Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

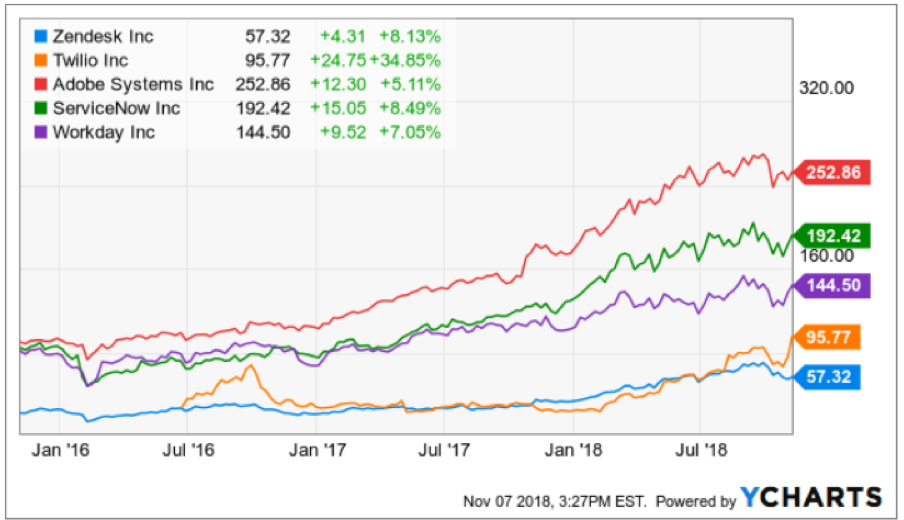

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

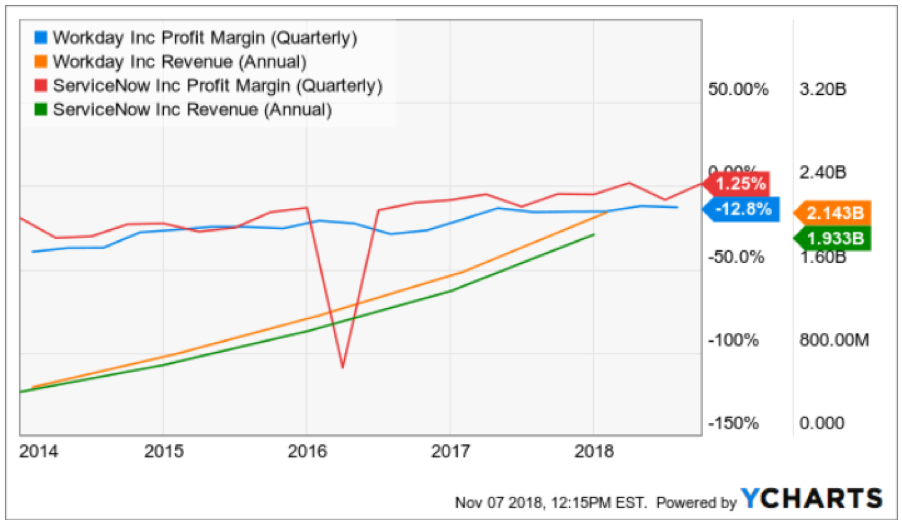

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.

Mad Hedge Technology Letter

September 6, 2018

Fiat Lux

Featured Trade:

(THE SMART PLAYS IN FINTECH),

(SQ), (PYPL), (JPM), (COF), (WFC), (BAC),

(MGI), (GRUB), (BABA), (NFLX)

Fintech is all the rage now, and it’s time for investors to grab a piece of the action.

The tech sectors’ stellar performance in 2018 is a little taste of things to come as every industry forcibly pushes toward software and artificial intelligence to enhance products and services.

Bull markets don’t die of old age and some of these tech stalwarts are truly defying gravity.

The fintech sector is no exception.

Square (SQ) led by tech visionary Jack Dorsey has been a favorite of the Mad Hedge Technology Letter practically from the newsletter’s inception.

But another company has caught my eye that most of you already know about – PayPal (PYPL).

PayPal, a digital payments company, has extraordinary core drivers and a splendid growth trajectory.

Its arsenal of services includes digital wallets, money transfers, P2P payments, and credit cards.

It also has Venmo.

Venmo, a digital payment app, is the strongest growth lever in PayPal’s umbrella of assets right now, and was the first meaningful digital payment app in America.

