the private jet terminal at Henderson, where I have kept a share in a plane for years for my Grand Canyon jaunts.

I noticed one of the earlier mentioned marketers buying a $695 pair of Christian Louboutin shoes, you know, the ones with the red bottoms? Clearly, they had been successful in their sales efforts.

For more about the 2019 SALT conference, please click here.

For more about Skybridge Capital, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/john-thomas-5.png387516Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-21 02:02:592019-07-09 03:43:24Report from the 2019 Las Vegas SALT Conference

Whatever the market is drinking right now, I’ll take some of that stuff. If you could bottle it and sell it, you’d be rich. Certainly, the Viagra business would go broke.

To see the Dow average only give up 7% in response to the worst trade war in a century is nothing less than stunning. To see it then make half of that back in the next four days is even more amazing. But then, that is the world we live in now.

When the stock market shrugs off the causes of the last great depression like it’s nothing, you have to reexamine the root causes of the bull market. It’s all about the Fed, the Fed, the Fed.

Our August central bank’s decision to cancel all interest rate rises for a year provided a major tailwind for share prices at the end of 2018. The ending of quantitative tightening six months early injected the steroids, some $50 billion in new cash for the economy per month.

We now have a free Fed put option on share prices. Even if we did enter another 4,500-point swan dive, most now believe that the Fed will counter with more interest rate cuts, thanks to extreme pressure from Washington. A high stock market is seen as crucial to winning the 2020 presidential election.

Furthermore, permabulls are poo-pooing the threat to the US economy the China (FXI) trade war presents. Some $500 billion in Chinese exports barely dent the $21.3 trillion US GDP. It’s not even a lot for China, amounting to 3.7% of their $13.4 trillion GDP, or so the argument goes.

Here’s the problem with that logic. The lack of a $5 part from China can ground the manufacture of $30 million aircraft when there are no domestic alternatives. Similarly, millions of small online businesses, mostly based in the Midwest, couldn’t survive a 25% price increase in the cost of their inventory.

As for the Chinese, while trade with us is only 3.7% of their economy, it most likely accounts for 90% of their profits. That’s why the Chinese yuan (CYB) has recently been in free fall in a desperate attempt to offset punitive tariffs with a substantially cheaper currency.

The market will figure out all of this eventually on a delayed basis and probably in a few months when slowing economic growth becomes undeniable. However, the answer for now is NOT YET!

Markets can be dumb, poor sighted, and mostly deaf animals. It takes them a while to see the obvious. One of the problems with seeing things before the rest of the world does, I can be early on trades, and that can translate into losing money. So, I have to be cautious here.

When that happens, I revert to an approach I call “Trading devoid of the thought process.” When prices are high, I sell. When they are low, I buy. All other information is noise. And I keep my size small and stop out of losers lightning fast. That’s how I managed to eke out a modest 0.63% profit so far this month, despite horrendous trading conditions.

You have to trade the market you have, not what it should be, or what you wish you had. It goes without saying that the Mad Hedge Market Timing Index become an incredibly valuable tool in such conditions.

It was a volatile week, to say the least.

China retaliated, raising tariffs on US goods, ratcheting up the trade war. US markets were crushed with the Dow average down 720 intraday and Chinese plays like Apple (AAPL) and Boeing (BA) especially hard hit.

China tariffs are to cost US households $500 each in rising import costs. Don’t point at me! I buy all American with my Tesla (TSLA).

The China tariffs delivered the largest tax increases in history, some $72 billion according to US Treasury figures. With Walmart (WMT) already issuing warnings on coming price hikes, we should sit up and take notice. It is a highly regressive tax hike, with the poorest hardest hit.

The Atlanta Fed already axed growth prospects for Q2, from 3.2% to 1.1%. This trade war is getting expensive. No wonder stocks have been in a swan dive.

US Retail Sales cratered in March while Industrial Production was off 0.5%. Why is the data suddenly turning recessionary? It isn’t even reflecting the escalated trade war yet.

European auto tariff delay boosted markets in one of the administration’s daily attempts to manipulate the stock market and guarantee support of Michigan, Wisconsin, and Pennsylvania during the next presidential election. All government decisions are now political all the time.

Weekly Jobless Claims plunged by 16,000 to 212,000. Have you noticed how dumb support staff have recently become? I have started asking workers how long they have been at their jobs and the average so far is three months. No one knows anything. This is what a full employment economy gets you.

Four oil tankers were attacked at the Saudi port of Fujairah, sending oil soaring. America’s “two war” strategy may be put to the test, with the US attacking Iran and North Korea simultaneously.

Bitcoin topped 8,000, on a massive “RISK OFF” trade, now double its December low. The cryptocurrency is clearly replacing gold as the fear trade.

The Mad Hedge Fund Trader managed to blast through to a new all-time high last week.

