Below please find subscribers' Q&A for the Mad Hedge Fund Trader May 23 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Would you short Tesla here?

A: Tesla (TSLA) is on the verge of making the big leap to mass production, so they're in somewhat of an in-between time from a profit point of view, and the burden of proof is on them. Elon Musk is notorious for squeezing shorts. I would not want to bet him.

Musk has been successfully squeezing shorts for 10 years now, from the time the stock was at $16.50 all the way up to $392. So, I would not short Tesla. Buy the car but don't play in the stock; it's really a venture capital play that happens to have a stock listing because so many people are willing to back his vision of a carbon-free economy.

Q: What is your takeaway on the China trade war situation?

A: The Chinese said "no," and that is positive for economic growth. Anything that enhances international trade is good for growth and good for the stock market; anything that damages international trade is bad for corporate earnings and bad for the stock market. So, the China win in the trade war is essentially positive, but I don't think we'll see that reflected in stock prices until the end of the year.

Q: What do you think about Gilead Sciences?

A: I don't really want to touch Gilead (GILD), or the entire sector, for that matter. We shouldn't be seeing such a poor performance at this point in the market. Health care has been dead for a long time, and you would have expected a rally based purely on fundamentals; they are delivering good earnings, it's just not reflected in the price action of the stocks. I think with no new money going into the market, there's nothing to push up other sectors; it's really become a "technology on and off" market. Health care doesn't fit anywhere in that world.

Q: Do you still like Nvidia?

A: I love Nvidia (NVDA). The chip sector still has another year to go. Nvidia has the high value-added product, and I'm looking for $300 dollars a share sometime this year/next year. The reason the stock hasn't really been moving is that it's over-owned; too many people know about the Nvidia story, which continues to go "gangbusters," so to speak. The chairman has also put out negative comments on short-term inventories, which have been a drag.

Q: Treasuries (TLT) are over 3%. Will they go over 3.5% by then end of this year?

A: I would say yes. Since that is only 50 basis points away from the current market, I would say it's a pretty good bet. So, if you get any good entry points you can do LEAPS going out to next year, betting that Treasuries will not only be below $116 by the end of the year, but they'll probably be below 110. And that would give you a very good high return LEAP with a yield of 50% in the next, say 8 months. By the way, if the Treasury yield rises to 4% that takes the (TLT) down to $98!

Q: Any chance General Electric will be acquired this year?

A: Absolutely not. General Electric (GE) worth far more if you break it up into individual pieces and sell them. Some parts are very profitable like jet engines and Baker Hughes, while other parts, like their medical insurance exposure, are awful.

Q: What do you see about the India ETF?

A: The one I follow is the PowerShares India Portfolio ETF (PIN) and we love it long term. Short term, they can take some pain with the rest of the emerging markets.

Q: What should I do with my January 2019 Gold calls?

A: I would sell them. It's not worth hanging on to here with too many other better things to do in stocks.

Q: Would you continue to hold ExxonMobile?

A: I would not. If you were lucky enough to get in at the bottom on ExxonMobile (XOM). I would be taking profits here. I'm not sure how long this energy rally will last, especially if the global economic slowdown continues.

Q: Is Freeport-McMoRan (FCX) a buy?

A: Yes, but only buy the dip in the recent range, so you don't get stopped out when the price goes against you. Commodities are the best performing asset class this year and that should continue.

Q: How high is oil (USO) headed?

A: I think we're probably peaking out short of $80 a barrel currently unless we get a major geopolitical event. Then it could go up to $100 very quickly and trigger a recession.

Q: Are you looking to buy the Volatility Index here?

A: Buy the next dip, but the trick with (VIX) is buying after it sits on a bottom for about five days. You also want to buy it when stocks (SPY) are at the top of a range, like yesterday.

Q: How long do you think the market will be range-bound for?

A: My bet is at least three months, and possibly four or five. We should start to anticipate the outcome of the midterm congressional elections in September/October; that's when you get your upside breakout.

Q: Is Gold (GLD) not worth buying since Bitcoin has taken over market share from Gold buyers?

A: Essentially, yes. That's probably why you're not getting these big spikes in Gold like you're used to. Instead, you're getting them in Bitcoin. Bitcoin is clearly stealing Gold's thunder. That's a major reason why we haven't been chasing Gold this year.

Q: After the emerging market sell-off, is it a good time to go in?

A: No, I think the emerging market (EEM) sell-off is being created by rising interest rates and a strong dollar. I don't see that ending anytime soon. In a year let's take another look in emerging markets. By then overnight Fed funds should be at 2.50% to 2.75%.

One has to be truly impressed with the selloff in biotech and health care stocks over the past year.

Since May, there were signs that life was returning to this beleaguered sector. Then Mylan decided to raise the prices of it's EpiPen by 400% and it was back to the penalty box.

Let?s gouge poor small children who may die horrible deaths if they can?t afford our product. That sounds like a great marketing and PR strategy. NOT!

Once the top performing sectors of 2015, they went from heroes to goats so fast, it made your head spin.