It was established by Andrew Kortina and Iqram Magdon-Ismail, who were roommates at the University of Pennsylvania, and the company was bought out by PayPal for $800 million in 2014, marking a new chapter in PayPal’s evolution.

Funny enough, Venmo’s original use was to buy mp3 formatted songs via email in 2009.

Venmo is wildly popular with tech savvy millennials. A brief survey conducted illustrates how fashionable Venmo is by recording higher user statistics than Apple Pay.

The app is commonly used for ordering pizza through Uber Eats or Grubhub (GRUB), or even shelling out for monthly rent.

If you want to stir up your imagination even more, Venmo has a prominent social feed where users can view other Venmo users’ purchases.

Financial models suggest Venmo could contribute $300 million to the PayPal top line in 2021. If Venmo executes perfectly, revenue could surpass the $1 billion mark in 2021, with much higher operating margins than PayPal’s core products.

Even though management declines to speak specifically about Venmo, the dialogue in the earnings call usually provides some color into what is going on underneath the hood.

Xoom, a digital remittance distributor app with offices in San Francisco and Guatemala City owned by PayPal, along with Venmo grew payment volume by 50% YOY, surging to $33 billion annually.

Of that $33 billion in volume, $19 billion was contributed by Venmo and Xoom chipped in with $14 billion.

More than 60,000 new merchants joined PayPal’s array of platforms, adding up to more than 19.5 million total merchants.

All in all, PayPal locked in $3.86 billion of sales last quarter, which was a 23% YOY jump in revenue, at a time where widespread acceptance of fintech platforms is brisk.

PayPal raised its end-of-year forecast and rewarded shareholders with authorization of a $10 billion buyback.

Upward margin expansion, expanding market share, multiple revenue stream, and untapped pricing power is the recipe to PayPal’s meteoric rise.

PayPal’s share price has climbed higher from a base of $73 at the beginning of the year to an all-time high of more than $90.

Offering more proof fintech is alive and kicking is Jack Dorsey’s Square’s dizzying rise of more than 200% YOY in its share price.

The company is exceeding all revenue growth expectations and is poised to ramp up subscription revenue.

As with the Venmo app, Square’s Cash app has unrealized potential and will be one of the outperforming profit drivers going forward.

Square hopes to be the one-stop-shop for all types of digital payment needs including consumer finance, equity purchases, possibly international transfers, and cryptocurrency.

All of this is happening amid a robust secular story that could have seen traditional banks swept into the dustbin of history.

Rewind a few years ago, perusing the data about the movement to digital payments must have frightened the living daylights out of the executives from major Wall Street mainstays.

Digital wallets assertive migration into mainstream money payment services could have detached traditional banks’ core businesses.

Slogging your way to a physical bank to put in a wire transfer was not appealing.

Archaic methods of business are painful to see, and traditional banks were still operating this way as of 2015.

Time is money and technology has crashed the traditional waiting time to almost zero.

The way these tech companies operate is simple.

They compete to hire a hoard of advanced computer developers or shortcut the process using the time-honored tradition of poaching the competition’s best talent.

Then snatch market share at all costs and grow like crazy.

Banks badly needed introducing some functions to their array of services such as linking with third-party payment APIs to facilitate online payments and enabling cross-platform digital payments.

Other functions such as establishing modern peer-to-peer payment systems or adopting QR code technology that are wildly popular in East Asia could enhance optionality as well.

These are several instruments they could have amalgamated into their arsenal of fintech technology that could have freshened up these dinosaur institutions.

Harmonizing banking tasks with mobile functionality was fast coming and would be the standard.

Anyone not on board would sink like the Titanic.

Ultimately, banking institutions needed to up their game and acquire one of these digital wallet processors or watch from the sidelines.

They chose the former when a consortium called Early Warning Services (EWS) jointly created by behemoth American banks, including JPMorgan Chase & Co. (JPM), Capital One (COF), Bank of America (BAC), and Wells Fargo (WFC) to “prevent fraud and reduce detection risk” made a game-changing decision.

