I went to the local branch of Wells Fargo Bank (WFC) yesterday, and I was appalled. The bank occupied the most expensive corner in town. It was staffed by a dozen people, all of whom spoke English as a second language.

Ask even the simplest question and they had to call a support center and wait 10 minutes on hold for the answer. It took an hour for me to open a checking account for one of my kids. The branch was in effect a glorified call center.

I thought, "This can't last." And it won't.

Banks were supposed to be the sector to own this year. They had everything going for them. The economy was booming, interest rates were rising, and regulations were falling like leaves in the fall.

Despite all these gale force fundamental tailwinds the banks have utterly failed to deliver. The gold standard J.P. Morgan is up only 8.46% on the year, while bad boy Citibank (C) is down 5.47%, and the vampire squid Goldman Sachs (GS) is off a gut-punching 10.27%. Where did the bull market go? Why have bank shares performed so miserably?

The obvious reason could be that the improved 2018 business environment was entirely discounted by the big moves we saw in 2017. Last year, banks were the shares to own with (JPM) shares up a robust 24.5%, while (C) catapulted by 29.3%.

It is possible that bank shares are acting like a very early canary in the coal mine, tweeting about an approaching recession. Loan growth has been near zero this year. That is not typical for a booming economy. It IS typical going into a recession.

When the fundamentals arrive as predicted but the stock fails to perform it can only mean one thing. The industry is undergoing a long-term structural change from which it may not recover. Yes, the bank industry may be the modern-day equivalent of the proverbial buggy whip maker just before Detroit took over the transportation business.

Managing a research service such as the Mad Hedge Technology Letter, it is easy to see how this is happening. Financial services are being disrupted on a hundred fronts, and the cumulative effect may be that it will no long exist.

This explains why this is the first bull market in history where there has been no new hiring by Wall Street. What happens when we go into a bear market? Employment will drop by half and those expensive national branch networks will disappear.

Financial services are still rife with endless fees, poor service, and uncompetitive returns. Online brokers such as Robin Hood (click here) will execute stock and option transactions for free. Now that overnight deposits actually pay a return they make their money on margin loans. They have no branch network but are still SIPC insured.

Legacy brokers such as Fidelity and Charles Schwab (SCHW) used to charge $25 a share to execute and are still charging $7.00 for full-service clients. And it's not as if their research has been so great to justify these high prices either. In a world that is getting Amazoned by the day, these high prices can't stand.

Regular online banking service also pay interest and are about to eat the big banks' lunch. Many now pay 1.75% overnight interest rates and offer free debit and credit cards, and checking accounts. Of course, none of these are household names yet, but they will be.

To win the long-term investment game you have to identify the industries of the future and run from the industries of the past. The legacy financial industry is increasingly looking like a story from the past.

Are Big Banks Ready for the Future?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-14 01:22:162018-08-14 01:22:16Why Banks Have Performed So Badly This Year

Below please find subscribers Q&A for the Mad Hedge Fund Trader April Global Strategy Webinar with my guest co-host Mike Pisani of Smart Option Trading.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Are you out of Alphabet (GOOGL) and Microsoft (MSFT)?

A. I'm out of Alphabet and I'm in Microsoft, but only for the very short term. I'm waiting for another big meltdown day to go back and buy everything back because I think the FANGs and technology in general are still in a secular bull market.

Q. Are Advanced Micro Devices (AMD) and NVIDIA (NVDA) affected by the underperformance of Bitcoin?

A. They are. Bitcoin has been an important part of the chip story for the last two years because mining, or the creation of bitcoins, creates enormous demand for chips to do the processing. I think selling in bitcoin is over for the time being. You had a $25 billion in capital gains taxes that had to be paid by April 15.

People were paying those bills by selling their bitcoins. That's over now, and bitcoin is rallied about 30% since Tax Day because of that. So, yes, bitcoin is getting so big that it is starting to affect the chip sector meaningfully. That is another reason why we see secular long-term growth in the entire chip sector.