What I called ?The ATM Effect? kicked in big time.

That?s when frightened investors run for the sidelines and sell their best stocks to raise cash. After all, no one wants to sell other stocks for a loss and admit defeat, at least in front of their clients.

It?s not that the companies themselves were without blood on their hands. Valuations were getting, to use the polite term, ?stretched? after a torrid five-year run.

Gilead Sciences (GILD) soaring from $18 to $125?

Celgene (CELG) rocketing from $20 to $142?

It has been a performance for the ages.

If a financial advisor wasn?t in health care, chances are that he is driving for Uber in a bad neighborhood by now.

Then there was The Tweet That Ate Wall Street.

Presidential candidate Hillary Clinton made clear in a broadcast on September 21, 2015 that the health care industry would be target number one in her new administration.

Her move was triggered by an overnight 5000% price hike for a specialty HIV drug by a minor player in the industry.

Among the reforms she would implement are:

1) Give the government power to negotiate drug purchases with the industry collectively. 2) Allow Medicare to import drugs from abroad to encourage price competition (which I already do with my annual trips to Switzerland). 3) Ban drug companies from using government grants to pay for sales and advertising. 4) Set an out of pocket limit for drugs bought through Obamacare at $250 a month, thus ending customers? blank checks. 5) Set a 20% of revenue minimum which companies must spend on research and development.

She certainly got our attention.

Competition in the drug industry? Yikes! Not what the shareholders had in mind.

Raise your hand if you think Americans aren?t paying enough for their prescription drugs.

Yes, I thought so.

Drug company CEOs aren?t helping their case by flying to press conferences to complain about the proposals in brand new $65 million Cessna G-5?s.

And that Mylan CEO, Heather Bresch? She took home $18 million last year, and she?s just a kid.

Here?s the key issue for health care and biotech for investors. It all about politics.

Even if Hillary does get elected, the government is likely to remain gridlocked for another 4-8 years. The Democrats will almost certainly retake the Senate in 2016, thanks to a highly favorable calendar, and keep it for at least two years.

But the heavily gerrymandered House is another story.

With the current districting map, the Democrats would have to win 57% of the national vote for them to regain a majority in both houses.

That is a feat even Barack Obama could not pull off in 2008, when a perfect storm in favor of his party blew in.

A Hillary appointed liberal Supreme Court could bring an end to gerrymandering, but that is a multiyear process. Texas hasn?t had a legal districting map since 2000.

Even with Democratic control of congress, Hillary won?t get everything she wants.

Remember, Obamacare passed by one vote only after a year of cantankerous infighting, and then, only when a member changed parties (Pennsylvanian Arlen Spector).

That means few, if any, Clinton proposals will ever make it into law. If they do, they will be severely watered down and subject to the usual horse-trading and quid pro quos.

Beyond what she can accomplish through executive order, her election may be largely symbolic.

Therefore, the biotech and health care stocks are a screaming ?BUY? at these levels, provided you ignore Mylan (MYL), now the poster boy for corporate greed.

It?s a political call I can only make after spending years in the White House and a half century following presidential elections.

It?s easy to understand why these stocks were so popular, and are found brimming to overflowing in client portfolios and personal 401ks and IRAs.

We are just entering a Golden Age for biotech and health care.

Profit growth for many firms is exceeding 20% a year. Hyper accelerating biotechnology is rapidly bringing to market dozens of billion dollar earning drugs that were, until recently, considered in the realm of science fiction.

And we have only just gotten started. Cures for cancer, heart disease, arthritis, diabetes, AIDS, and dementia? You can take your pick.

Most biotech and health care stocks have given up all of their 2015 gains. Here is a chance to hoover up the fastest growing companies in the US at 2014 prices.

If you missed biotech and health care the first time around, you?ve just been given a second chance at the brass ring.

Here?s a list of five top quality names to get your feet wet:

Gilead Sciences (GILD) ? Has the world?s top hepatitis cure, which it sells for $80,000 per treatment. For a full report, see the next piece below.

Celgene (CELG) ? A biotech firm that specializes in cancer cures (thalidomide) and inflammatory diseases. It also produces Ritalin for the treatment of ADHD.

Allergan (AGN) ? Has the world?s third largest low cost generic drug business. In addition, it has built a major portfolio of drug therapies through more than two dozen acquisitions over the last decade.

Regeneron (REGN) ? Already has a great anti-inflammatory drug, and is about to market a blockbuster anti cholesterol drug that will substantially reduce heart disease.

HCA Holdings (HCA) ? Is the world?s largest operator of for profit health care facilities in the world.

If you want a lower risk, more diversified play in the area, you can buy the Health Care Select Sector SPDR (XLV). Please note that a basket of stocks is going to deliver a fraction of the volatility of single stocks.

Therefore, we have to be more aggressive with our positioning to make any money, picking call option strikes that are closer to the money.