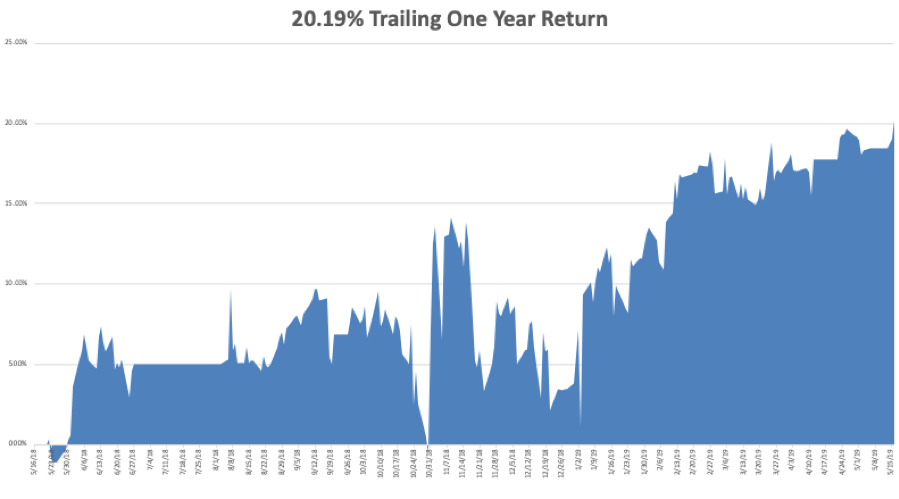

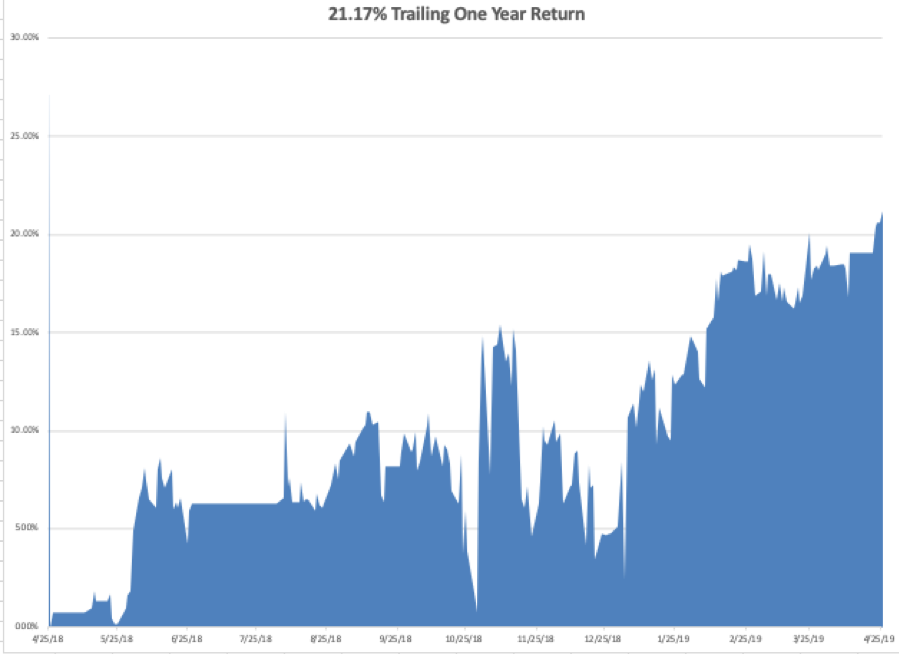

Global Trading Dispatch closed the week up 16.35% year to date and is up 0.63% so far in May. My trailing one-year rose to +20.19%. We jumped in and out of short positions in bonds (TLT) for a small profit, and our tech positions appreciated.

The Mad Hedge Technology Letter did OK, making some good money with a long position in Intuit (INTU) but stopping out for a small loss in Alphabet (GOOGL).

Some 10 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

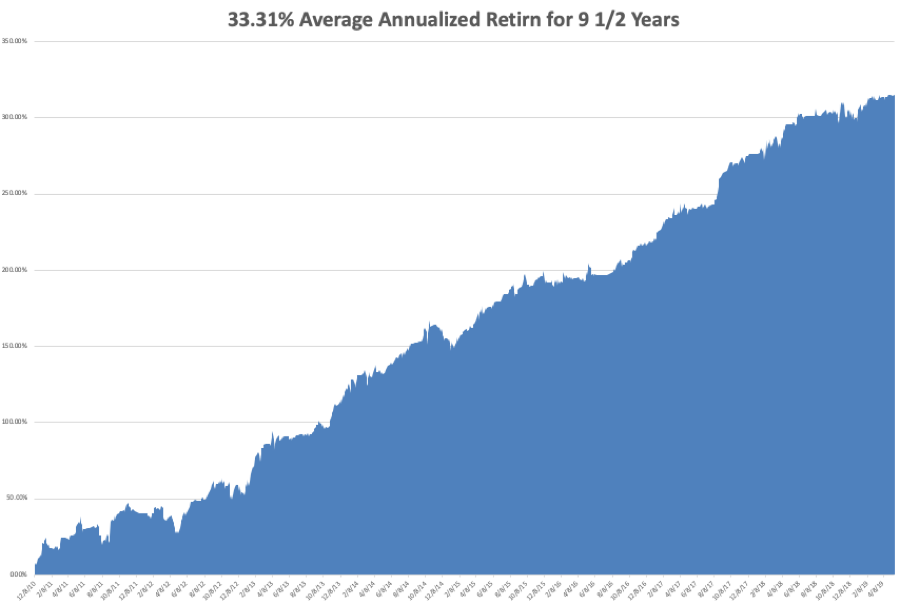

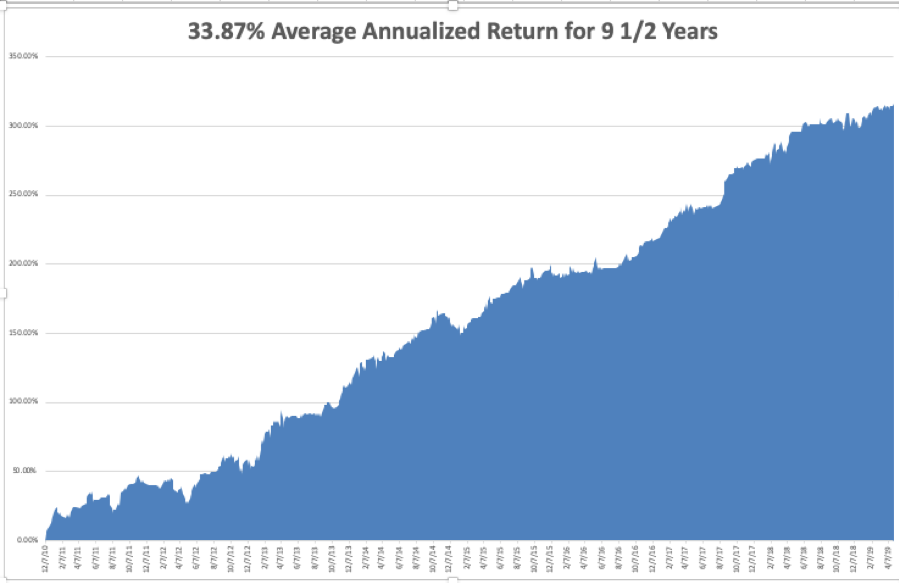

My nine and a half year profit jumped to +316.49%.The average annualized return popped to +33.21%. With the markets incredibly and dangerously volatile, I am now 80% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets retest the bottom end of the recent range before considering another long position.