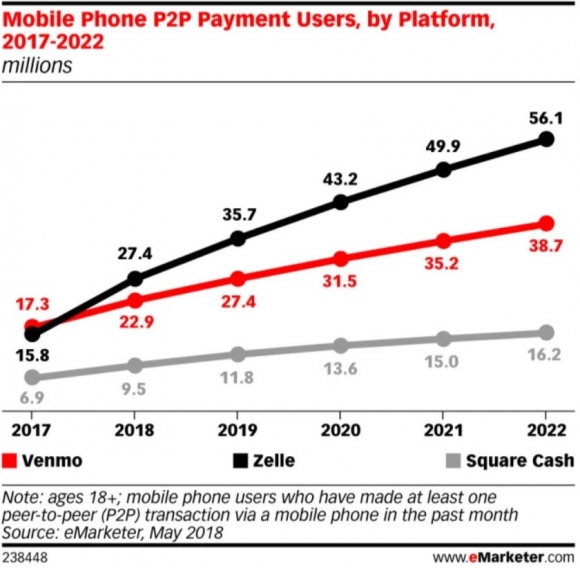

(EWS) acquired digital payment app Zelle in 2016, and this was its aggressive response to Square Cash and PayPal’s Venmo.

Results have been nothing short of breathtaking.

Leveraging the embedded base of existing banking relationships, Zelle took off like a scalded chimp and never looked back.

In a blink of an eye, Zelle had already signed up more than 30 banks and over 100 financial institutions to its platform.

Banks couldn’t bear being left out of the fintech party.

With hearty conviction, Zelle is signing up users at a pace of 100,000 per day, and the volume of payments in 2017 eclipsed $75 billion.

Zelle projects to expand more than 73% in 2018, integrating 27.4 million new accounts in the U.S., head and shoulders above Venmo’s 22.9 million and Square Cash due to add 9.5 million more users.

Make no bones about it, Zelle was in prime position to convert existing relationships into digital converts. The banks that do not have an interest in Zelle have an uphill climb to stay relevant.

The United States is rather late to this secular growth story. That being said, already 57% of Americans have used a mobile wallet at least once in their lives.

Innovative ideas bring supporters galore and even more adoptees.

That is why the strong pivot into technological enhanced ideas bear unlimited fruit.

Using a mobile platform to just open an app then send funds within a split second with minimal costs is appealing for the Netflix (NFLX) crazed generation that can hardly get off the couch.

Ironically, it’s those in the emerging parts of the world leading this fintech revolution by skipping the traditional banking experience completely and downloading digital wallet apps on their mobile devices.

It’s entirely realistic that some fresh-faced youth have never been present at a physical banking branch before in India or China.

Download an app and your fiscal life commences. Period.

The volume of funds passing through the arteries of Chinese digital wallet apps surpassed $15 trillion in 2017.

And by 2021, 79.3% of the Chinese population are projected to use digital wallets as their main source of splurging Chinese yuan.

America lags a country mile behind China, but the Chinese progress has offered American tech companies a crystal-clear blueprint to springboard digital payment initiatives.

Chinese state banks are already starting to become marginalized, and the Wall Street banks are not immune to the same fate.

Devoid of a digital strategy will be a death knell to certain banking institutions.

Compare the pace of adoption and some must question why American adoption is tardy to a fault.

Highlighting the lackadaisical pace of American fintech integration was Alibaba’s (BABA) smash-and-grab attempt at MoneyGram International Inc. (MGI), as it sought to gain a foothold into the American fintech market.

The attempt was rebuffed by the federal government.

The nascent state of the digital payment world in America must alarm Silicon Valley experts. And the run-up in Square and PayPal includes calculated bets that these two standouts will leapfrog into the future with guns blazing along with Zelle.

The parabolic nature of Square’s mystifying gap up means that a moderate pullback is warranted to put capital to work in this name.

Investors should wait for a timely entry point into PayPal as well.

These two stocks have overextended themselves.

As the fintech pie extrapolates, there will be multiple victors, and these victors are already taking shape in the form of Zelle, PayPal, and Square.

![]()

________________________________________________________________________________________________

Quote of the Day

“In the not-too-distant future, commerce is just going to be commerce. It won't be online commerce or offline commerce. It's just going to be commerce. And that will happen because of the phone,” – said CEO of PayPal Dan Schulman.