Mike Pisani: Interesting take on bitcoin today, and I've been with you on it. I think the worst of it is over; it's going to go. Today is the largest volume day we've seen on it so far. We're up over 15,500 contracts traded.

Q: If you're 100% cash, is now a good time to commit funds to the equity market?

A. Franz, I would say nein. Absolutely not. 2009 was the time to commit funds to the equity market. If you're 100% cash now I would stay out for the next six months. We may get a good entry point over the summer or the fall. I'll let you know when that happens because I will be jumping back in myself.

But right now, a week ahead of the worst six months of equity investment of the year, I would stay away and do research instead. Read your Mad Hedge Fund Trader letters. Build a list of names that you're going to buy on the next meltdown and practice buying meltdowns with your practice account, which doesn't use real money.

There's a lot of things you can get ready to do for the next leg up in the bull market, but buying right now, NO! I would put that in the category of, "Is it time to start shorting bonds question?" that we got a few minutes ago.

Q: Why did tech stocks sell off when they have great earnings results?

A: It's called, "Buy the rumor, sell the news." So many people already own the stocks and were expecting good earnings that there was no surprise when they were announced. These are some of the most over-owned stocks in history.

Everybody in the world owns them. Many people have multiple weightings in them, so when we enter a high-risk macro environment, which we have now, you want to get rid of the most over-owned stocks. That is exactly why all of these stocks that have had great runs are selling off, even though they have great earnings report.

Q: Are financials a good play here with interest rates rising though 3%?

A. Normally I would say yes. However, the macro background for the general market are so negative they are overwhelming any positive fundamentals specific to individual sectors like banks and stocks like Citigroup (C). By the way, financials all reported great results and got killed, so that is why I bailed out of my (C) position this morning at around cost. If you throw the best news in the world on a stock and it won't go up, it's time to get out of there.

Q: Would an unleveraged inverse ETF like the ProShares Short S&P 500 ETF (SH) be good at a spike even now?

A. Yes, but when I say spike up better expect at least 20 (SPY) points or 1,000 Dow points. All these downside ETFs are great but you've got to get in at the right price. You know as they say in trading school, the profit is always made on the "BUY" and not on the "SELL."

So, if you can get on one of these super spikes up on the short side that is a great trade. So is the ProShares Ultra Short ETF (SDS) if you want to do the 2X leverage short fund. We've recently started doing this every month. We've been shorting (SPY)s and buying (VIX) on every one of these spikes up, and it's been working like a charm.

Q: Here's the best question of the day. Your timing has been perfect says Mary in Chicago, Ill.

A: Well, I'll take that kind of question all day long. Thank you very much. You're too nice to do that.

Q: Richard is asking would you buy an NVIDIA (NVDA) LEAP?

A: I would wait for meltdown days. Remember this is a market that gives you lots of meltdown days. Just wait for the next presidential tweet and you might get another 600-700-point dip in the markets. Those are the days you buy LEAPS. You don't have to get buy writing Trade Alerts like I do. You can just enter a limit order in your account. Put it as a stupidly low level to "BUY" and you may get hit. And that's where you really make the big money in this kind of market.

Q: Is there a good one- or two-month trade in Amazon?

A: Yeah, Paul, with this volatility you can pick a big winner like Amazon and you know to buy the 250-point dips and sell the rallies. These ranges are so wide now that even a beginner can make money. So, I would say you have to wait until after tomorrow on Amazon and let them get their earnings out. We know they're going to be great. They're doing home deliveries now to your car.

Q: Can long bond interest rates go up to 4%, and if that happens what would the market do?

A: Yes, they can go up to 4%, and I expect them to probably do that next year. What will it do to the market? Answer: Cause a bear market and a recession. Is that answer clear enough? My bet is that interest rates cap in this cycle much lower than they did in past cycles, maybe 4%-5%. We have been used to zero cost of money for so long that a move to 4% would be like stabbing somebody in the chest. People are much less able to deal with rising rates than they ever have been in the past, so watch this space.

