(WHY CHINA’S US TREASURY DUMP WILL CRUSH THE BOND MARKET),

(TLT), (TBT), ($TNX), (FCX), (FXE), (FXY), (FXA),

(USO), (OXY), (ITB), (LEN), (HD), (GLD), (SLV), (CU),

(THE 13 NEW TRADING RULES FOR 2019)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-27 01:08:542019-02-27 00:50:55February 27, 2019

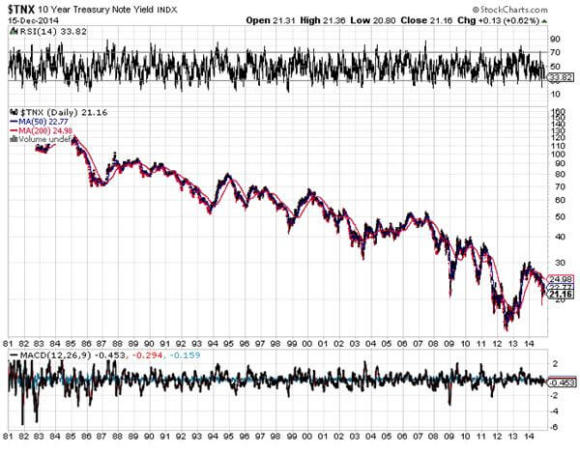

Years ago, if you asked traders what one event would destroy financial markets, the answer was always the same: China dumping its $1 trillion US treasury bond hoard.

It looks like Armageddon is finally here.

Once again, the Chinese boycotted this week’s US Treasury bond auction.

With a no-show like this, you could be printing a 2.90% yield in a couple of weeks. It also helps a lot that the charts are outing in a major long term double top.

You may read the president’s punitive duties on Chinese solar panels as yet another attempt to crush California’s burgeoning solar installation industry. I took it for what it really was: a signal to double up my short in the US Treasury bond market.

For it looks like the Chinese finally got the memo. Exploding American deficits have become the number one driver of all asset classes, perhaps for the next decade.

Not only are American bonds about to fall dramatically in value, so is the US dollar (UUP) in which they are denominated. This creates a double negative hockey stick effect on their value for any foreign investor.

In fact, you can draw up an all assets class portfolio based on the assumption that the US government is now the new debt hog:

Stocks – buy inflation plays like Freeport McMoRan (FCX) and US Steel (X) Emerging Markets – Buy asset producers like Chile (ECH) Bonds – run a double short position in the (TLT) Foreign Exchange – buy the Euro (FXE), Yen (FXY), and Aussie (FXA) Commodities – Buy copper (CU) as an inflation hedge Energy – another inflation beneficiary (USO), (OXY) Precious Metals – entering a new bull market for gold (GLD) and silver (SLV)

Yes, all of sudden everything has become so simple, as if the fog has suddenly been lifted.

Focus on the US budget deficit which has soared from $450 billion a year ago to over $1 trillion today on its way to $2 trillion later this year, and every investment decision becomes a piece of cake.

This exponential growth of US government borrowing should take the US National Debt from $22 to $30 trillion over the next decade.

I have been dealing with the Chinese government for 45 years and have come to know them well. They never forget anything. They are still trying to get the West to atone for three Opium Wars that started 180 years ago.

Imagine how long it will take them to forget about washing machine duties?

By the way, if I look uncommonly thin in the photo below it’s because there was a famine raging in China during the Cultural Revolution in which 50 million died. You couldn’t find food to buy in the countryside for all the money in the world. This is when you find out that food has no substitutes. The Chinese government never owned up to it.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Man-in-China-story-2-image-6.jpg225336Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-27 01:07:462019-07-09 04:06:37Why China’s US Treasury Dump Will Crush the Bond Market

You wanted clarity in understanding the current state of play in the global financial markets? Here?s your #$%&*#!! clarity.

You should expect nothing less for this ridiculously expensive service of mine.

But maybe that is the cabin fever talking, now that I have been cooped up in my Tahoe lakefront estate for a week, engaging in deep research and grinding out the Trade Alerts, devoid of any human contact whatsoever.

Or, maybe it?s the high altitude.

I did have one visitor.

A black bear broke into my trash cans last light and spread garbage all over the back yard. He then left his calling card, a giant poop, in my parking space.