Global Market Comments

June 8, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE TUESDAY, JUNE 12, 2018,

NEW ORLEANS, LA, GLOBAL STRATEGY LUNCHEON),

(JUNE 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (TTT), (TBT), (AMLP), (IBB),

(SPY), (SDS), (SH), (GS), (BAC)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader June 6 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: What does the coming Kim Jong-un summit with North Korea mean for the market?

A: It means absolutely nothing for the market. The entire North Korean threat has been wildly exaggerated as a distraction from the chaos in Washington. So, you may get a one- or two-day rally if it's successful. If it's not expect a one- or two-day sell-off, but no more. Whatever North Korea agrees to, we will not see any follow through; they won't buy the Libyan model of denuclearizing North Korea for fear of their leader meeting the same end as Libya's Khadafy (i.e. being hunted and shot in a storm drain.) North Korea will never give up its nuclear weapons.

Q: What do you do at market tops?

A: Well, hopefully if you're reading this letter you're long up the wazoo, so you sell everything you have. Then, wait for a double top in the market (which is clear as day) and falling volume. You start looking at things like the ProShares Ultra Short S&P 500 ETF (SDS). That's the -2X version (there's the (SH), which is the -1X short S&P 500) and you just start buying outright puts on a lot of different things, particularly the overbought sectors of the market, which are generally pretty obvious. It's also good to look for a stock that has made a new high and has negative money flow.

Q: Why are the banks doing so poorly?

A: I believe they fully discounted all of this year's interest rate hikes last year when the stocks nearly doubled. We just talked about a technical setup; Goldman Sachs (GS), Bank of America (BAC), and other stocks had those bear setups. At this point, I believe they're coming down to a place of support and probably getting a decent dead cat bounce. They've had their sell-off, they had their run, and it was triggered by one of the best technical short setup patterns you'll see.

Q: Would you buy financials here?

A: Absolutely not. It's unclear why they're doing so badly, but I would not buy it with anyone's money. Their earnings growth is nowhere what you see with technology stocks.

Q: Is crude oil poised for the next leg up?

A: No, it's not. The oil game may be over if they rush to overproduce once again. It's clearly been artificially boosted to get the Saudi Aramco IPO done. After the end of the quota system, you can get oil back down to the $50s easily. I don't want to touch it here; if anything, I'm more inclined to buy it if we get down to the $50s, which would essentially be the February low.

Q: Is the U.S. dollar overbought here?

A: Yes. The dollar has had a great run all year, which is evident from the rising interest rates. It's done a 10% move up in a fairly short time, which is a lot for the foreign exchange market. It's way overbought; you could easily get a round of profit taking in the dollar, either going into or right after the next Fed interest rate hike in two weeks. I'm staying away from the currencies. There are too many better fish to fry in the equities.

Q: Can you expect Tech to keep going up after this next run?

A: Yes, I expect us to break out to a new high and give back some ground in a retest of the old high. The old high will then hold and then I expect a sort of slow grind up. Tech could well go up for the rest of 2018.

Q: If the S&P 500 is in a trading range, would you sell any rally?

A: Yes, but I'm going to wait for the rally to come to me; I'm not going to reach for any marginal trades. When the (SPY) gets to $280, I'll be looking very closely at the $285-$290 vertical bear put spread one or two months out. So, that peak should hold for the summer and you can make a good 25%-30% on that kind of spread.

Q: Would you buy Biotech here?

A: Yes, the chart setup here is looking very positive, and it's natural for people to rotate out of Tech to Biotech because the earnings growth is so dramatic. That's why I sent out a Trade Alert to buy the NASDAQ Biotechnology ETF (IBB) yesterday. They have been unfairly held back by fears of drug pricing regulation, which has nothing to do with biotech, but it affects their share prices anyway. But so far, it has been all talk from Trump and no action. I think he's busy with North Korea and the trade wars anyway.

Q: My custodian won't let me sell short the United States Treasury Bond Fund (TLT) so I bought the ProShares Ultra Pro Short 20+ Treasury Fund (TTT). Is that alright?

A: You definitely want to be short the Treasury bonds market for the next several years going forward, so you have the right idea. If the 10-year U.S. Treasury bond yield jumps from 2.95% today to 4% in a year as I expect, that takes the (TLT) down from $119 to $97. If you can't make money shorting bonds in that environment you should consider another line of work.