The coming week will see only one report of any real importance, the Fed Minutes on Wednesday afternoon. Q1 earnings are almost done.

On Monday, May 20 at 8:30 AM, the April Chicago Fed National Activity Index is out.

On Tuesday, May 21, 10:00 AM EST, the April Existing Home Sales is released. Home Depot (HD) announces earnings.

On Wednesday, May 22 at 2:00 PM, the minutes of the last FOMC Meeting are published. Lowes (LOW) announces earnings.

On Thursday, May 16 at 23 AM, Weekly Jobless Claims are published. Intuit (INTU) announces earnings.

On Friday, May 24 at 8:30 AM, April Durable Goods is announced.

As for me, I’ll be taking a carload of Boy Scouts to volunteer at the Oakland Food Bank to help distribute food to the poor and the homeless. Despite living in the richest and highest paid urban area in the world, some 20% of the population now lives on handouts, including many public employees and members of the military. It truly is a have, or have-not economy.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/john-thomas-3.png816612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-20 02:02:272019-07-09 03:43:34The Market Outlook for the Week Ahead, or I’ll Take Some of That!

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 15 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Where are we with Microsoft (MSFT)?

A: I think Microsoft is really trying to bottom here. It’s only giving up $8 from its recent high, that's why I went long yesterday, and you can be hyper-conservative and only do the June $110-$115 vertical bull call spread like I did. That will bring in a 13.68% profit in 28 trading days, which these days is pretty good. This morning would have been a great entry point for that spread if you couldn’t get it yesterday.

Q: How will tariffs affect Apple (AAPL) when they hit?

A: The price of your iPhone goes up $140—that calculation has already been done. All of Apple's iPhones are made in China, something like 220 million a year. There’s no way that can be moved, they need a million people for the production of these phones. It took them 20 years to build that facility and production capacity; it would take them 20 years to move it and it couldn't be done anywhere else in the world. So, that's why Apple led the charge on the downside and that's why it will lead the charge to the upside on any trade war resolution.

Q: How bad is the trade war going to get?

A: The market is betting now by only going down 1,400 Dow points it will be resolved on June 28th in Osaka. If that doesn’t happen it could get a lot worse. It could get down to my down 2,250-point target, and if it continues much beyond that, then we’ll get the whole full 4,500 points and be back at December lows. After that, you’re really looking at a global recession, a global depression, and ultimately nearing 18,000 in Dow, the 2016 low.

Q: Will global trade wars force US Treasuries down to around 2.10% on the ten year?

A: Yes. Again, the question is how bad will it get? If we resolve the trade war in six weeks, treasuries will probably double bottom here at around a 2.33% yield. If we go beyond that, then 2.10% is a chip shot and we go into a real live recession. The truth is no one knows anything, and we really don’t have any influence over what happens.

Q: How will equities digest and increase in European tariffs for cars?

A: It would completely demolish the European economy—especially that of Germany (EWG) which has 50% of its economy dependent on exports (primarily cars) and mostly to the U.S. And if we wipe out our biggest customer, Europe, then that would spill over here very quickly. Anybody who sells to Europe—like all the big Tech companies—would get slaughtered in that situation.

Q: Is it time to buy the Volatility Index (VIX)?

A: It’s too late to buy (VIX) now. I don’t want to touch it until we get down to that $12-$13 handle again because the time decay on this is enormous. Time decay is more than 50% a year, so your timing has to be perfect with trading any (VIX) products, whether it’s the (VXX), the (VIX) futures, the (VIX) options, or so on. There are countless people shorting (VIX) here, and they will short it all the way down to $12 again.

Q: What should I do about Boeing at this point?

A: We went long, got out, took our profit and caught this rally up to $400 a share. Then (BA) gave it up and it broke down. It’s a really tempting long here. Along with Apple, Boeing has the largest value of exports to China of any company. They have orders for hundreds of airlines from China, so they are an easy target, especially if there is a ramp up in the intensity of the trade war. That said, something like a June $270-$300 vertical bull call spread is very tempting, especially with elevated volatility up here, so I’m watching that very closely. We’re looking for the recertification of the 737 MAX bounce which could happen in the next few weeks; if that does happen it should rally at least back up to 380.

Q: Are your moving averages simple or exponential?

A: I just use the simple. I find that the simpler a concept is, the more people can understand it, and the more people buy it; that’s why I always try to keep everything simple and leave the algorithms for the computers.

Q: What stocks are insulated from a US/China trade war?

A: None. When the whole market goes risk off, people sell everything. Remember that an overwhelming portion of the market is now indexed with passive investment funds, so they just go straight risk on/risk off. It makes no difference what the fundamentals are, it makes no difference who has a lot of Chinese business or a little—everyone gets hit and everyone will get boosted when the trade war ends. There is no place to hide except cash, which is why I went 100% cash going into this. People seem to forget that cash has option value and having a lot of cash going into one of these situations is actually worth a lot of money in terms of opportunities.

Q: Do you have any thoughts on Uber’s (UBER) bad performance?