Judging by the size of the turds, I would say he was at least 600 pounds. This is why you never take out the trash at night in the High Sierras.

Ah, the delights of Mother Nature!

We certainly live in a confusing, topsy-turvy, tear your hair out world this year. Good news is bad news, bad news worse, and no news the worst of all.

The biggest under performing week of the year for stocks is then followed by the best. Net net, we are absolutely at a zero movement, and lots of clients complaining about poor returns on their investment.

I tallied the year-on-year performance of every major assets class and this is what I found.

+16% - Hedged Japanese Stocks (DXJ)

+15% - Hedged European stocks (HEDJ)

+13% - US dollar basket (UUP)

+10% - My house

0% - Stocks (SPY)

0% -? bonds (TLT)

-5% - Japanese Yen (FXY)

-11% - Euro (FXE)

-12% - Gold (GLD)

-18% -? Oil (USO)

-27% -? Commodities (CU)

-27% - Natural Gas (UNG)

There are some sobering conclusions to be drawn from these numbers.

There were very few opportunities to make money this year. If you were short energy, commodities, and foreign currencies, you did very well.

Followers of the Mad hedge Fund Trader can?t help but know and love these ticker symbols. They?ll notice that our long plays were found among the asset classes with the best performance, while our short bets populated the losers.

The problem with that is most financial advisors are not permitted to place client funds in the sort of inverse or leveraged ETF?s that most benefit from these kinds of moves (like the (YCS), (EUO), and (DUG)).

That left them reading about the success of others in the newspapers, even when they knew these trends were unfolding (through reading this letter).

How frustrating is that?

What was one of my best investments of 2015?

My San Francisco home, which has the additional benefit in that I get to live in it, have a place to stash all my junk, and claim big tax deductions (depreciated home office space, business use of phone, blah, blah, blah).

Of course, I do have the advantage of living in the middle of one of the greatest technology and IPO booms of all time. Every time one of these ?sharing? companies goes public, the value of my home rises by a few hundred grand.

The real problem here is that investing since the end of the Federal Reserve?s quantitative easing program ended a year ago has become a real uphill battle.

While the government was adding $3.9 trillion in funds to the economy we traders enjoyed one of the greatest free lunches of all time. It made us all look like freakin? geniuses!

Just maintaining their present $3.9 trillion balance sheet, not adding to it, has left almost every asset class dead in the water.

Heaven help us if they ever try to unwind some of that debt!

Janet has promised me that she isn?t going to engage in such monetary suicide.

The Fed is continuing with Ben Bernanke?s plan to run all of their Treasury bond holdings into expiration, even if it takes a decade to achieve this. And with deflation accelerating (see charts below), the need for such a desperate action is remote.

Still, one has to ponder the potential implications.

It all kind of makes my own 43% Trade Alert gain in 2015 look pretty good. But I don?t want to boast too much. That tends to invite bad luck and losses, which I would much rather avoid.

What! No QE?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/11/Ship-Torpedoed-e1448310356189.jpg265400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-11-24 01:08:272015-11-24 01:08:27Bring Back QE!

Watching the entire commodity complex collapse in unison this year was nothing less than amazing, with many down 30% or more. And I mean the broader definition of commodity.

It includes the base metals like copper (JJC), (CU), agricultural products (CORN), (SOYB), (DBA), precious metals (GLD), (SLV), and even energy (USO), (KOL).

If you look carefully, you can find commonality in many, but not all, of these.

A slowing China meant that global consumption of bulk commodities would recede to a low ebb. The Chinese stock market crash threw gasoline on the fire.

A bull market in US stocks produced a world clamoring for paper assets at the expense of hard ones.

And of course, the high prices seen in all of these nearly four years ago cured high prices, drawing in new production from untold corners of the earth.

This is how bubbles always end.

What leaves many scratching heads is how widespread the route became. Those clever people who used one commodity to hedge another were left with portfolios of ashes, as everything plunged in lockstep.

The big talk now among my global strategist friends is this: will this year?s dogs become next year?s Cinderellas?

It is easy to imagine how this could happen. For a start, the higher paper stocks rise, the cheaper commodities look. They are now starting to appear like great laggard/diversification plays.

Here is another conundrum.

The world is on track for a global synchronized recovery, with the US. China, Japan and Europe all going ?pedal to the metal? to spur economic growth.