The problem with these 3X leveraged funds is that the cost of carry is very high. In the case of the (TTT) it is three times the 3.0% 10-year bond coupon you are shorting plus a 1% management fee for a total of 10% a year. For that reason, the 3X funds are really only good for day trading. You run into a similar problem with the 2X (TBT). This is why I use non-leveraged put spreads or outright puts for this asset class.

Q: Why are we seeing strength in the Alerian master limited partnership (AMLP) when oil prices are falling, and interest rates are rising? Shouldn't it be going the other way?

A: How about more buyers than sellers? There are so many retirees out there desperate for yield they will take on inordinate amounts of risk to get it. With an 8.0% dividend yield you always have an underlying bid for this ETF. That's why we have been recommending this since April. An 8% dividend can cover up a lot of sins, even when interest rates are rising and oil prices are falling. Also, the U.S. is infrastructure constrained now that production is approaching 11 million barrels a day. That is great for the kind of energy projects (AMLP) finances.

Q: What's the next support price for NVIDIA (NVDA)?

A: With the stock going straight up there is little need for support. Our 2018 target is $300. If you recall, we have been recommending this cutting-edge GPU manufacturer since $68, and people have made fortunes. Those who bought long dated deep out-of-the-money leaps $100 out made 1,000% on this Trade Alert 18 months ago. That said, the 200-day moving average at $213 looks rock solid.

Good luck and good trading to all.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Sometime in the early 1970?s, a friend of mine said I should take a look at a stock named Berkshire Hathaway (BRKA) run by a young stud named Warren Buffett.

I thought, ?Why the hell should I invest in a company that makes sheets??

After all, the American textile industry was in the middle of a long trek toward extinction that began in the 1920?s, and was only briefly interrupted by the hyper prosperity of WWII. The industry?s travails were simply an outcome of ever rising US standards of living, which pushed wages, and therefore costs, up.

It turns out that Warren Buffett made a lot more than sheets. However, he is not a young stud anymore, just an old one, like me.

Since then, Warren?s annual letter to investors has been an absolute ?must read? for me when it is published every spring.

It has been edited for the past half century by my friend, Carol Loomis, who just retired after a 60-year career with Fortune magazine. (I never wrote for them because their freelance rates were lousy).

Witty, insightful, and downright funny, I view it as a cross between a Harvard Business School seminar and a Berkeley anti establishment demonstration. You will find me lifting from it my ?Quotes of the Day? for the daily newsletter over the next several issues. There are some real zingers.

And what a year it has been!

Berkshire?s gain in net worth was $18.3 billion, which increased the share value by 8.3%, and today, the market capitalization stands at an impressive $343.4 billion. (Sorry Warren, but I clocked 30% last year, eat your heart out).

The shares are not for small timers, as one now costs $214,801, and no, they don?t sell half shares. This compares to a 1965 per share market value of $23.80, and is why the media are always going gaga over Warren Buffett.

If you?re lazy and don?t want to do the math, that works out to a compound annualized return of an eye popping 21.6%. This is why guessing what Warren is going to do next has become a major cottage industry (Progressive Insurance anyone?).

Warren brought in these numbers despite the fact that its largest non-insurance subsidiary, the old Burlington Northern Santa Fe Railroad (BNSF) suffered an awful year.

Extensive upgrades under construction and terrible winter weather disrupted service, causing the railroad to lose market share to rival Union Pacific (UNP).

I was kind of pissed when Warren bought BNSF in 2009 for a blockbuster $44 billion, as it was long my favorite trading vehicles for the sector. Since then, its book value has doubled. Typical Warren.

Buffett plans to fix the railroad?s current problems with $6 billion in new capital investment this year, one of the largest single capital investments in American history. Warren isn?t doing anything small these days.

Buffett also got a hickey from his investment in UK supermarket chain Tesco, which ran up a $444 million loss for Berkshire in 2014. Warren admits he was too slow in getting out of the shares, a rare move for the Oracle of Omaha, who rarely sells anything (which avoids capital gains taxes).

Warren increased his investment in all of his ?Big Four? holdings, American Express (AXP), Coca-Cola (KO), IBM (IBM), and Wells Fargo (WFC).

In addition, Berkshire owns options on Bank of America (BAC) stock, which have a current exercise value of $12.5 billion (purchased the day after the Mad Hedge Fund Trader issued a Trade Alert on said stock for an instant 300% gain on the options).