Q: Should I buy the ProShares Ultra Short Treasury ETF (TBT) or the iShares 20+ Year Treasury Bond Fund (TLT)?

A: Brad, it's really is a leverage question for you. The (TLT) is 1X; the TBT is 2X, so I would be taking profits on the (TBT) here and then buying a couple of points lower. Or if you want to keep it for the long term you can but remember the cost of carry on the TBT is around 7% a year.

Q: Yves in Paris, France is asking: What possible scenario will you see material wage growth that could lead to higher inflation?

A: We're starting to see that now with the ultra-low unemployment rates. People are having great difficulty hiring anyone in technology. But at the minimum wage level there seems to be plenty of supply. The other possibility is that the cost of everything else goes up but wages, because technology is replacing jobs so fast there may never be any increase in wages.

So, we will get inflation, but nothing like the inflation we saw in the past driven by rising wages, commodity prices, oil prices, and interest rates. Yes, money is a commodity, which can add quite a lot to the cost of leveraged companies like airlines, REITs, and so on.

Q: Will rising interest rates force the US dollar up?

A. The answer is yes! It has been a long time coming, but if rates continue to rise from here, you can expect that to lead to a continuously rising dollar and falling foreign currencies, and that will become a major drag on the economy and corporate earnings going forward.

Q: When is a good time to buy TIPS?

A: Just like your Treasury bond short, I would buy Treasury Inflation Protected Securities (TIPS) on the next rally in bond prices (TLT) and dip in yields. That will give you a decent entry point. That said, TIPS have been a horrible performer for the last 10 years because there has just been no inflation. A lot of people just keep TIPS as a hedge in their portfolio and it just costs them money every year.

Q: Which could blow up, Brad wants to know, TBT or TLT?

A: The easy answer there is probably neither. But if I had to pick between the two, the (TBT) would be the one to blow up because it's a 2X and has a lot less liquidity. So, I can't image in what world has (TBT) blowing up, but then I don't watch zombie TV shows either.

Q: I think US equities are expensive. Are emerging markets (EEM) or Europe (HEDJ) a better bet for the rest of the year?

A: I would say yes. Because if interest rates here in the US go higher that means a stronger dollar. That means a weaker US stock market. Because US companies are punished by a rising dollar. And European and Asian companies benefit from a rising dollar and falling home currencies, so that makes Europe the first choice of any of the global markets.

Q: Does oil going to $100 have a chance of bringing down the US economy?

A: Absolutely yes. If oil prices don't start to slow down, they will start having a big impact on the economy because that means rising prices for any energy consumer, which is you and me.

With no ability to offset that by rising prices of your products that would put a squeeze on any oil consuming industry, which is why things like the transports and consumer staples have been performing so poorly. If we get to $100, then you're really looking at a full-on recession and bear market for stocks. By bear market I mean down 25% or more in stocks.

Q: How do you see the India ETF?

A: We like it. India is the No. 1 pick of any hedge fund investor in emerging markets, and the ETF you can buy there is the PowerShares India Portfolio ETF (PIN).

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COMES THE FOUR HORSEMEN OF THE APOCALYPSE),

(SPY), (GOOGL), (TLT), (GLD), (AAPL), (VIX), (VXX), (C), (JPM), (HOW TO AVOID PONZI SCHEMES),

(TESTIMONIAL)

Because if you are an index player, you get to do it all over again. For the major stock indexes are now unchanged on the year. In effect, it is January 1 once more.

Unless of course you are a follower of the Mad Hedge Fund Trader. In that case, you are up an eye-popping 19.75% so far in 2018. But more on that later.

Last week we caught the first glimpse in this cycle of the investment Four Housemen of the Apocalypse. Interest rates are rising, the yield on the 10-year Treasury bond (TLT) reaching a four-year high at 2.96%. When we hit 3.00%, expect all hell to break loose.

The economic data is rolling over bit by bit, although it is more like a death by a thousand cuts than a major swoon. The heavy hand of major tariff increases for steel and aluminum is making itself felt. Chinese investment in the US is falling like a rock.