A: Yes, the whole sector was wildly overvalued, but no one knew that until they brought it to market and found out the real supply and demand for the issue. The smartest company of the year has to be Lyft (LYFT), which got a nice valuation by doing their issue first and keeping it small. So, they kind of rained on Uber’s parade; at one point, Uber was down 25% from their IPO price. That’s awful.

Q: Is Trump forcing the Fed to drop rates with all this tariff threat?

A: Yes, and if you remember, Trump really ramped up the attacks on the Fed in December. And my bet is at the first sign the trade talks were in trouble, they wanted to lower rates to offset the hit to the U.S. economy. There was no economic reason to suddenly demand huge interest rate cuts last December other than a falling stock market. The tariffs amount to a $72 billion tax increase on the American consumer, felt mostly at the low end, and that is terrible for the economy in that it reduces purchasing power by exactly that much.

Q: Would you buy the dollar as a safe haven trade?

A: No, I would not. The dollar may actually go down some more, especially with the collapse in our interest rates and European interest rates bottoming at negative levels. The best thing in the world in a high-risk environment like this is cash—don’t try to get clever and buy something you think will outperform. You could be disappointed.

Q: Why is healthcare (XLV) behaving so badly?

A: You don’t want to get into political football ahead of an election. That said, they're already so cheap that any kind of recovery could very well take healthcare up big, especially on an individual company basis. This is a sector where individual stock selection is crucial.

Q: Would you buy deep in the money calls on PayPal (PYPL)?

A: Yes, I would. Wait for a down day. Today we’re up slightly, but if we have a weak afternoon and a weak opening tomorrow morning, that would be a good time to add more longs in technology. PayPal is absolutely at the top of the list, as are names like Adobe (ADBE) and Alphabet (GOOGL).

Q: Should I be buying LEAPS in this environment?

A: No; a LEAP is a one-year long term deep out-of-the-money call spread. That was a great December bottom trade. The people who bought leaps then made huge fortunes. We’re too high here to consider leaps for the main market unless it's for something that’s just been bombed out, like a Tesla (TSLA) or a Boeing (BA), where you had big drops—then I would look at LEAPS for the super decimated stocks. But the rest of the market is still too high for thinking about leaps. Wait a couple of months and we may get back to those December lows.

Q: What happened to your May 10th bear market call?

A: Actually, it’s kind of looking good. It’s looking in fact like the market topped on May 2nd. If saner heads prevail, the trade war will end (or at least we’ll get a fake agreement) and the market will go to a new high. If not, then that May 10th target forecast I made two years ago IS the final top.

Q: You’re saying today we’re at a bottom?

A: We’re at a bottom for a short-term trade with a June 21st target. That was the expiration date of the options spreads I did this week. Whether this is the final bottom in the whole down move for a longer term, no one has any idea, even if they try to say differently. This is totally dependent on political developments.

Q: What do you have to say about Lockheed Martin (LMT)?

A: This sector usually does well with a wartime background. Expect that to continue for the foreseeable future. But at a certain point, the defense stocks which have had fantastic runs under Trump will start to discount a democratic win in the next election. If that does happen, defense will get slaughtered. I would be using any future strength to sell out of the whole defense area. Peace could be fatal to this sector.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/unit-sales.png591899Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-17 02:04:382019-07-09 03:43:41May 15 Biweekly Strategy Webinar Q&A

With the Dow Average down 1,400 points in six trading days, you are being given a second bite of the apple before the yearend tech-led rally begins.

So, it is with great satisfaction that I am rewriting Arthur Henry’s Mad Hedge Technology Letter’s list of recommendations.

By the way, if you want to subscribe to Arthur’s groundbreaking, cutting edge service, please click here.

It’s the best read on technology investing in the entire market.

You don’t want to catch a falling knife but at the same time, you want to diligently prepare yourself to buy the best discounts of the year.

The China trade war has triggered a tsunami wave of selling, tearing apart the tech sector with vicious profit-taking few trading days.

No doubt that asset managers are frantically locking in profits for the rest of the year and protecting ebullient performance from a first quarter to remember.

This week shouldn’t deter investors from picking up bargains that were non-existent since December because the bulk of the highest quality tech names churned higher with lurching momentum.

Here are the names of five of the best stocks to slip into your portfolio in no particular order once the madness subsides.

Apple

Steve Job’s creation weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software service-tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has its supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $150 billion in shares by the end of 2019. Get into this stock while you can as entry points are few and far between.

Amazon (AMZN)

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart door bell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2018 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data in Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox-related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

Square (SQ)

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer makes me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

The recently departed CFO Sarah Friar triggered a 10% collapse in share price on top of the market meltdown. The weakness will certainly be temporary, especially if they keep doubling their revenue every two years like they have been doing.

Roku (ROKU)

Benefitting from the broad-based migration from cable tv to online streaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Roku’s active accounts mushroomed 46% to 22 million in the second quarter. Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an off-shoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square.

Be patient and wait for 5-7% drops to pick up some shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2019-05-14 03:02:172019-07-09 03:44:00Five Stocks to Buy at the Bottom

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 1 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