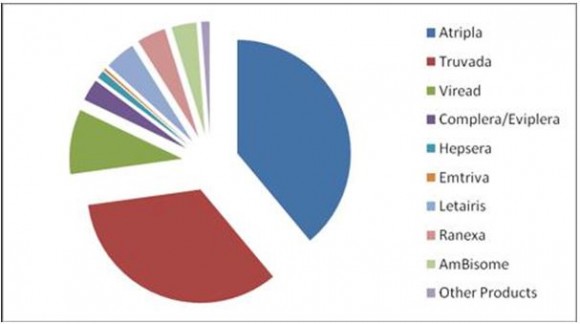

Johnson and Johnson (JJ) is the largest holding in the (XLV), with a 12.8% weighting, while Gilead Sciences (GILD) is the fourth, with a 5.1% share. For a list of the largest components of this ETF, please click: https://www.spdrs.com/product/fund.seam?ticker=XLV.

Their largest holding is Biogen (BIIB), followed by Gilead Sciences (GILD), Celgene (CELG), Amgen (AMGN), and Regeneron Pharmaceutical (REGN).

I?ll be shooting out Trade Alerts on biotech and health care names as soon as I think the coast is clear.

Until then, enjoy the ride!

Say You Were A Biotech Investor, Did You?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/EpiPen-e1472773044918.jpg375400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-09-02 01:06:052016-09-02 01:06:05Biotech and Health Care Stocks to Buy at the Bottom

I am going to continue to use this correction in the stock market as an opportunity to put new names in front of you for inclusion in your investment portfolio.

That way, when the markets turn, you can strike with the speed of a rattlesnake in returning to a ?RISK ON? posture.

Major turnarounds are not the time to engage in deep, fundamental research. It is when you should be pulling the trigger on Trade Alerts, which you have wisely spent time lining up.

This brings me back to my three core sectors for long-term investment, technology, health care, and energy. For a four cyclical play, you can add the financials as an interest rate play.

Which brings me to one of my perennial favorites, Gilead Sciences (GILD). Long-term readers will recall this big momentum name, which I first recommended last December at $75 a share. It hit $125 in June, last week, and could fly as high as $200 in 2016.

Obamacare is proving to by one of the greatest windfalls in the history of the health care industry. More than 45 million new individuals now enjoy government guaranteed payments for health care services for the first time. In addition, millions more are signing up for private insurance.

One of the cleanest shots at this new profit stream is Gilead Sciences. The ticker symbol seems so appropriate for this new Golden Age for the health care industry.

(GILD) is an American biotechnology company that discovers, develops and commercializes treatments for a range of different diseases. The California based firm initially concentrated on antiviral drugs to treat patients infected with HIV, hepatitis B, or influenza.

In 2006, Gilead acquired two companies that were developing drugs to treat patients with pulmonary diseases.

These are all expected to be huge growth areas in the future, and the company has become a favorite of hedge fund traders. Both the shares and the sector have been on fire all year.

Don?t rush out and buy (GILD) today. Rather, I?d wait until the last of the sellers get flushed out in this correction, which will probably not be until well into October.

Take a look at the charts below, and they suggest that the S&P 500 could reach as low as 1,976, or down another 160 handles from here.

That will give us another top to bottom pullback of 12.52%, which certainly qualifies as a healthy correction. This will be the time to load the boat with (GILD).

Keep close tabs on your text message service and email, and I?ll let you know when it is time to lay your cajones on the line once more.

Yes, It?s $1,000 a Pill

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/Pills-e1411767040932.jpg226400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-01 01:06:142015-10-01 01:06:14Keep Gilead Sciences on Your Radar

Basking in the glow of the spectacular 22% profit by the Trade Alert Service so far in 2015, I sat down on a rock on a high mountain the other day to try and figure out what happened.

The last time I saw a move this healthy was back in 2013, when I clocked a 68% gain for the year.

During the 1990?s, we saw a perfect trifecta of the Internet going mainstream, cheap graphical user interface enabled personal computers, and an easy to use World Wide Web that conspired to create a Dotcom boom and send risk assets everywhere ballistic.

Sure, the advent of cheap domestic energy unleashed by the fracking and horizontal drilling of natural gas is a game changer of similar magnitude.

But that isn?t enough to suddenly convert every investor from a pessimist to an optimist, a Cassandra to a Pollyanna, or a bear to a bull.

So what else is helping to send stocks ever Northward?

Fortunately, I brought along an abacus with me to my high altitude retreat. So I ran a few numbers.

Approximately 18% of US GDP is derived from the health care industry in some form or another. In Europe they spend only 8%, live longer and certainly eat better food (I spent two months field testing it last summer).

So what happens when America?s Affordable Care Act, otherwise known as Obamacare, brings our spending down to European levels? The savings would amount to 10% of GDP, or $1.6 trillion. That is a handsome amount of change.

Where would all of this money go? The short answer is: to you and me. To be precise, I get half, and you get half, which works out to $800 billion for each of us, per year.

The reality is a little more complicated than that. We are not going to get our new found wealth in unmarked bills stuffed in a duffle bag left at a dead drop in the middle of the night.