The duty on newsprint imports from Canada is about to put what's left of the newspaper business out of business. Gee, how did this industry get targeted above all others?

The dollar is weak (UUP), thanks to endless talk about trade wars.

Anecdotal evidence of inflation is everywhere. By this I mean that the price is rising for everything you have to buy, like your home, health care, college education, and website upgrades, while everything you want to sell, such as your own labor, is seeing the price fall.

We're not in a recession yet. Call this a pre-recession, which is a long-leading indicator of a stock market top. The real thing shouldn't show until late 2019 or 2020.

There was a kerfuffle over the outlook for Apple (AAPL) last week, which temporarily demolished the entire technology sector. iPhone sales estimates have been cut, and the parts pipeline has been drying up.

If you're a short-term trader, you should have sold your position in April 13 when I did. If you are a long-term investor, ignore it. You always get this kind of price action in between product cycles. I still see $200 a share in 2018. This too will pass.

This month, I have been busier than a one-armed paper hanger, sending out Trade Alerts across all asset classes almost every day.

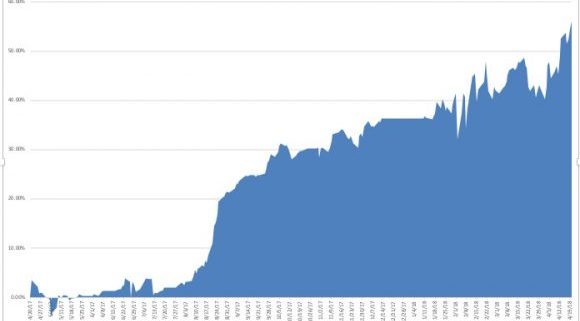

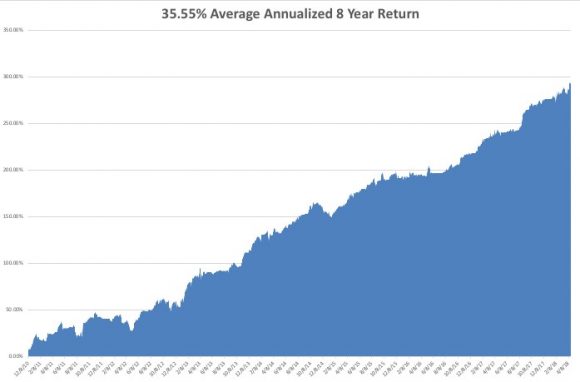

Last week, I bought the Volatility Index (VXX) at the low, took profits in longs in gold (GLD), JP Morgan (JPM), Alphabet (GOOGL), and shorts in the US Treasury bond market (TLT), the S&P 500 (SPY), and the Volatility Index (VXX). It is amazing how well that "buy low, sell high" thing works when you actually execute it. As a result, profits have been raining on the heads of Mad Hedge Trade Alert followers. That brings April up to an amazing +12.99% profit, my 2018 year-to-date to +19.75%, my trailing one-year return to +56.09%, and my eight-year performance to a new all-time high of 296.22%. This brings my annualized return up to 35.55% since inception.

The last 14 consecutive Trade Alerts have been profitable. As for next week, I am going in with a net short position, with my stock longs in Alphabet (GOOGL) and Citigroup (C) fully hedged up.

And the best is yet to come!

I couldn't help but laugh when I heard that Republican House Speaker Paul Ryan announced his retirement in order to spend more time with his family. He must have the world's most unusual teenagers.

When I take my own teens out to lunch to visit with their friends, I have to sit on the opposite side of the restaurant, hide behind a newspaper, wear an oversized hat, and pretend I don't know them, even though the bill always mysteriously shows up on my table.

This will be FANG week on the earnings front, the most important of the quarter.

On Monday, April 23, at 10:00 AM, we get March Existing-Home Sales. Expect the Sohn Investment Conference in New York to suck up a lot of airtime. Alphabet (GOOGL) reports.

On Tuesday, April 24, at 8:30 AM EST, we receive the February S&P CoreLogic Case-Shiller Home Price Index, which may see prices accelerate from the last 6.3% annual rate. Caterpillar (CAT) and Coca Cola (KO) report.