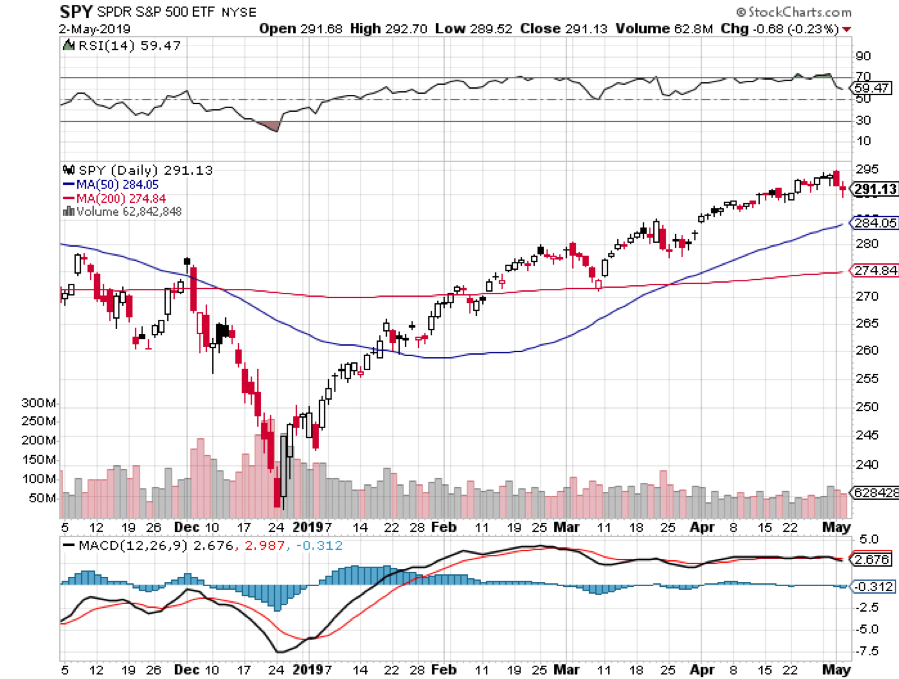

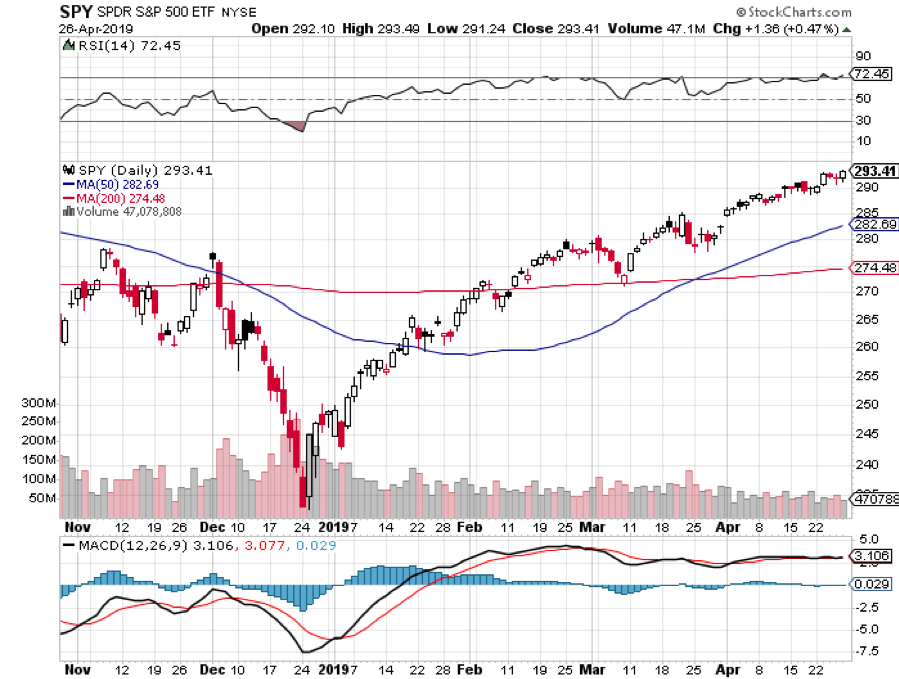

Q: Your old target for the (SPY) was $292.80; we’re clearly above that now. What’s your new target and how long will it take to get there?

A: My new target on the S&P 500 (SPY) is $296.80. You’re looking at $295 on the (SPY), so we’re almost there. However, we’re grinding up too slowly so I can’t give you an exact date.

Q: Will Fed governor Jay Powell give in to pressure from Trump who wants him to drop rates? Does he have any sway over the process?

A: Officially he has no sway, but every day Trump is tweeting: “I want QE back, I want a 1% rate cut.” And if that happened, the economy would completely blow up—an interest rate cut with the market at an all-time high and 3.25% GDP growth rate would be unprecedented, would deliver a short term gain and long term disaster.

Q: What do you think about the Uber (UBER) IPO?

A: I wouldn’t touch it with a 10-foot pole—they’ve been cutting valuations almost every day. At one point they were going to value the company at $120 billion dollars, now they’re at $90 billion and they may even lower it from there. The last car sharing IPO (LYFT) dropped 33% from its high. I would stay away from all of the IPOs once they’re listed. The rule is: only buy these things when they’re down 50%. Warren Buffet never buys IPOs, nor do I.

Q: What do you think about buying or selling Lyft?

A: I would wait a couple of months for Lyft to find its true price. Then you’ll have something to trade against.

Q: Do you think the bad news is over on Tesla (TSLA)? Is it time to buy? Or is it going bankrupt?

A: The whole world knew that the electric car subsidy would be cut in January, so what customers did was accelerate their orders in the 4th quarter, which took us all the way up to $380 in the shares, and then created a vacuum in the Q1 of this year. It reported the first quarter last week—they were disastrous orders, and the company is cutting back overhead as fast as possible as if it’s going into a recession, which it kind of is. The question is whether or not sales will bounce back in Q2 with the smaller subsidy. I happen to think they will. But we may not see 2018 Q4 sales levels again until 2019 Q4.

Q: Why has healthcare (XLV) been so awful this year?

A: There’s an election next year and both parties promise to beat up on the healthcare industry with drug control pricing and other forms of regulation. Of course, the current president promised free competition in drug prices; but then he moved to Washington DC and found the drug industry lobby, and nothing was ever heard again on that front. It’s a very high political risk sector, but there is some great value at these levels in the healthcare industry in the long term. I’m about to start the Mad Hedge Biotech and Health Care newsletter imminently.

Q: Should I buy the (TLT) $120-$123 call spread now?

A: That's a very aggressive trade, I would wait and go with strikes for in the money, and then only on a big dip. Don’t reach for a trade when the market is at an all-time high.