Rather, the payoff will come in an indirect form. We will get better quality health care for less money, and more of us will get it, some 48 million to be precise.

Oh, and we get to live longer too.

What are we going to do with this windfall? Buy stocks, and lots of them. At least that?s what the stock market thinks. Hence, the ballistic move in equities. This year could be just as good.

In fact, we will be buying a lot of everything, which is why the auto industry is on fire, real estate is recovering, yet the bond market hasn?t crashed.

This amount of money hitting the financial system over the coming decade could well be the appetizer to an investment ?Golden Age? during the 2020?s.

This is fabulous news for asset owners of all stripes, and pretty good for everyone else as well. Companies with rising share prices are much more likely to hire and expand capital investment than those with falling ones, raising standards of living.

The way this happens is what makes Obamacare so interesting, unlike the purely government sponsored plans now in operation in Europe and Asia. It does this with a heavy reliance on the private sector to unleash free market capitalism on the health care industry for the first time in its history.

At last, they will be thrown into the merciless pit of dog eat dog, cutthroat competition where the rest of us have already been living for quite some time. They will be the losers, and we will be the winners.

I have been studying health care for about 40 years now. I was once destined to become a medical researcher at the Center for Disease in Atlanta. But the Defense Department found out I was pretty good with numbers, and I found myself in a bleak part of Northern Nevada now known as Area 51.

When improving relations with the Soviet Union wound things down there and all the aliens went home, there was nowhere else for me to go but the stock market. Suffice it to say, I still know which end of a test tube to hold up.

Health care is the last 19th century industry that operates in this country (except possibly for coal mining). It is fragmented into local monopolies spread amongst the country?s 3,141 counties.

I haven?t had health insurance myself for seven years. After paying on a Blue Cross of California policy for 20 years, they suddenly cancelled my policy claiming an alleged pre existing condition. My real pre existing condition was that I was a 55-year-old white male, and was not a great risk.

Since I was paying out of pocket for every trip to the doctor, I became an expert on what things cost. The first thing that I learned is that no one in a doctor?s office knows what anything costs. They deliberately don?t know. That way they can feign innocence when you get hit with a whopping big bill.

It was only with the greatest persistence that I was able to chase down the actual dollar cost of tests and procedures. Needless to say, my health care providers considered me a nut case and a pain in the ass and kindly offered a referral to a mental health professional. Some actually refused me care.

This is the land of the $100 plastic hypodermic needle, the $300 paper gown, and the $1,000 saline drip (its salt water). MRI Scans can cost $6,000, or $1,500 at the hospital down the street.

In fact, I?ve had friends show up for procedures at hospitals with a $3 gown they bought on Ebay, but were still forced to use the identical $300 version.

This is why the wealthiest guy in the county is often the one who runs the local hospital, or sells specialized prescribed treatments and procedures, to be reimbursed by the government.

From 1995 to 2012, dermatologists saw a 50% increase in annual incomes to an average $471,000 while most of America saw a steady decline in real take home pay. Oncologists and gastroenterologists did as well. This is especially true in rural parts of the country where there is a chronic shortage of doctors. Competition is anathema to these people.

What broke the health care system in this country is that there was a total absence of cost control, but an unlimited ability to get paid. If you?re having a heart attack, you don?t shop around for the hospital offering the best deal on surgery that week, as we might for a new set of tires (go to Costco) or a new computer.

Being the savvy consumers that we have become, if we don?t like the prices down at the mall we just go online. That?s tough to do with health care.

With insurers or the government picking up the tab whatever the cost, there was no incentive to do so anyway. Doctors excessively ordered tests to protect themselves from lawsuits, thanks to a tort system run amuck.

Drug companies kept inventing new diseases (do any of you male readers suffer from ?low T??). Indulgent lifestyles assured that ever-rising numbers of us got sick, driving prices skyward.

By creating national exchanges selling plain vanilla policies and setting rigorous standards on what they will pay for (?death panels? to opponents), American health care costs are now falling for the first time in history. 2013 saw the first year on year fall on record. This is only the beginning of that $1.6 trillion plunge in costs.

No one really knows what the marginal cost of an MRI scan is. But if you count the capital cost of buying a new $1.4 million machine, deduct the fee the specialist to read the scan, the $60,000 annual salary of the technician to run it, along with maintenance and depreciation, and I bet you get a number a hell of a lot less than $6,000. We are soon going to find out what the marginal cost really is.

This is why opposition to Obamacare has been so violent and vehement five years after it became law. Those who have been feeding off of the gravy train for so long will do anything to protect it. $1.6 trillion buys a lot of lobbyists in Washington DC. <

br /> Most opposing Obamacare in the media are being paid to do so. Ask them exact details about exactly why it is so bad and they either mumble some lame ideological explanation or go mute.

States that support Obamacare and set up their own exchanges, like California, New York, and Kentucky, are seeing dramatic reductions in the cost of health care costs and insurance, up to 50% in some cases. Those that oppose it, such as Texas, are not.