The secret to understanding Buffett picks over the years is that cash flow is king.

This means that he has never participated in the many technology booms over the decades, or fads of any other description, for that matter.

He says this is because he will never buy a business he doesn?t intrinsically understand, and they didn?t offer computer programming as an elective in high school during the Great Depression.

No doubt this has lowered his potential returns, but with the benefit of much lower volatility.

That makes his position in (IBM) a bit of a mystery, the worst performing Dow stock of the past two years. I would much rather own Apple (AAPL) myself, which also boasts great cash flow, and even a dividend these days (with a 1.50% yield).

Warren will be the first to admit that even he makes mistakes, sometimes, disastrous ones. He cites his worst one ever as a perfect example, his purchase of Dexter Shoes for $433 million in 1993. This was right before China entered the shoe business as a major competitor.

Not only did the company quickly go under, he exponentially compounded the error through buying the firm with an exchange of Berkshire Hathaway stock, which is now worth a staggering $5.7 billion.

Ouch, and ouch again!

Warren has also been mostly missing in action on the international front, believing that the mother load of investment opportunities runs through the US, and that its best days lie ahead. I believe the same.

Still, he has dipped his toe in foreign waters from time to time, and I was sometimes quick to jump on his coattails. A favorite of mine was his purchase of 10% of Chinese electric car factory BYD (BYDDF) in 2009, where I have captured a few doubles over the years.

Buffett expounds at great length the attractions of the insurance industry, which today remains the core of his business. For payment of a premium up front, the buyers of insurance policies receive a mere promise to perform in the future, sometimes as much as a half century off.

In the meantime, Warren can invest the money any way he wants. The model has been a real printing press for Buffett since he took over his first insurer in 1951, GEICO.

Much of the letter promotes the upcoming shareholders annual meeting, known as the ?Woodstock of Capitalism?.

There, the conglomerate?s many products will be for sale, including, Justin Boots (I have a pair), the gecko from GEICO (which insures my Tesla S-1), and See?s Candies (a Christmas addiction, love the peanut brittle!).

There, visitors can try their hand at Ping-Pong against Ariel Hsing, a 2012 American Olympic Team member, after Bill Gates and Buffett wear her down first.

They can try their hand against a national bridge champion (don?t play for money). And then there is the newspaper-throwing contest (Buffett?s first gainful employment).

Some 40,000 descend on remote Omaha for the firm?s annual event. All flights to the city are booked well in advance, with fares up to triple normal rates.

Hotels sell out too, and many now charge three-day minimums (after Warren, what is there to do in Omaha for two more days other than to visit PayPal?s technical support?). Buffett recommends Airbnb as a low budget option (for the single shareholders?).

I was amazed to learn that Berkshire files a wrist breaking 24,100-page Federal tax return (and I thought mine was bad!). Add to this a mind numbing 3,400 separate state tax returns.

Overall, Berkshire holdings account for more than 3% of the total US gross domestic product, but a far lesser share of the government?s total tax revenues, thanks to careful planning.

Buffett ends his letter by advertising for new acquisitions and listing his criteria. They include:

(1) ?Large purchases (at least $75 million of pre-tax earnings unless the business will fit into one of our existing units),

(2) ?Demonstrated consistent earning power (future projections are of no interest to us, nor are ?turnaround? situations),

(3) ?Businesses earning good returns on equity while employing little or no debt,

(4) Managemen

t in place (we can?t supply it),

(5) Simple businesses (if there?s lots of technology, we won?t understand it),

(6) An offering price (we don?t want to waste our time or that of the seller by talking, even preliminarily, about a transaction when price is unknown).

Let me know if you have any offers.

To read the entire history of Warren Buffett?s prescient letters, please click here: http://www.berkshirehathaway.com/letters/letters.htm.

There is no better sight to a hungry trader than blood in the water.

?Buy them when they?re cryin? is an excellent investment strategy that always seems to work.

There are rivers of tears being shed over the banking industry right now.

Federal Reserve officials openly told investors that after the December ?% rate hike that they would continue to do so on a quarterly basis. Only weeks later, a collapse in the stock market shattered this scenario to smithereens.

I doubt we?ll see any more Fed action in 2016.

This caught investors in bank shares wrong footed in a major way.

But wait! It gets worse!