Q: Should I be shorting Tesla down here?

A: Absolutely not, your short trade was at $380, $350, $330 and $300. Down here, you run the risk of a surprise tweet from Elon Musk causing the stock to go $50 against you. Buy the way, he’s already announced that he’s buying $10 million worth of shares in his next capital raise.

Q: What do you think about CRISPR stocks long term, like Editas Medicine (EDIT), Sangamo Life Sciences (SGMO), and Cellectis (CLLS)?

A: These are probably the best bunch of 10 baggers long term. Short term they are afflicted with the same problems impacting all of healthcare—promises of regulation and price control on all of their products ahead of an election. So, hold for the long term; short term I’d only be buying the really big dips. Did I mention that I’m about to start the Mad Hedge Biotech and Health Carenewsletter imminently?

Q: Is your May 10th market top forecast still good?

A: Well we’re getting kind of close to May 10th. I made this prediction based on an inverting yield curve two years ago. However, that target did not anticipate interest rates topping out for the 10-year US Treasury bond at 3.25%. Nor did it consider the Fed canceling all interest rate hikes for the year. Without the artificial stimulus, the market would certainly have already rolled over and died. That said, I still have a week to go.

Q: Should I be selling my long term holds in the FANGS, like Apple (AAPL), Amazon (AMZN), and Microsoft (MSFT)?

A: For the long term, no. However, we know from December that these things can get hit with a 40% drawdown at any time. As long as you can handle that, they always bounce back.

Q: What will happen to Venezuela? Any trades?

A: The only related trades would be in the oil market (USO). If we get a coup d’ etat which installs a new pro-American president, which could be at any time, that could lead to a selloff in oil for a couple of days as 1 Million barrels of crude per day come back on the market, but probably no more than that.

Q: With current national debt and budget deficits, when will interest in gold kick in?

A: Very simple: when the stock market goes down, you want to buy gold. It’s the hedge that everyone will chase after, and inflation is just around the corner.

Q: Do you need me to place any Kentucky Derby bets?

A: Me being the cautious guy I am, I pick the horse with the best odds and then I bet him to show. That almost always works.

Q: What about pot stocks?

A: I’ve never liked them very much; after all, how hard is it to grow a weed? The barriers to entry are zero. All of these pot companies coming up now are not really pot stocks as much as they are marketing companies, so you’re buying their distribution capability primarily. That said, I’m having breakfast with the CEO of a major pot company next week, so I’ll be writing about that once I get the inside scoop.

Q: Will the Fed be the non-event?

A: Yes, as stated in the Mad Hedge Hot Tips this morning, it will be a non-event and the news is due out in about an hour.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas-bear.png402291Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-03 03:06:422019-05-03 13:56:12May 1 Biweekly Strategy Webinar Q&A

To the dozens of subscribers in Afghanistan, Somalia, Iraq, Syria, and the surrounding ships at sea, thank you for your service!

I think it is very wise to use your free time to read my letter and learn about financial markets in preparation for an entry into the financial services when you muster out.

And if Donald Trump gets his way with a 10% rise in defense spending and a 30% cut in the State Department budget, it looks like there are going to be a lot more of you abroad to take advantage of my services.

Nobody is going to call you a baby killer and shun you, as they did when I returned from Southeast Asia four decades ago. In fact, employers have been given fantastic tax breaks and other incentives to hire you.

I have but one request. No more subscriptions with .mil addresses, please. The Defense Department, the CIA, the NSA, Homeland Security, and the FBI do not look kindly on private newsletters entering the military network, even the investment kind.

If you think civilian spam filters are tough, watch out for the military kind! And no, I promise that there are no secret messages embedded with the stock tips. “BUY” really does mean “BUY.” “Sell” means “Sell” too.

If I did not know the higher ups at these agencies, as well as the Joints Chiefs of Staff, I might be bouncing off the walls in a cell at Guantanamo by now wearing an orange jumpsuit.

It also helps that many of the mid-level officers at these organizations have made a fortune with their meager government retirement funds following my advice. All I can say is that if the Baghdad Stock Exchange ever become liquid, I'm going to own it.

Where would you guess the greatest concentration of readers The Diary of a Mad Hedge Fund Trader is found? New York? Nope. London? Wrong. Chicago? Not even close.

Try a ten-mile radius centered on Langley, Virginia, by a large margin.

The funny thing is, half of the subscribing names coming in are Russian. I haven't quite figured that one out yet.

Did we hire the entire KGB at the end of the cold war? If we did, it was a great move. Those guys were good. That includes you, Yuri.

So, keep up the good work, and fight the good fight. But please, only subscribe to my letter with personal Gmail, Yahoo, or Hotmail addresses. That way my life can become a lot more boring.

Oh, and by the way, Langley, you're behind on your bill. Please pay up, pronto, and I don't want to hear whining about any damn budget cuts!

I Want My Mad Hedge Fund Trader!

https://www.madhedgefundtrader.com/wp-content/uploads/2017/06/army-cig-e1498672458898.jpg393557MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-05-02 01:06:372019-05-01 15:31:53Notice to Military Subscribers

This is one of those markets where you should have followed your mother’s advice and become a doctor.

I was shocked, amazed, and gobsmacked when the Q1 GDP came in at a red hot 3.2%. The economy had every reason to slow down during the first three months of 2019 with the government shutdown, trade war, and terrible winter. Many estimates were below 1%.

I took solace in the news by doing what I do best: I shot out four Trade Alerts within the hour.

Of course, the stock market knew this already, rising almost every day this year. Both the S&P 500 and the NASDAQ (QQQ) ground up to new all-time highs last week. The Dow Average will be the last to fall.

Did stock really just get another leg up, or this the greatest “Sell the news” of all time. Nevertheless, we have to trade the market we have, not the one we want or expect, so I quickly dove back in with new positions in both my portfolios.