On Wednesday, April 25, at 2:00 PM, the weekly EIA Petroleum Statistics are out. Facebook (FB), Advanced Micro Devices (AMD), and Boeing (BA) report.

Thursday, April 26, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 9,000 last week. At the same time, we get March Durable Goods Orders. American Airlines (AAL), Raytheon (RTN), and KB Homes (KBH) report.

On Friday, April 27, at 8:30 AM EST, we get an early read on US Q1 GDP.

We get the Baker Hughes Rig Count at 1:00 PM EST. Last week brought an increase of 8. Chevron (CVX) reports.

As for me, I am going to take advantage of good weather in San Francisco and bike my way across the San Francisco-Oakland Bay Bridge to Treasure Island.

Good Luck and Good Trading.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Trailing-one-year-story-1-image-1-2-e1524264283463.jpg384580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-04-23 01:08:102018-04-23 01:08:10The Market Outlook for the Week Ahead, or Here Comes The Four Horsemen of the Apocalypse

There is no better sight to a hungry trader than blood in the water.

?Buy them when they?re cryin? is an excellent investment strategy that always seems to work.

There are rivers of tears being shed over the banking industry right now.

Federal Reserve officials openly told investors that after the December ?% rate hike that they would continue to do so on a quarterly basis. Only weeks later, a collapse in the stock market shattered this scenario to smithereens.

I doubt we?ll see any more Fed action in 2016.

This caught investors in bank shares wrong footed in a major way.

But wait! It gets worse!

Among the largest holders of American bank shares are the Persian Gulf sovereign wealth funds, including those for Saudi Arabia, Kuwait, Oman, Qatar, and the United Arab Emirates, my old stomping grounds. Pieces of me are still there.

The collapse in oil prices (USO) has put their budgets in tatters and they now have to sell stock to fund wildly generous social service programs. The farther Texas tea drops, the more shares they have to sell, and at $26 a barrel they have to sell bucket loads.

Had enough? There?s more.

The junk bond market (JNK) and oil company shares are suggesting that up to half of all American oil companies will go bankrupt sometime this year, mostly small ones. It all depends on how long oil stays under $40.

Unfortunately, the oil industry has been the most prolific borrower from banks for the last decade. The covenants on many of these loans require borrowers to pump and sell oil to meet interest payments NO MATTER THE PRICE! It?s a perfect formula for maxing out production and selling into a hole.

So fear of widespread energy defaults has also been dragging down bank shares as well.

Some of the moves so far in this short year have been absolutely eye popping. Bank of America (BAC) has plunged 31% from its recent high, while Citibank (C) is down 32% and JP Morgan is off 19%. Basically, they all had a terrible year just in the month of January.

Bank shares have been beaten so mercilessly that they are approaching levels last seen at the nadir of the 2009 financial crisis.

Except that this time, there is no financial crisis, not even the hint of one. For the past seven years, banks have been relentlessly raising capital, reducing leverage, and growing BIGGER.

They proved last time that they were too big to fail. Now they are REALLY too big to fail. Default rates aren?t even a fraction of what we saw during the bad old days. Energy industry borrowing is only a tenth the size of bank home loan portfolios going into the crisis.

Blame the Dodd-Frank financial regulation bill, which requires banks to hold far more capital In US Treasury bonds (TLT) than in the past, which by the way, are doing spectacularly well.

Blame ultra cautious management.

Whatever the reason, Big US banks are now solid as the Rock of Gibraltar.

Which means I?m starting to get interested. Interest rates don?t go down forever, nor does the price of oil. And scares about loan defaults are being wildly exaggerated by the media, as always.

But there is more than one way to skin a cat.

All of these companies issue high yield preferred stock with exceptionally high dividends. For example, Bank of America issued 6.2% yielding paper as recently as October. It is paying something like 8% now.

Since these securities are stock, you get to participate in price appreciation when the panic subsides. A guaranteed 8% return, plus the prospect of substantial capital appreciation? Sounds like a pretty good deal to me.