Among the largest holders of American bank shares are the Persian Gulf sovereign wealth funds, including those for Saudi Arabia, Kuwait, Oman, Qatar, and the United Arab Emirates, my old stomping grounds. Pieces of me are still there.

The collapse in oil prices (USO) has put their budgets in tatters and they now have to sell stock to fund wildly generous social service programs. The farther Texas tea drops, the more shares they have to sell, and at $26 a barrel they have to sell bucket loads.

Had enough? There?s more.

The junk bond market (JNK) and oil company shares are suggesting that up to half of all American oil companies will go bankrupt sometime this year, mostly small ones. It all depends on how long oil stays under $40.

Unfortunately, the oil industry has been the most prolific borrower from banks for the last decade. The covenants on many of these loans require borrowers to pump and sell oil to meet interest payments NO MATTER THE PRICE! It?s a perfect formula for maxing out production and selling into a hole.

So fear of widespread energy defaults has also been dragging down bank shares as well.

Some of the moves so far in this short year have been absolutely eye popping. Bank of America (BAC) has plunged 31% from its recent high, while Citibank (C) is down 32% and JP Morgan is off 19%. Basically, they all had a terrible year just in the month of January.

Bank shares have been beaten so mercilessly that they are approaching levels last seen at the nadir of the 2009 financial crisis.

Except that this time, there is no financial crisis, not even the hint of one. For the past seven years, banks have been relentlessly raising capital, reducing leverage, and growing BIGGER.

They proved last time that they were too big to fail. Now they are REALLY too big to fail. Default rates aren?t even a fraction of what we saw during the bad old days. Energy industry borrowing is only a tenth the size of bank home loan portfolios going into the crisis.

Blame the Dodd-Frank financial regulation bill, which requires banks to hold far more capital In US Treasury bonds (TLT) than in the past, which by the way, are doing spectacularly well.

Blame ultra cautious management.

Whatever the reason, Big US banks are now solid as the Rock of Gibraltar.

Which means I?m starting to get interested. Interest rates don?t go down forever, nor does the price of oil. And scares about loan defaults are being wildly exaggerated by the media, as always.

But there is more than one way to skin a cat.

All of these companies issue high yield preferred stock with exceptionally high dividends. For example, Bank of America issued 6.2% yielding paper as recently as October. It is paying something like 8% now.

Since these securities are stock, you get to participate in price appreciation when the panic subsides. A guaranteed 8% return, plus the prospect of substantial capital appreciation? Sounds like a pretty good deal to me.

Google bank preferred shares and you will find an entire world out there of specialist advisors, dedicated newsletters and even day trading and hedging recommendations.

One thing to keep in mind here is that you should only buy ?non callable? paper. This prevents issuers from stealing your paper when better times return to cut their interest payouts.

There is another way to play this beleaguered sector.

You can buy the iShares S&P US Preferred Stock Index Fund ETF (PFF), which owns a basket of preferred stocks almost entirely made up of bank shares. As of today it was yielding 5.62%. To visit the fund?s website, please click link: https://www.ishares.com/us/products/239826/ishares-us-preferred-stock-etf.

Time to BUY?

Time to BUY?In view of the blockbuster October nonfarm payroll report, and the collapse of the bond market that followed, it is time to take a cold, steely eyed look, and the financials, especially Bank of America (BAC).

What did the stock do? It rocketed by 6.5%, along with the rest of the market, hitting four month high of $18.09. I hate it when that happens, being right on the fundamentals, and wrong on the market timing.

You are getting the reaction that the bang up Q3 earnings report should have delivered, just one week late. The shares appear to be taking a run at a new multi year high.

It was a stellar report, with earnings beating expectations handily on both the top and the bottom lines. Expenses are in free-fall, and the company?s cost of funds is plummeting, as lower cost deposit surge.

Analysts were blown away when they saw after tax profits come in at $4.5 billion, producing a diluted earnings per share of $0.37. The company returned a staggering $3 billion to shareholders in the form of dividends and an aggressive share buy back program.

Every major business segment showed big year on year improvements, including consumer and business banking. Global wealth and investment management knocked the cover off the ball.

The sudden burst of market volatility gave a nice push in income to the global banking division.

Deposits from mobile banking jumped. Average deposits are up 4%. Subterranean interest rates kept income there flat.