So how is it supposed to do this without using more commodities?

Yes, you can argue, there are big stockpiles to eat through before we see any real price appreciation. But stores can be exhausted in mere months.

This is why I am starting to get interested in the entire commodity space. I have already executed a couple of profitable trades in Freeport McMoRan (FCX) this year-- one of the world?s largest copper producers.

And if my old friend, Carl Icahn, is interested, should I be?

I look forward to more visits to the trough.

Higher prices for commodities in 2016 may not turn out to be a fairy tale after all.

A Commodity Recovery in 2016 is No Fairy Tale

https://www.madhedgefundtrader.com/wp-content/uploads/2013/12/Cinderella.jpg263347Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-09-10 01:07:472015-09-10 01:07:47Is This the Big Trade of 2016?

I am writing this to you from Terminal 2 at San Francisco Airport, awaiting my Virgin America flight to Chicago.

My conclusion so far is that the beef curry rice at the Japanese fast food joint Wakaba isn?t what it used to be. The meat is paper thin and full of fat and gristle. I guess everyone is trying to cut costs these days.

I saw a tall blond hustle by in a pilot?s uniform, and thought I recognized her behind as that of my former flight instructor from decades ago. But when I caught up with her, I learned she worked for American Airlines. Emmy flew for United. And I was off by a generation on the age.

That?s the problem with reaching Medicare age. You can?t see worth a damn, and all of your friends are dead. At least the landings are exciting when I am the pilot.

There?s nothing like getting in on the ground floor of a raging bull market in commodities to get your juices flowing, even for a senior citizen.

That?s what I did when I jumped into the Freeport McMoRan (FCX) May, 2015 $17-$18 deep in-the-money vertical call spread two weeks ago. This is the second time in a month I have coined it with this name, the world?s largest producer of copper.

Since (FCX) began its torrid move in mid April, the shares have added an eye popping $6, or 35%. That?s a winner and a half.

Many thanks to my many subscribers who work at Freeport, although I assure you, you had absolutely nothing to do with the recent move in your stock.

This is despite the fact that prices for the red metal (CU) have remained virtually unchanged during this period.

Instead, there is a parade of people I wish to thank for the success of this trade.

First, I have to tip my hat to Federal Reserve Chairman, Janet Yellen, for making it abundantly clear to me on countless occasions that she has absolutely no intention of raising interest rates this year. This has knocked the wind out of the greenback, forced a 5% correction, and given newfound strength to commodity stocks like (FCX).

Hey, Janet, call me!

I also want to thank the government in Beijing for the assist, which announced a major program to stimulate the Chinese economy right after I strapped on this trade, through the reduction of bank reserve requirements from 18.5% to 17.5%.

China is the world?s largest consumer of copper, and a stronger economy consumes more of the stuff, boosting prices northward.

I owe you all a Peking duck dinner for this one. Might I suggest the Da Dong Roast Duck Restaurant on Dongsi on the 10th Alley in Beijing? They?re supposed to be the best in town.

Finally, one can?t ignore the contribution of the Houthi rebels in Yemen for inspiring a sharp rally in the price of crude oil (USO), which helped drag up the price of other commodity stocks as well, including those producing copper.

For you I owe a round of falafels and cooked sheep?s eyes, favorites of yours, I know. However, I?ll have to mail this one in, lest a CIA Predator drone strike take me out over dinner.

You can sell this vertical bull call spread anywhere around the $0.99 and lock in 92% of the potential profit in this trade. Or you can run it until the May 15 expiration, ten trading days away, and collect the last penny or two.

Either way, it?s time to declare victory on this one and move on to the next one.

The spread clocked a gain in 12.5% in two weeks. That is on top of the one day 22.5% wonder we earned with the Freeport McMoRan (FCX) May, 2015 $16-$17 deep in-the-money vertical call spread.

When it rains, it pours.

If instead of buying the (FCX) call spread, you purchased the shares outright, the First Trist ISE Global Copper ETF (CU), First Quantum Minerals Ltd. (FM.TO), Antofagasta (ANTO.L), hang on. We are going much higher.

The 200-day moving average beckons at $26.33. And if the Chinese economic recovery is real, as the stock market there seems to think, you can easily double that target.

I have a feeling that Freeport McMoRan is my new rich uncle, cutting me generous maintenance checks every month.