Google bank preferred shares and you will find an entire world out there of specialist advisors, dedicated newsletters and even day trading and hedging recommendations.

One thing to keep in mind here is that you should only buy ?non callable? paper. This prevents issuers from stealing your paper when better times return to cut their interest payouts.

There is another way to play this beleaguered sector.

You can buy the iShares S&P US Preferred Stock Index Fund ETF (PFF), which owns a basket of preferred stocks almost entirely made up of bank shares. As of today it was yielding 5.62%. To visit the fund?s website, please click link: https://www.ishares.com/us/products/239826/ishares-us-preferred-stock-etf.

Time to BUY?

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/ATM-Crash-e1454593247769.jpg299400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-04 01:08:092016-02-04 01:08:09Perfect Storm Hits the Banks

Regular readers of this letter are probably weary of me harping away about the financials as a great place to put your money for the rest of 2014.

Never mind that these names have all jumped 10% in the past month. But this is not an ?I told you so? story. This is more of a ?But wait, there?s more,? story.

The basis for my call is quite simple. I believe that bond prices are peaking, and yields bottoming. As mining the yield curve is a major source of bank profits, borrowing short term and lending long term, a rise in interest rates falls straight to the bottom line. Thus, buying banks is an indirect way of selling short the bond market.

However, there are many more reasons to overweight this long neglected sector. In a market that has gone virtually straight up for the past three years, many large institutions are going to be forced to roll money out of leaders, like my favored technology, energy and health care, into laggards, such as the financials.

Expect this trend to accelerate as we head into yearend institutional book closing, which start as early as October 30.

Look at other important drivers of bank profits, and you?ll find them at multi decade lows.

Trading and investment banking volumes are off 30%-40% from mean historic levels. We options traders already know this all too well, as turnover has cratered and spreads widened due to investor lack of interest.

This is especially true of put options, which are now being given away virtually for free. Volatility that seems to permanently live at the $12 handle is another such indicator of this disinterest.

This will not last. If my ?Golden Age? scenario plays out in the 2020?s (click here for ?Get Ready for the Coming Golden Age?), trading and investment banking volumes will not only double to return to the norms, they will skyrocket tenfold from today?s tedious, moribund levels.

Indeed, I have recently discovered an entire subculture of financial oriented private equity firms currently amassing portfolios that are betting on precisely such an outcome. Think of big, smart, long-term money. The big bets on the coming decade are being made now.

There is another ripple in the case for banks. After passage of the Financial Stability Act of 2010, otherwise known as ?Dodd Frank?, banks became target numero uno of the federal government. The public?s demand for accountability for the 2008-09 crash knew no bounds.

As a result, the fines and settlements with the big banks, most of which were rescued from bankruptcy by the government, now well exceed $100 billion. Four years into the enforcement onslaught, the Feds are running out of scandals to prosecute. There is nothing left for the banks to plead guilty to.

This means that a major portion of the banks? costs are about to disappear, not only new massive fines, but hundreds of millions of dollars in legal fees and diverted management time as well. More money drops to the bottom line.

Dramatically rising income? Substantially falling costs? Sounds like ?Ka-ching? to me, and a ?BUY? for the bank stocks.

The bottom line is that bank stock could double from here in coming years. It is not hard to pick names. Bank of America (BAC) took the big hit on fines and settlements, and therefore should enjoy the largest bounce.

So should Citigroup (C), which came the closest to vaporizing. And for good measure, I?ll throw in American Express (AXP) as a play on the burgeoning credit card spending by the growing class of well to do.

Barney Frank Had a Few Things to Say

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/John-Thomas-and-Barney-Frank.jpg357577Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-09-03 09:29:542014-09-03 09:29:54The Case for Buying Financials

I have discovered a correlation in the market that you can use for the rest of this year, for all of 2014, and probably for the next 20 years. Whenever the Treasury bond market (TLT) takes a dive, bank shares rocket. This is a particularly happy discovery, as my model-trading portfolio is long bank shares and short the Treasury bond market.