Given the bank?s tremendous upside leverage, many analysts are now pegging the stock with a $30 handle.

There is another play here. (BAC) is highly geared to raising interest rates, which will enable them to lend money out at higher interest rates, increasing their spread. Think of it as long dated put option on the iShares Barclays 20+ Treasury Bond ETF (TLT).

That is not a bad position to have on board, given that we probably put in a multigenerational spike in bond prices last week.

Because of the bank?s long and well-publicized problems with regulators dating back to before the 2008 financial crisis, (BAC) became toxic waste for many portfolio mangers.

The end result of that has been to make the best-run banks in the industry also the cheapest.

I have a feeling that I will be visiting the trough here often, and generously.

Time to Visit the ATM Again

Time to Visit the ATM Again

It?s fall again, when my most loyal readers are to be found taking transcontinental railroad journeys, crossing the Atlantic in an a first class suite on the Queen Mary 2, or getting the early jump on the Caribbean beaches.

What better time to spend your trading profits than after all the kids have gone back to school, and the summer vacation destination crush has subsided.

It?s an empty nester?s paradise.

Trading in the stock market is reflecting as much, with increasingly narrowing its range since the August 24 flash crash, and trading volumes are subsiding.

Is it really September already?

It?s as if through some weird, Rod Serling type time flip, August became September, and September morphed into August. That?s why we got a rip roaring August followed by a sleepy, boring September.

Welcome to the misplaced summer market.

I say all this, because the longer the market moves sideways, the more investors get nervous and start bailing on their best performing stocks.

The perma bears are always out there in force (it sells more newsletters), and with the memories of the 2008 crash still fresh and painful, the fears of a sudden market meltdown are constant and ever present.

In fact, nothing could be further from the truth.

What we are seeing unfold here is not the PRICE correction that people are used to, but a TIME correction, where the averages move sideways for a while, in this case, some five months.

Eventually, the the moving averages catch up, and it is off to the races once again.

The reality is that there is a far greater risk of an impending market melt up than a melt down. But to understand why, we must delve further into history, and then the fundamentals.

For a start, most investors have not believed in this bull market for a nanosecond from the very beginning. They have been pouring their new cash into the bond market instead.

Now that bonds have given up a third of 2015?s gains in just a few weeks, the fear of God is in them, and dreams of reallocation are dancing in their minds.

Some 95% of active managers are underperforming their benchmark indexes this year, the lowest level since 1997, compared to only 76% in a normal year.

Therefore, this stock market has ?CHASE? written all over it.

Too many managers have only three months left to make their years, lest they spend 2016 driving a taxi for Uber and handing out free bottles of water. The rest of 2015 will be one giant ?beta? (outperformance) chase.

You can?t blame these guys for being scared. My late mentor, Morgan Stanley?s Barton Biggs, taught me that bull markets climb a never-ending wall of worry. And what a wall it has been.

Worry has certainly been in abundance this year, what with China collapsing, ISIL on the loose, Syria exploding, Iraq falling to pieces, the contentious presidential elections looming, oil in free fall, , the worst summer drought in decades, flaccid economic growth, and even a rampaging Donald Trump.

We also have to be concerned that my friend, Fed governor Janet Yellen, is going to unsheathe a giant sword and start hacking away at bond prices, as she has already done with quantitative easing (I?ve been watching Game of Thrones too much).

This will raise interest rates sooner, and by more.

Let me give you a little personal insight here into the thinking of Janet Yellen. It?s all about the jobs. Any hints about rate rises have been head fakes, especially when they come from a small, anti QE Fed minority.

When in doubt, Janet is all about easy money, until proven otherwise. Until then, think lower rates for longer, especially on the heels of a disappointing 173,000 August nonfarm payroll.

So I think we have a nice set up here going into Q4. It could be a Q4 2013 lite--a gain of 5%-10% in a cloud of dust.

The sector leaders will be the usual suspects, big technology names, health care, biotech (IBB), and energy (COP), (OXY). Banks (BAC), (JPM), (KBE) will get a steroid shot from rising interest rates, no matter how gradual.

To add some spice to your portfolio (perhaps at the cost of some sleepless nights), you can dally in some big momentum names, like Tesla (TSLA), Netflix (NFLX), Lennar Husing (LEN), and Facebook (FB).

You Mean it?s September Already?

You Mean it?s September Already?