So I?ll be looking to roll back into the next set of strike prices higher up and a maturity farther out at the next dip in the stock.

See you There Beijing

https://www.madhedgefundtrader.com/wp-content/uploads/2015/04/Beijing-Restaurant-e1430398966155.jpg241400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-05-01 01:05:472015-05-01 01:05:47Cashing in on Freeport McMoRan

So far in 2015 the Indian stock market has handily beaten that of the US, by 10.6% compared to 5.3%.

?The India election result is the biggest development to affect emerging markets over the last 30 years.? That is what retired chairman of Goldman Sachs Asset Management and originator of the ?BRIC? term, Jim O?Neal, told me last week.

Indeed, the stunning news has sent long term country specialists scampering. In my long term strategy lectures I have been titillating listeners for years with predictions that India was about to become the next China.

With half the per capita income of the Middle Kingdom, India was lacking the infrastructure needed to compete in the global marketplace. All that was needed was the trigger.

This is the trigger.

With a new party taking control of the government for the first time in 50 years, the way is now clear to carry out desperately needed sweeping political and economic reforms. At the top of the list is a clean sweep of corruption, long endemic to the subcontinent. I once spent four months traveling around India on the Indian railway system, and the demand for ?bakshish? was ever present.

A reviving and reborn India has massive implications for the global economy, which could see growth accelerate as much at 0.50% a year for the next 30 years. This will be great news for stocks everywhere. It will help offset flagging demand for commodities from China, like coal (KOL), iron ore (BHP), and the base metals (CU).

Demand for oil (USO) grows, as energy starved India is one of the world?s largest importers.

A strengthening Rupee, higher standards of living, and relaxed import duties should give a much needed boost for gold (GLD). India has always been the world?s largest buyer.

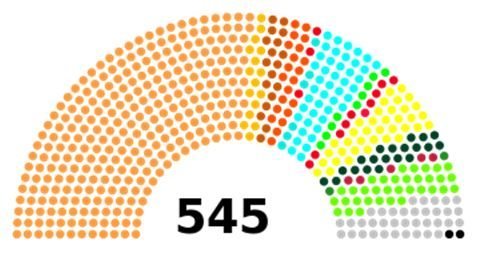

The world?s largest democracy certainly delivers the most unusual of elections, a blend of practices from today?.and a thousand years ago. It was carried out over five weeks, and a stunning 541 million voted, out of an eligible 815 million, a turnout of 66.4%. That is far higher than elections seen here in the United States.

Of the 552 members in the Lok Sabha, the lower house (or their House of Representatives), a specific number of seats are reserved for scheduled castes, scheduled tribes, and women. Gee, I wonder which one of these I would fit in?

Important issues during the campaign included rising prices, the economy, security, and infrastructure such as roads, electricity and water. About 14% of voters cited corruption as the main issue.

Some 12 political parties ran candidates. The winner was Hindu Nationalist Narendra Modi of the Bharatiya Janata Party (BJP), who led a diverse collection of lesser parties to take an overwhelming majority. For more details on this fascinating election, please click here at http://www.ndtv.com/elections.

It is still early days for the Bombay stock market, which has already rocketed by a stunning 20% since the election results became obvious last week.

This could be the beginning of a ten-bagger move over coming decades. Managers are hurriedly pawing through stacks of research on the subcontinent they have been ignoring for the past four years, the last time emerging markets peaked.

In the meantime, the action has spilled over into other emerging markets (EEM), their currencies (CEW), and their bonds (ELD), which have all punched through to new highs for the year.

I?ll be knocking out research o specific names when I find them. Until then, use any dip to pick up the Indian ETF?s (INP), (PIN), and (EPI).

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/India-Election-Results.jpg254477Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-24 01:03:152015-02-24 01:03:15The Game Changer in India

When the Trade Alerts quit working. I stop sending them out. That?s my trading strategy right now. It?s as simple as that.

So when I received a dozen emails this morning asking if it is time to double up on Linn Energy (LINE), I shot back ?Not yet!? There is no point until oil puts in a convincing bottom, and that may be 2015 business.

Traders have been watching in complete awe the rapid decent the price of Linn Energy, which is emerging as the most despised asset of 2014, after commodity producer Russia (RSX).

But it is becoming increasingly apparent that the collapse of prices for the many commodities is part of a much larger, longer-term macro trend.