By buying bank shares here you are playing the second derivative of the short bond trade. Banks are about to go from being less profitable to more profitable during a falling bond, rising interest rate environment. Every trader on the street knows this, hence the sudden renaissance of the financials.

Take a look at the charts below prepared by my friends at Stockcharts.com. They show that after tracking nicely with the S&P 500 for most of the year, Financials suddenly started to drastically lag the market in October. That was on the heels of the bond market rally triggered by the Federal Reserve?s failure to taper in September.

Fast forward to two weeks ago, when I correctly called the top of the bond market and started slamming out the Trade Alerts to buy puts as fast as I could write them. Since November 1, financials have become the top performing sector of the market, and it is dragging the (SPY) upward kicking and screaming all the way.

I?ll tell you what is happening here. Traders are dumping story driven momentum stocks like Tesla (TSLA), and piling into the biggest lagging sectors for fresh meat. The dive in Treasuries gave them all the excuse they needed. That?s why the Financial Select Sector SPDR ETF (XLF) has bolted out of nowhere to a new five year high. The same is also true for Wells Fargo (WFC) and our favored Citigroup (C).

The financials rally could continue until the sector becomes overbought relative to the rest of the market, which could be well into next year. And yes, before you ask, that includes Morgan Stanley (MS) and Goldman Sachs (GS), which are really more structured like banks now in the wake of the Dodd Frank bill.

So I am going to take profits here on my existing long position in the Citigroup (C) December $45-$47 bull call spread. With the shares now trading just short of $52, we are now too far in-the-money to get much further benefit from a continued appreciation. Better to go into cash now, so I can reload on the next dip, which could happen next week.

We grabbed 80% of the potential profit holding the position a mere seven trading days. This is my 15th consecutive closing Trade Alert, and the 20th including my remaining open profitable positions. I have only six more to go until a break my previous record of 25. It doesn?t get any better than this.

Time to enter more bids on eBay for Christmas presents. That black Chanel Classic handbag with gold trim is looking pretty good. Do you think a new Brioni suit will fit into Dad?s stocking over the fireplace? Santa?.hint, hint!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Citibank.jpg361545Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-11-22 01:05:432013-11-22 01:05:43Taking Profits on Citigroup

After ignoring the financial sector for most of the year, I am more than happy to jump into it here. The sector has been a serious laggard for the past three months, trailing the front-runners I picked in technology, industrials, health care, and consumer cyclicals. After chasing these favorites, traders are now looking for new fresh meat to devour.

No one would touch financials with a bargepole while interest rates were falling. This is because banks are most profitable when short-term interest rates, where they borrow, are low, while longer-term rates that they lend at, are rising. Falling interest rates make financials a no go area. They have done so with a vengeance after the September Federal Reserve decision not to taper its quantitative easing program.

Two weeks ago interest rates bottomed and began a rapid upswing, which I believe could last many months. We could even see ten-year Treasury bonds rebound from the recent 2.47% low back up to 3.0% by year-end, and 4.0% by the end of 2014.

That?s why I called the top of the bond market two weeks ago and showered you with a machine gun succession of Trade Alerts to go short Treasuries, all of which became immediately profitable. Those who followed my advice soon found money raining down upon them.

By buying bank shares here you are playing the second derivative of the short bond trade. Banks are about to go from being less profitable to more profitable during a falling bond price, rising interest rate environment. I have published three books on this topic, so believe me, I know. Every trader on the street understands this, hence the sudden renaissance of the financials.

I picked Citibank (C) because I know the former CEO, Vikram Pandit, well having worked with him for a decade at Morgan Stanley (MS). That relationship gave me unequaled access to the inner workings of this financial institution.

Citibank is not the target of multiple government civil and criminal prosecutions, as JP Morgan (JPM) has become, thanks to the London whale incident. They also do not suffer from the legacy problems bedeviling Bank of America (BAC), which they stepped into with their multiple acquisitions during the financial crisis.