The great irony in all of this is that the states opposing Obamacare need it the most. The 13 states of the old southern Confederacy suffer the worst health in the country.

Take three states out of the national averages, Georgia, Mississippi and Alabama, and the average male life span jumps from 78 to 82. I?m told they eat pure lard down there, not exactly a health food.

So Obamacare is basically a giant federal program that shifts money away from the two coasts toward the South and Midwest, or out of blue states into red ones. This is the same pattern for all large government programs. Why they are against Obamacare one can only imagine, except possibly the name.

I have been pointing out to the administration for years that they have greatly underestimated the long-term impacts of Obamacare on the economy, most of which are positive.

This has led them to unintentionally undersell the program. The impact on the world?s large economy is so enormous that it was impossible to foresee all of the unintended consequences. The only way to find out was to do it.

I?ll give you a couple of examples. Take the ?Obama lied? issue, where the president promised voters they could keep their existing doctors and insurance.

By setting minimal coverage and care standards the government put out of business the ?junk insurance? industry, which provides questionable policies with deductibles of $8,000 or more, low lifetime maximums, and boots you off your coverage as soon as you sneeze.

They had a bad habit of taking in your premium income and disappearing as soon as you made a major claim, with denials at some companies running as high as 50%.

Banning these rip-offs from the industry is all well and good. But nobody knew there were so many such polices, over 5 million. It turns out that no research had been done on this ugly little backwater, as it was purely a private sector enterprise. Then the cancellation letters all went out at once, to the shock and surprise of everyone.

When you are living paycheck to paycheck, about 20% of the country, even $100 a month is too much to spend. Many just don?t like doctors or hospitals and will only sign up after they are seriously ill, probably at the prompting of a social worker. Then they go to the emergency room and don?t pay.

I can tell you from my journalist days that 40% of the population doesn?t read newspapers at all, either the online or hard copy kind. Unless something appears on ESPN or the Golf Channel, they have no clue that it exists. There are those who still can?t operate a computer, as unbelievable as that may seem in the 21st century.

Then there was the website fiasco, the most easily preventable error in the entire rollout. I would bet big money that the former Health and Services Director, Kathleen Sebelius, has never built her own website.

For her, I highly recommend Websites for Dummies (click here for Amazon), which helped me get Mad Hedge Fund Trader off the ground seven years ago.

I was outraged when I heard that the lead contract for the construction of the website was given to a Canadian firm. I raised my hand and said ?Hey, we out here in Silicon Valley know how to build websites too.?

They should have just given the whole thing to Google (GOOG). But that would have raised conflict of interest questions, as founders Larry Page and Sergei Brin were two of Obama?s largest donors.

Corporations will get, thankfully, out of the health care business completely, offloading coverage to Obamacare as fast as they can. Small companies are already doing this in large numbers because workers can get better coverage for less money. This will level the playing field with foreign competitors for the first time in more than half a century, whose own governments cover the health care costs of their employees for free.

Those in the hedge fund, banking and oil industry luxuriating in $30,000 a year formerly tax free Cadillac insurance plans now have to pay ordinary income tax on benefits worth more than $10,000 a year. With most of the tax subsidy gone, there is little reason for employers to continue with these perks.

What is the bottom line for the shareholders in all of this? A substantial reduction in costs that drops straight to the bottom line, creating surging profits and stock prices. That works for me!

All of the above is a major reason why health care has been a major plank in my trading portfolio for the past two years, and may remain so for the next decade.

Followers of my Trade Alert Service cashed in on my long in the Health Care Sector Select SPDR ETF (XLV) and hepatitis drug manufacturer Gilead Sciences (GILD) multiple times. Those who took my advice joyfully watched them run away to the upside.

Expect this to be a recurring theme in my equity coverage. The SPDR S&P Pharmaceutical Index (XPH), Celgene (CELG), Biogen (BIIB), and the SPDR S&P Biotech Index (XBI) are also on the menu and looking tasty.

Every country in the world that has implemented national heath care has been successful. We are the smartest people in the world, so there is no reason we can?t make it work as well, if not better. Only political obstacles stand in the way.

It could well be that the stock markets are the first to see these momentous changes, far ahead of we mere mortals. Such is the wisdom of markets. So far, your investment portfolio agrees.

It will be at least a decade before we can judge the results of Obamacare, it is so vast and complex an undertaking. Up for grabs are individual markets for over 10,000 different treatments and services. It is far too early to call it a failure or a success. In any case, the earliest it can be repealed is 2025, after Hillary Clinton completes her second term as president. So get used to it.

What about my own insurance? I am waiting for my Medicare to kick in, which is only a year off. Until then, they are going to have to come after me with handcuffs and a taser. I bet many other Americans plan on doing the same.

By then, the website should be working and the costs brought in line with reality. Then I?ll buy the cheapest possible policy, the popular ?Bronze? plan, because I never get sick.

Who has time for doctors?

After all, who needs health insurance if they are going to live forever?