(LINN) is doing the best impersonation of a company going chapter 11 I have ever seen, without actually going through with it. Only last Thursday, it paid out a dividend, which at today?s low, works out to a mind numbing 30% yield.

I tried calling the company, but they aren?t picking up, as they are inundated with inquires from investors. Search the Internet, and you find absolutely nothing. What you do find are the following reasons not to buy Linn Energy today:

1) Falling oil revenue is causing Venezuela to go bankrupt. 2) Large layoffs have started in the US oil industry. 3) The Houston real estate industry has gone zero bid. 4) Midwestern banks are either calling in oil patch loans, or not renewing them. 5) Hedge Funds have gone catatonic, their hands tied until new investor funds come in during the New Year. 6) Every oil storage facility in the world is now filled to the brim, including many of the largest tankers.

Let me tell you how insanely cheap (LINN) has gotten. In 2009, when the financial system was imploding and the global economy was thought to be entering a prolonged Great Depression, oil dropped to $30, and (LINN) to $7.50. Today, the US economy is booming, interest rates are scraping the bottom, employment is at an eight year high, and (LINE) hit $9.70, down $70 in six months.

Go figure.

My colleague, Mad Day Trader, Jim Parker, says this could all end on Thursday, when the front month oil futures contract expires. It could.

It isn?t just the oil that is hurting. So are the rest of the precious and semi precious metals (SLV), (PPLT), (PALL), base metals (CU), (BHP), oil (USO), and food (CORN), (WEAT), (SOYB), (DBA).

Many senior hedge fund managers are now implementing strategies assuming that the commodity super cycle, which ran like a horse with the bit between its teeth for ten years, is over, done, and kaput.

Former George Soros partner, hedge fund legend Paul Tudor Jones, has been leading the intellectual charge since last year for this concept. Many major funds have joined him.

Launching at the end of 2001, when gold, silver, copper, iron ore, and other base metals, hit bottom after a 21 year bear market, it is looking like the sector reached a multi decade peak in 2011.

Commodities have long been a leading source of profits for investors of every persuasion. During the 1970?s, when president Richard Nixon took the US off of the gold standard and inflation soared into double digits, commodities were everybody?s best friend. Then, Federal Reserve governor, Paul Volker, killed them off en masse by raising the federal funds rate up to a nosebleed 18.5%.

Commodities died a long slow and painful death. I joined Morgan Stanley about that time with the mandate to build an international equities business from scratch. In those days, the most commonly traded foreign securities were gold stocks. For years, I watched long-suffering clients buy every dip until they no longer ceased to exist.

The managing director responsible for covering the copper industry was steadily moved to ever smaller offices, first near the elevators, then the men?s room, and finally out of the building completely. He retired early when the industry consolidated into just two companies, and there was no one left to cover. It was heartbreaking to watch. Warning: we could be in for a repeat.

After two decades of downsizing, rationalization, and bankruptcies, the supply of most commodities shrank to a shadow of its former self by 2000. Then, China suddenly showed up as a voracious consumer of everything. It was off to the races, and hedge fund managers were sent scurrying to look up long forgotten ticker symbols and futures contracts.

By then commodities promoters, especially the gold bugs, had become a pretty scruffy lot. They would show up at conferences with dirt under their fingernails, wearing threadbare shirts and suits that looked like they came from the Salvation Army. As prices steadily rose, the Brioni suits started making appearances, followed by Turnbull & Asser shirts and Gucci loafers.

There was a crucial aspect of the bull case for commodities that made it particularly compelling. While you can simply create more stocks and bonds by running a printing press, or these days, creating digital entries on excel spreadsheets, that is definitely not the case with commodities. To discover deposits, raise the capital, get permits and licenses, pay the bribes, build the infrastructure, and dig the mines and pits for most commodities, takes 5-15 years.

So while demand may soar, supply comes on at a snail pace. Because these markets were so illiquid, a 1% rise in demand would easily crease price hikes of 50%, 100%, and more. That is exactly what happened. Gold soared from $250 to $1,922. This is what a hedge fund manager will tell us is the perfect asymmetric trade. Silver rocketed from $2 to $50. Copper leapt from 80 cents a pound to $4.50. Everyone instantly became commodities experts. An underweight position in the sector left most managers in the dust.