Citibank also sponsors that really cool bike sharing program in Manhattan, called, what else, Citibike.

There is another method to my ?Madness? here. Take a look at the six-month chart for (C) shares. It shows absolute rock solid support at the $47.40 floor. That makes the Citicorp December $45-$47 bull call spread a complete no-brainer.

If you don?t like Citibank you can caste a wider net and buy the Financial Select Sector SPDR ETF (XLF). You can click here to find the precise index makeup and the fund details. Berkshire Hathaway is the largest holding, with an 8.18% weighting, while Citibank is the fifth largest holding with a 6% weighting.

But Will It Take Me to a Great Trading Year?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Citibike.jpg312467Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-11-14 01:04:302013-11-14 01:04:30Loading Up On the Financials

Take a look at the chart below for the S&P 500, and it is clear that we are at the top, of a top, of a top. How much new stock do you want to buy here? Not much. Virtually every technical trading service I follow, including my own, is now flashing distressed warning signals. Maybe we really were supposed to ?Sell in May and go away.?

All RSI?s are through the roof. We have not had a pullback of more than 3.2% in six months, the longest in history. It has been up 19 Tuesdays in a row. Some 67% of this year?s gains have been on Tuesdays, and 83% since the 2012 low. So buying Monday afternoon and selling Tuesday afternoon is the new winning investment strategy. It?s a day trader?s paradise. The market is clearly cruising for a bruising here.

A 5%-10% correction seems imminent. After that, we will probably power on to a new high by the end of the year. The Vampire Squid, Goldman Sachs, posted a 1,750 target for (SPY). Why not? Their number seems as good as any. Who knew that the top market strategist for the year would be perma-bull Wharton business school professor, Jeremy Siegel?

The smart money is sitting on its hands here, maintaining discipline, and waiting for better opportunities. It is also pounding away at the research, building lists of stocks to pounce on during the second half. It is still early, but here is my short list of things to watch from the summer onward.

Apple (AAPL) ? Rotation into laggards will become the dominant theme for those playing catch up, and the biggest one out there is Apple. Buy the dips now for a 25% move up into yearend. An onslaught of new products and services will hit in the fall, and the company is still making $60 million an hour in net profits. Look for the iPhone 5s, Apple TV, and new generations of the iMac, iPad, and iPods. It will also make its China play, inking a deal with China Telecom (CHA). The world?s second largest company is not going to trade at half the market multiple for much longer, especially while that multiple is expanding. Technology is the last bargain left in the market. QUALCOMM (QCOM) might be a second choice here.

MSCI Spain Index Fund ETF (EWP) ? Look for the European economy to bottom out this summer and recover in the fall. In the end, the Germans will pay up to keep the European community together. The reach for yield and the global liquidity surge will drive interest rates on sovereign debt down as well, accelerating the move up. Also, the more expensive the US gets, the more you can expect other parts of the world to play catch up. Spain is the leveraged play here.

iShares FTSE 25 Index Fund ETF (FXI) ? Now that the new Chinese leadership has their feet under the desk, look for them to stimulate the economy. China will play catch up with the US, which should start topping out by yearend. It is also an indirect play on the reviving Japanese economy, the Middle Kingdom?s largest foreign investor. Japan has gotten too expensive to buy, so consider this a second derivative play.

Proshares Ultra Short 20+ Year Treasury ETF (TBT) ? The Treasury market bubble is history, and it is just a matter of time before we break down from these elevated prices. Look for the ten-year bond to probe the high end of the yield range at 2.50%. I don?t expect Treasuries to crash from here, but you might be able to squeeze another 25% from the (TBT) in the meantime.

Citicorp (C) ? Look, the financials are going to run all year. Use the summer dip to get back into this name, the most undervalued of the major banks, and a hedge fund favorite. A multidecade steepening of the yield curve is a huge plus for the industry. Now that real estate prices are rising, some of those dud loans on their books may actually be worth something.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Market-Pit.jpg182277Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-22 09:15:382013-05-22 09:15:38Five Stocks to Buy for the Second Half

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.