They Said This Would Be So Easy

https://www.madhedgefundtrader.com/wp-content/uploads/2014/01/Obama.jpg312472Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-04-29 09:26:222015-04-29 09:26:22How Obamacare Will Boost Your Portfolio

I am sitting here at the Lone Eagle Grill in Incline Village, Nevada, enjoying a rare solo lunch. No one is asking me about the future of interest rates, if there is any gold inside Fort Knox or if the aliens really landed at Roswell, New Mexico.

My table overlooks majestic Lake Tahoe, and a brace of mallard ducks has just skidded across the smooth surface for a landing.

My big score last night was coming across a wild bobcat, the first I had ever seen in the Sierras. After cautiously studying me for a minute with his bright yellow glowing eyes, he scampered up the mountain.

My pastrami sandwich is cooked to perfection, and would give Manhattan?s best culinary effort a run for its money. In fact, I have enough food here for two entire meals. Bring on the doggie bag!

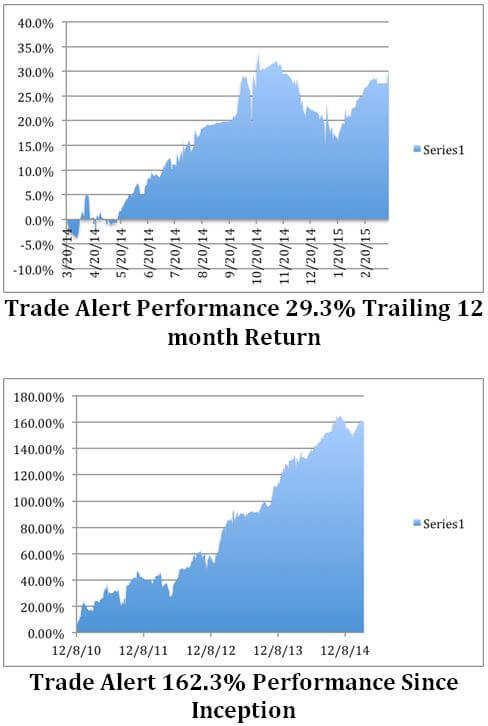

After surviving a meat grinder of a January, putting the pedal to the metal in February, and dodging the raindrops of March, the model-trading portfolio of the Mad Hedge Fund Trader has posted a year-to-date gain of 10%.

We have generated profits for followers every month this year, and are now a mere 4.75% short of a new all time performance high.

Mad Day Trader, Jim Parker, and myself have performed like tag team wrestlers, delivering winners for our paid subscribers one right after the other. Some 12 out of my last 14 Trade Alerts have been profitable.

I managed to nail the collapse in the euro (FXE), (EUO) big time, backing that up with profitable long positions in the S&P 500 (SPY), the Russell 2000, and Gilead Sciences (GILD).

When the markets turned jittery, I coined it with short positions in Alcoa (AA), QUALCOM (QCOM) and AT&T (T).

Only a premature long in oil (LINE) and a short in Treasuries (TBT) have scarred my numbers so far this year.

Jim has been on an absolute hot streak in 2015, shaking the Bull Run in biotechs for all it is worth (ZIOP), (THRX), (ZTS) and executing some perfectly times shorts in oil (USO).

This is compared to the miserable performance of the Dow Average, which is up a pitiful +2% during the same period.

The nearly four and a half year return of my Trade Alert service is now at an amazing 162.4%, compared to a far more modest increase for the Dow Average during the same period of only 51%.

That brings my averaged annualized return up to 38.2%. Not bad in this zero interest rate world. It appears better to take on some risk and reach for capital gains and trading profits, than surrender to the paltry fixed income yields out there.

This has been the profit since my groundbreaking trade mentoring service was first launched in 2010. Thousands of followers now earn a full time living solely from my Trade Alerts, a development of which I am immensely proud.

What saved my bacon this month was my instant and accurate decoding of Fed chairman Janet Yellen?s cryptic comments on the future of possible interest rate hikes, or the lack thereof.

We got to eat our ?patience? and have it too.

Wall Street gets so greedy, and takes out so much money for itself, there is now nothing left for the individual investor any more. They literally kill the goose that lays the golden egg.

The Mad Hedge Fund Trader seeks to address this imbalance and level the playing field for the average Joe. Looking at the testimonials that come in every day, I?d say we?ve accomplished that goal.

It has all been a vindication of the trading and investment strategy that I have been preaching to followers for the past seven years.

Quite a few followers were able to move fast enough to cash in on my trading recommendations. To read the plaudits yourself, please go to my testimonials page by clicking here.

Watch this space, because the crack team at Mad Hedge Fund Trader has more new products and services cooking in the oven. You?ll hear about them as soon as they are out of beta testing.

Our business is booming, so I am plowing profits back in to enhance our added value for you.

The coming year promises to deliver a harvest of new trading opportunities. The big driver will be a global synchronized recovery that promises to drive markets into the stratosphere by the end of 2015.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011, 14.87% in 2012, and 67.45% in 2013, and 30.3% in 2014.