One has to ask the question of how strong the economy really would have been without the above self-induced drags. 4%, 5%, yikes!

However, digging into the numbers, there is far less than meets the eye with the 3.2% figure. Exports accounted for a full 1% of this. That is unlikely to continue with Europe in free fall. A sharp growth in inventories generated another 0.7%, meaning companies making stuff that no one is buying. This is growth that has been pulled forward from future quarters.

Strip out these one-off anomalies and you get a core GDP that is growing at only 1.5%, lower than the previous quarter.

What is driving the recent rally is that corporate earnings are coming in stronger than expected. Back in December, analysts panicked and excessively cut forecasts.

With half of the companies already reporting, it now looks like the quarter will come in a couple of points higher than lower. That may be worth a rally of a few more percentage points higher for a few more weeks, but not much more than that.

So will the Fed raise rates now? A normal Fed certainly would in the face of such a hot GDP number. But nothing is normal anymore. The Fed canceled all four rate hikes for 2019 because the stock market was crashing. Now it’s booming. Does that put autumn rate hikes back on the table, or sooner?

Microsoft (MSFT) knocked it out of the park with great earnings and a massive 47% increase in cloud growth. The stock looks hell-bent to hit $140, and Mad Hedge followers who bought the stock close to $100 are making a killing. (MSFT) is now the third company to join the $1 trillion club.

And it’s not that the economy is without major weak spots. US Existing Home Sales dove in March by 5.9%, to an annualized 5.41 million units. Where is the falling mortgage rate boost here? Keep avoiding the sick man of the US economy. Car sales are also rolling over like the Bismarck, unless they’re electric.

Trump ended all Iran oil export waivers and the oil industry absolutely loved it with Texas tea soaring to new 2019 highs at $67 a barrel. Previously, the administration had been exempting eight major countries from the Iran sanctions. More disruption all the time. The US absolutely DOES NOT need an oil shock right now, unless you’re Exxon (XOM), Chevron (CVX), or Occidental Petroleum (OXY).

NASDAQ hit a new all-time high. Unfortunately, it’s all short covering and company share buybacks with no new money actually entering the market. How high is high? Tech would have to quadruple from here to hit the 2000 Dotcom Bubble top in valuation terms.

Tesla lost $700 million in Q1, and the stock collapsed to a new two-year low. It’s all because the EV subsidy dropped by half since January. Look for a profit rebound in quarters two and three. Capital raise anyone? Tesla junk bonds now yielding 8.51% if you’re looking for an income play. After a very long wait, a decent entry point is finally opening up on the long side.

The Mad Hedge Fund Trader blasted through to a new all-time high, up 16.02% year to date, as we took profits on the last of our technology long positions. I then added new long positions in (DIS), (FCX), and (INTU) on the hot GDP print, but only on a three-week view.

I had cut both Global Trading Dispatch and the Mad Hedge Technology Letter services down to 100% cash positions and waited for markets to tell us what to do next. And so they did.

I dove in with an extremely rare and opportunistic long in the bond market (TLT) and grabbed a quickie 14.61% profit on only three days.

April is now positive +0.60%. My 2019 year to date return gained to +16.02%, boosting my trailing one-year to +21.17%.

My nine and a half year shot up to +316.16%.The average annualized return appreciated to +33.87%. I am now 80% in cash with Global Trading Dispatch and 90% cash in the Mad Hedge Tech Letter.

The coming week will see another jobs trifecta.

On Monday, April 29 at 10:00 AM, we get March Consumer Spending. Alphabet (GOOGL) and Western Digital (WDC) report.

On Tuesday, April 30, 10:00 AM EST, we obtain a new Case Shiller CoreLogic National Home Price Index. Apple (AAPL), MacDonald’s (MCD), and General Electric (GE) report.

On Wednesday, May 1 at 2:00 PM, we get an FOMC statement.

QUALCOMM (QCOM) and Square (SQ) report. The ADP Private Employment Report is released at 8:15 AM.

On Thursday, May 2 at 8:30 AM, the Weekly Jobless Claims are produced. Gilead Sciences (GILD) and Dow Chemical (DOW) report.

On Friday, May 3 at 8:30 AM, we get the April Nonfarm Payroll Report. Adidas reports, and Berkshire Hathaway (BRK/A) reports on Saturday.

As for me, to show you how low my life has sunk, I spent my only free time this weekend watching Avengers: Endgame. It has already become the top movie opening in history which is why I sent out another Trade Alert last week to buy Walt Disney (DIS).

I supposed that now we have all become the dumb extension to our computers, the only entertainment we should expect is computer-generated graphics with only human voice-overs.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/avengers.png272485Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-29 01:06:452019-07-09 03:53:45The Market Outlook for the Week Ahead, or Another Leg Up for the Market

Let me warn you in advance that I am only going off drugs long enough to write this newsletter.

This year’s flu has finally laid me low and let me tell you it is a real killer. Perhaps it is my advanced age that has magnified its effects. Then I developed an allergic reaction to the flu medicine I was taking. For a couple of days there, I was looking like the Michelin Man.

However, I did have a lot of time to read research. And what I learned was sobering.

For a start, we are fully back to a quantitative easing market. In one fell swoop, the Fed went from an expectation of four interest rate hikes in 2019 to none. By ending quantitative tightening early, it has cut the amount of cash it is withdrawing from the financial system from $4.3 trillion to only $1.5 trillion.

The Fed is in effect reflating the bubble one more time. And what do you do in a QE-driven economy. YOUBUY EVERYTHING! This explains why stocks, bonds, commodities, and energy have all been marching upward in unison this year even though that is supposed to be theoretically impossible.

Yes, the decade long liquidity-driven bull market may have another leg up to go.