Some 14 years later and now what are we seeing? Many of the gigantic projects that started showing up on drawing boards in 2001 are coming on stream. In the meantime, slowing economic growth in China means their appetite has become less than endless.

Supply and demand fell out of balance. The infinitesimal change in demand that delivered red-hot price gains in the 2000?s is now producing equally impressive price declines. And therein lies the problem. Click here for my piece on the mothballing of brand new Australian iron ore projects, ?BHP Cuts Bode Ill for the Global Economy?.

But this time it may be different. In my discussions with the senior Chinese leadership over the years, there has been one recurring theme. They would love to have America?s service economy.

I always tell them that they have a real beef with their ancient ancestors. When they migrated out of Africa 50,000 years ago, they stopped moving the people exactly where the natural resources aren?t. If they had only continued a little farther across the Bering Straights to North America, they would be drowning in resources, as we are in the US.

By upgrading their economy from a manufacturing, to a services based economy, the Chinese will substantially change the makeup of their GDP growth. Added value will come in the form of intellectual capital, which creates patents, trademarks, copyrights, and brands. The raw material is brainpower, which China already has plenty of.

There will no longer be any need to import massive amounts of commodities from abroad. If I am right, this would explain why prices for many commodities have fallen further that a Middle Kingdom economy growing at a 7.5% annual rate would suggest. This is the heart of the argument that the commodities super cycle is over.

If so, the implications for global assets prices are huge. It is great news for equities, especially for big commod

ity importing countries like the US, Japan, and Europe. This may be why we are seeing such straight line, one way moves up in global equity markets this year.

It is very bad news for commodity exporting countries, like Australia, South America, and the Middle East. This is why a large short position in the Australian dollar is a core position in Tudor-Jones? portfolio. Take a look at the chart for Aussie against the US dollar (FXA) since 2013, and it looks like it has come down with a severe case of Montezuma?s revenge.

The Aussie could hit 80 cents, and eventually 75 cents to the greenback before the crying ends. Australians better pay for their foreign vacations fast before prices go through the roof. It also explains why the route has carried on across such a broad, seemingly unconnected range of commodities.

In the end, my friend at Morgan Stanley had the last laugh.

When the commodity super cycle began, there was almost no one around still working who knew the industry as he did. He was hired by a big hedge fund and earned a $25 million performance bonus in the first year out. And he ended up with the biggest damn office in the whole company, a corner one with a spectacular view of midtown Manhattan.

He is now retired for good, working on his short game at Pebble Beach.

Good for you, John.

Not as Shiny as it Once Was

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Gold-Coins.jpg391380Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-16 01:03:502014-12-16 01:03:50End of the Commodity Super Cycle

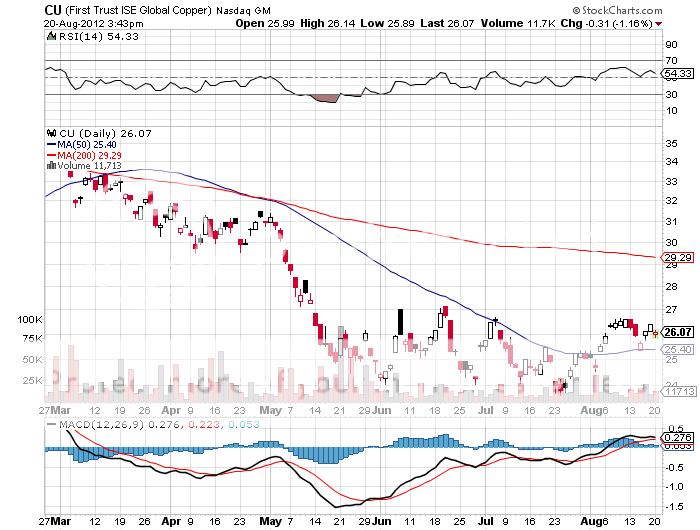

When Dr. Copper (CU), the only commodity with a PhD in economics, suddenly collapses from a heart attack, risk takers everywhere have to sit up and take notice.

Since the 2011 top, the red metal has collapsed a shocking 40%. It has given back a nausea inducing 10% just in the last two weeks. Will copper take down the rest of the financial markets with it?

Is the bull case for risk assets over?

I doubt it.