Our flagship product,?Mad Hedge Fund Trader PRO, costs $4,500 a year. It includes?Global Trading Dispatch(my trade alert service and daily newsletter). You get a real-time trading portfolio, an enormous research database and live biweekly strategy webinars. You also get Jim Parker?s?Mad Day Trader?service and?The Opening Bell with Jim Parker.

To subscribe, please go to my website, ?www.madhedgefundtrader.com, click on the ?Memberships? located on the second row of tabs.

By the way, those of you who ran up huge profits with your euro shorts in January and February, and the overnight killing I scored with the Russell 2000 (IWM) this week, you all owe me new testimonials.

Ship em in!

Oh, and buy the way, there is no gold in Fort Knox. That is why Nixon took us off the gold standard in 1973. And the aliens did land at Roswell. Where do you think my iPhone and Tesla came from?

Looking for the Next Great Trade

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/John-Thomas5.jpg398393Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-03-23 01:03:592015-03-23 01:03:59Mad Hedge Fund Trader Hits 10% Profit in 2015

We have several options positions that expire on Friday, and I just want to explain to the newbies how to best maximize their profits.

These include:

The Currency Shares Japanese Yen Trust (FXY) February $84-$87 vertical bear put spread

The Gilead Sciences (GILD) February $87.50-$92.50 vertical bull call spread

The S&P 500 (SPY) February $199-$202 vertical bull call spread

My bets that (GILD) and the (SPY) would rise, and that the (FXY) would fall during January and February proved dead on accurate. We got a further kicker with the two stock positions in that we captured a dramatic plunge in volatility (VIX).

Provided that some 9/11 type event doesn?t occur today, all three positions should expire at their maximum profit point. In that case, your profits on these positions will amount to 13% for the (FXY), 19% for (GILD) and 20% for the (SPY).

This will bring us a fabulous 5.58% profit so far for February, and a market beating 6.11% for year-to-date 2015.

Many of you have already emailed me asking what to do with these winning positions. The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck and pat yourself on the back for a job well done. You don?t have to do anything.

Your broker (are they still called that?) will automatically use your long put position to cover the short put position, cancelling out the total holding. Ditto for the call spreads. The profit will be credited to your account on Monday morning, and he margin freed up.

If you don?t see the cash show up in you account on Monday, get on the blower immediately. Although the expiration process is now supposed to be fully automated, occasionally mistakes do occur. Better to sort out any confusion before losses ensue.

I don?t usually run positions into expiration like this, preferring to take profits two weeks ahead of time, as the risk reward is no longer that favorable.

But we have a ton of cash right now, and I don?t see any other great entry points for the moment. Better to keep the cash working and duck the double commissions. This time being a pig paid off handsomely.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. Keep in mind that the liquidity in the options market disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration. This is known in the trade as the ?expiration risk.?

One way or the other, I?m sure you?ll do OK, as long as I am looking over your shoulder, as I will be.

This expiration will leave me with a very rare 100% cash position. I am going to hang back and wait for good entry points before jumping back in. It?s all about getting that ?buy low, sell high? thing going again.

There are already interesting trades setting up in bonds (TLT), the (SPY), the Russell 2000 (IWM), NASDAQ (QQQ), solar stocks (SCTY), oil (USO), and gold (GLD).

The currencies seem to have gone dead for the time being, so I?ll stay away.

Well done, and on to the next trade.

Pat Yourself on the Back

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Pat-on-the-back-e1424375419249.jpg259400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-20 01:04:322015-02-20 01:04:32A Note on the Friday Options Expiration

Long-term readers of this letter have prospered mightily from my addiction to biotech stocks in recent years, one of the most reliably top performing sectors in the stock market.

But have we visited the well one time too many times? Is biotech turning into a bubble that will eventually deliver the same grievous outcome of other past bubbles?

Not yet.

Still, one has to ask the question. No less a figure than Federal Reserve governor Janet Yellen has indicated that she thought valuations in the biotech sector were getting ?substantially stretched.? The Fed doesn?t single out stocks for commentary very often.

Biotech certainly has been a money-spinner for followers of my top performing Trade Alert service, which delivered a 30.5% profit in 2014.

Readers made three round trips in hepatitis C drug developer Gilead Sciences (GILD) in the past four months, adding 5.77% to the value of their portfolios. I believe the company?s blockbuster drug will become the most profitable in history. So do a lot of others.

Longer-term investors bought the Biotech iShares ETF (IBB) on my advice, which gained an impressive 45% last year, and is still rising.

However, biotech has long been a hedge fund favorite.

That means many shareholders are only dating these stocks and are not married to them. The hot money regularly flows in and out, giving the sector more than double the volatility of the main market. A 10% correction in any other stock is worth at least 25% in biotech.

This also makes biotech stocks great to buy on a dip. My last foray into (GILD) occurred after cautious guidance took the shares down a heart stopping 10% in a single day.

This is a great example of how unusually sensitive biotech stocks are to headline risk. I?ve ridden stocks to tremendous heights, watching them pour billions into a single treatment, only to see them crash and burn on failed stage three trials.