A higher high inevitably leads to a lower low. The trades you are executing now may be akin to picking up pennies in front of a steam roller. We are clearly planting the seeds of the next financial crisis. But for now, the pain trade is clearly to the upside.

Those of who who traded through the dotcom bubble are seeing déjà vu all over again. Huge money-losing tech companies are now floating IPOs on a daily basis. This too will end in tears, which is why I have recommended to followers to avoid all of them. This is a sucker’s game.

There is a cloud behind this silver lining. After a ballistic 21.43% move in the Dow Average in four months, markets are trading as if risk is a thing of the past. The euphoria is here and complacency rules. That means the number of new possible low risk/high return trades out there has fallen to zero.

There is another cloud to worry about. The more excess stimulus the Fed provides the economy now, the fewer resources it will have to get us out of the next recession, which might be only a year off. As a result, everyone is long but extremely nervous. They are still participating in the party but are standing next to the exit door. Pent up volatility is building like a volcano ready to explode.

The other great revelation is that markets have been trading extremely short term in nature, only one quarter ahead of what the real economy is doing. So, a stock market meltdown in Q4 2018 discounted a collapsing GDP growth in Q1 2019 of a 1% rate or less. That is down 80% from a year ago peak.

The ultra-strong market in Q1 is anticipating an economic rebound in Q2, After that, who knows?

That’s why I am moving both of my trading portfolios for Global Trading Dispatch and the Mad Hedge Technology Letter to 100% cash positions in the coming week.

Last week was the week when Walt Disney (DIS) morphed from being a has-been media stock hobbled by a failing holding in ESPN to a dynamic company that is suddenly taking over the world. The reward was an eye-popping 25% move in three weeks, which we caught.

Copper demand is rocketing, off of soaring global electric car production. Each vehicle needs 22 pounds of the red metal, and 4 million have been built so far. That number reached 5 million by June. Take a second bite of the apple with (FCX) as well.

General Electric got slaughtered again, with an earnings downgrade from Morgan Stanley. It will take years to sort out this mess. Avoid (GE).

The 30-year fixed rate mortgage plunged to 4.03% and may save the spring selling season for residential real estate.

Apple Topped $200. It looks like the market is finally buying the services story. Stand aside for the short term. It’s had a great run, up 42% from the December low. I’m waiting for 5G until I buy my next iPhone, probably next year.

The Mad Hedge Fund Trader hit a new all-time high briefly, up 15.46% year to date, and beating the pants off the Dow Average. Good thing I didn’t buy the bearish argument. There’s too much cash floating around the world. However, my downside hedges in Disney and Tesla cost me some money when I stopped out. I was late by a day.

We are taking profits on a six-month peak of 13 positions across the GTD and Tech Letter services and will wait for markets to tell us what to do next.

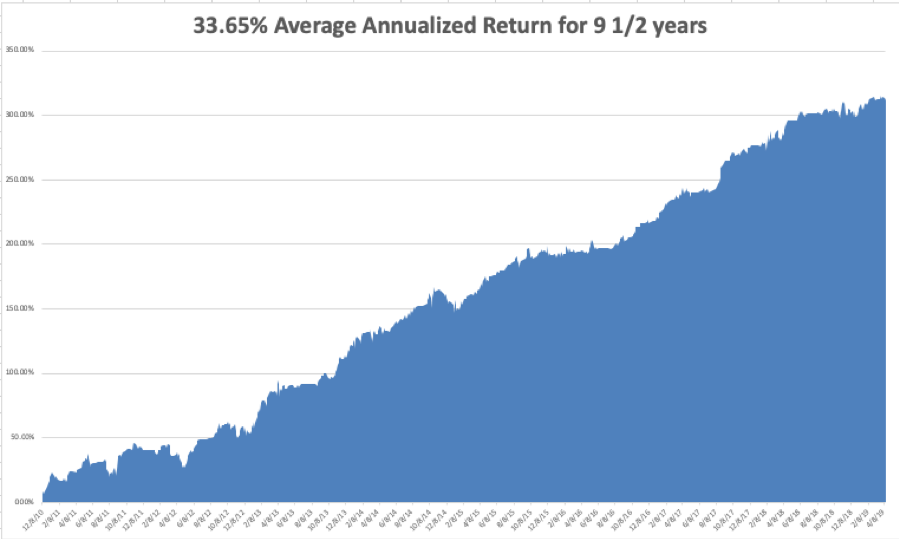

April is so far down -1.50%, as my downside hedges in Tesla (TSLA) and Disney (DIS) cost me some sofa change. My 2019 year to date return retreated to +13.92%, paring my trailing one-year return back up to +27.22%.

My nine and a half year return backed off to +314.06%.The average annualized return appreciated to +33.65%. I am now 100% in cash.

The Mad Hedge Technology Letter has gone ballistic, with an aggressive and unhedged 30% long which expires this week. It is maintaining positions in Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN), which are clearly going to new highs.

It’s going to be a dull week on the data front after last week’s fireworks.

On Monday, April 15 at 8:30 AM, we get the April Empire State Index. Citibank (C) and Goldman Sachs (GS) report.

On Tuesday, April 16, 9:15 AM EST, we learn March Industrial Production. Netflix (NFLX) and IBM (IBM) report.

On Wednesday, April 17 at 2:00 PM, we get the Fed Beige Book Indicators. Morgan Stanley reports (MS).

On Thursday, April 18 at 8:30 the Weekly Jobless Claims are produced. At 10:00 AM EST, we obtain the March Index of Leading Economic Indicators. American Express (AXP) reports.

On Friday, April 19 at 8:30 AM, the markets are closed for Good Friday.

As for me, I am staying planted in my bed reading up on research and watching HBO until I kick this flu. After that, I should be good for the rest of the year.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Flat on my Back

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/john-thomas-3.png391522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-15 08:06:302019-07-09 03:54:45The Market Outlook for the Week Ahead, or QE is Back!

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.