So called because of its uncanny ability to predict the future of the global economy, copper is warning of dire things to come. The price drop suggests that the great Chinese economic miracle is coming to an end, or is at least facing a substantial slowdown, the government?s 7.5% GDP target for 2014 notwithstanding.

It?s a little more complicated than that. Copper is no longer the metal it once was. Because of the lack of a consumer banking system in the Middle Kingdom, individuals are now hoarding 100 pound copper bars and posting them as collateral for loans from banks or backstreet money lenders.

China is, in effect, on a copper standard. Get any weakness of the kind we have seen this year, and lenders panic, dumping their collateral for cash, crushing spot prices.

The latest plunge has been fueled by continuing rumors of an imminent Chinese banking crisis. The Middle Kingdom?s first corporate bond default in history, by a third tier solar company a few years ago, further heightened fears. The implicit government guarantee that was believed to back this paper suddenly went missing in action.

The high frequency traders are now in the copper futures and spot markets in force, whipping around prices and creating unprecedented volatility. Notice how they seem to be running the movie on fast forward everywhere these days? Because of this, we could now be seeing an overshoot on the downside in copper.

Copper, along with all other hard assets, have also been taking a pasting from the strong US dollar. A robust greenback has effectively raised the price of copper in non dollar currencies in big consuming countries, like Japan and Europe. The only way to adjust for this is for the traders to take down dollar prices, which the markets have been doing with a vengeance.

It is no coincidence that copper has been falling in almost perfect lockstep with the rest of the hard asset universe, including gold, silver, oil, natural gas, coal, all the ags and ag stocks, and the commodity producing currencies of the Australian (FXA) and Canadian (FXC) dollars. The world wants paper assets (stocks and bonds), and none of the stuff you can drop on your foot (thanks Dennis).

However, cheaper copper is ultimately great news for we copper consumers, as with everything else.

Watch Dr. Copper closely. At the first sign of any real bottom, you should load up on long dated calls for Freeport McMoRan (FCX), the world?s largest producer, which also has been similarly decimated. The leverage in the company is such that a 10% rise in the price of copper triggers a rapid 20% rise or more in (FCX) shares.

I can wax one here about major structural changes in the Chinese economy that are underway, as the real problem. As the Middle Kingdom shifts from an export driven economy to a domestic demand one, there is less need for the red metal and more need for silicon and brains. But this isn?t something you can trade off of today.

So what is copper really telling us? The longer-term charts show a prolonged bottoming process. If $2.90 fails, we could see a revisit to the five-year low at $2.50.

That?s your load the boat price. During the global synchronized economic recovery that is underway, you want to view every panic sell off in a single asset class like this as a gift.

There is one further hope for copper. The Shanghai stock market has been absolutely on fire this year, rocketing some 40% since June, even beating the heady US exchanges. When risk accumulation accelerates to this extent in the world?s largest copper consumer that is great news for copper.

The two asset classes are now wildly out of sync. Either Chinese stocks are ridiculously overpriced and soon have to crash to come back in line with the red metal. Or copper has to rise.

I vote for the latter. It could be your big New Year trade.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/Pennies-e1417727294545.jpg299400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-05 01:04:382014-12-05 01:04:38Here is Your Big New Year Trade

When Dr. Copper (CU), the only commodity with a PhD in economics, suddenly collapses from a heart attack, risk takers everywhere have to sit up and take notice. Since the 2011 top, the red metal has collapsed a shocking 35%.

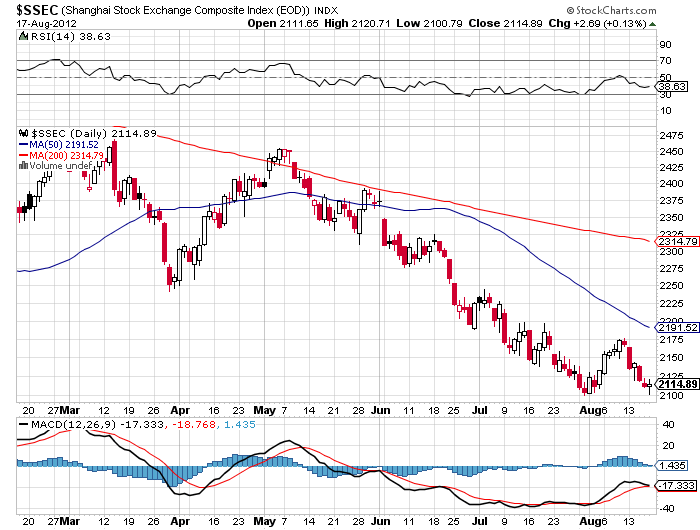

So called because of its uncanny ability to predict the future of the global economy, copper is warning of dire things to come. The price drop suggests that the great Chinese economic miracle is coming to an end, or is at least facing a substantial slowdown. This dark view is further confirmed by the weakness in the Shanghai index ($SSEC) which has been trading like grim death all year. Will China permabear, Jim Chanos, finally get his dream come true?

It?s a little more complicated than that. Copper is no longer the metal it once was. Because of the lack of a consumer banking system in the Middle Kingdom, individuals are now hoarding 100 pound copper bars and posting them as collateral for loans. Get any weakness of the kind we have seen this year, and lenders panic, dumping their collateral for cash.

The high frequency traders are now in there in force, whipping around prices and creating unprecedented volatility. You can see this also in gold, silver, oil, coal, platinum, and palladium. Notice how they seem to be running the movie on fast forward everywhere these days? Because of this, we could now be seeing an overshoot on the downside in copper which may never actually materialize to this extreme in equities or other asset classes.

Watch Dr. Copper closely. At the first sign of any sustained strength, you should load up on long dated calls for Freeport McMoRan (FCX), the world?s largest producer, which also has been similarly decimated. The gearing in the company is such that a 50% rise in the price of copper triggers a 100% rise in (FCX).

So what is copper telling us today? The longer term charts show a prolonged bottoming process. If this holds, we could be seeing the early days of a resurgence in the global economy. Just get Syria, Egypt, the debt ceiling crisis, and the taper out of the way, and we could be in for a major run. That is a tall order. But just to be safe, I am buying long dated calls in the next major dip in (FCX), which may have started today.

A Penny for Your Thoughts on Copper?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Pennies.jpg274399Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-28 01:03:562013-08-28 01:03:56The Great Copper Crash of 2013

It is a fact of life that markets get overstretched. Think of pulling on a rubber band too hard, or loading too many paddlers at one end of a canoe. Whatever the metaphor, the outcome is always unpleasant and sometimes disastrous.

Take a look at the charts below and you can see how extended markets have become. Stocks (DIA), (QQQ), (IWM) have reached the top of decade and a half trading ranges. Bonds (TLT), (LQD) are at three month lows, and yields have seen the sharpest back up in over a year.

In the meantime, the non-confirmations of these trends are a dime a dozen. Every trader?s handbook says that you unload risk assets like crazy whenever you see the volatility index (VIX) trade in the low teens for this long. The Shanghai Index ($SSEC), representative of the part of the world that generates 75% of the world?s corporate profits, hit a new four year low last night. Copper (CU) doesn?t believe in this risk rally for a nanosecond. Nor is the Australian dollar (FXA) signaling that happy days are here again.

I am betting that when the whales come back from their vacations in Southampton, Portofino, or the South of France, they are going to have a heart attack when they see the current prices of risk assets. A big loud ?SELL? may be the consequence of a homecoming. A Jackson Hole confab of central bankers that delivers no substantial headlines next week could also deliver the trigger for a sell off.

You may have noticed that European Central Bank president, Mario Draghi, has come down with a case of verbal diarrhea this summer. His pro-bailout comments have been coming hot and heavy. When the continent?s leaders return from their extended six week vacations, it will be time to put up or shut up. The final nail in this coffin could be A Federal Reserve that develops lockjaw instead of announcing QE3 at their September 12-13 meeting of the Open Market Committee.

To me, it all adds up to a correction of at least 5%, or 70 points in the S&P 500, down to 1,350. I?m not looking for anything more dramatic than that in the run up to the presidential election. I am setting up my bear put spreads to reach their maximum point of profitability in the face of such a modest setback. A dream come true for the bears would be a retest of the May lows at 1,266, however unlikely that may be.

For the real crash, you?ll have to wait for 2013 when a recession almost certainly ensues. Stay tuned to this letter as to exactly when that will begin.

?The Real Crash Isn?t Coming Until 2013

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-20 23:03:132012-08-20 23:03:13Watch Out for the Coming Risk Reversal

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.