That is just the nature of their business. It?s all about all or nothing bets.

It?s just a matter of time before one of the major companies gets stuck with a hickey like this, flushing billions down the drain. That could herald a generalized sector selloff that could last months, or even years.

Biotech is a high-risk sector that should only be held within a well diversified portfolio. You may notice that in the Mad Hedge Fund Trader?s model trading portfolio I never have more than 10% in biotech at any given time. I figure I could handle a total blow up and lose the whole 10% and still stay in business.

When I speak at conferences, strategy luncheons and on TV, I tell listeners of my lazy man?s guide to long-term investment. Only follow three sectors, technology, biotech and energy, and ignore the other 97. You?ll save yourself a lot of time reading pointless research.

Biotech currently accounts for a mere 1% of US GDP. It is on its way to 20%, about where technology is today. That means that a disproportionately large share of earnings growth will spring from biotech over the coming decades.

One way to protect yourself is to stick with the big caps, which are undervalued relative to the sector, and are expected to haul in 20% earnings growth this year.

Many smaller companies prices are assuming a total certainty of the success of their drugs. The reality is that this only happens about half the time.

If you do go with small caps, I would take a venture capital approach. Buy a dozen with the expectation that many will go under, a couple do OK, and one goes through the roof. Never put all your eggs in one basket.

It also helps that you have someone with a scientific background making your picks, like me. Because drug companies promise such amazing results, like curing cancer, the sector has always been prone to hype and over promotion. I never met I biotech CEO who didn?t believe his company was about to deliver the next panacea, taking his shares up tenfold.

One plus for biotech is that it has unusually strong patent protection, which usually extends out 20 years for new products. There are not a lot of Chinese companies that can imitate their drugs.

That means earnings can be predicted far into the future, and are largely immune from the economic cycle. If you?re sick, you want to get cured regardless of whether the GDP is growing or shrinking, or whether interest rates are low or high.

Make sure that your investments have plenty of new developments in the pipeline. Expiring patents on past winners with no replacements can spell certain death for a stock price.

Publicly listed drug companies are now venturing into research fields that were only science fiction when I was in the lab 45 years go. ?Gene editing? whereby genes can be repaired, edited and then turned on and off at will, is now becoming a burgeoning new science.

It promises to cure the whole range of human maladies, including heart disease, cancer, obesity and a whole range of degenerative diseases (including some of mine).

Expect to hear a lot more about TALENs (transcription activator-like effector nucleases) and CRISPR (clustered regular interspaced short palindromic repeats). You heard it here first.

What is truly fascinating is that hybrid computer science/biochemical scientists are now taking algorithms developed y the National Security Agency hackers and using them to decode human DNA. (I hope I?m not speaking too much out of school here.)

Gene editing is the natural outcome of the discovery of recombinant DNA technology developed during the 1970?s by Paul Berg, Herbert Boyer, and Stanley Cohen, all early heroes of mine.

Since none were the equity participants of private companies, the initial rewards for the breakthrough were minimal. I remember that one received a new surfboard for his efforts.

Berg went on to found Genentech (GENE) in 1977 and got rich. If I hadn?t gone into the stock market, that is almost certainly where I would have ended up.

How things have changed.

The short answer here is that biotech does have further to run. A lot further.

The rate of innovation of biotechnology is accelerating so fast that it will continue to spew out fantastic investment opportunities for the rest of your lives. So expect to receive many more Trade Alerts in this area in the years to come.

But it is definitely an ?E? ticket ride. So fasten your seatbelt on your path to riches.

As for me, I?m thrilled that I got to live so long to see this stuff happen. At times, it was a close run race.

This One Looks Like a Winner

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Scientist-Bio-Lab-e1424187891662.jpg265400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-17 10:52:212015-02-17 10:52:21How Far Will Biotech Run?

Those of you who are paid subscribers have the good fortune of waking up to a bounty of riches this morning.

Both Gilead Sciences (GILD) and the Japanese yen (FXY) have made gap moves in your favor overnight. Your long position in (GILD) saw a nice little $2 pop to the upside, and your short in the (FXY) just got whacked in the knees, down a full $1.

As a result, the Trade Alert model-trading portfolio is now up +4% on the year. It?s not exactly knocking the ball out of the park, but should be enough to keep you in fine Chardonnay for the rest of the year. And compared to most other suffering, money losing hedge fund traders, it is more than adequate.

If you followed my advice, your existing positions in these two securities are now close to their maximum expiration value. However, as is so often the case with deep in the money options with only days to expiration, they have become highly illiquid.

For example, the February (FXY) $87 puts are trading at $6.00-$6.90 on the screen, against an intrinsic value of $6.22 ($87 - $80.78 in the cash market = $6.22). So a market order to sell would most likely wipe out your entire profit.

So I am going to run my positions into expiration, given that we only have six trading days to go. These are my last two positions, so I also have an excess of dormant, unused cash.

I am trying to maintain some discipline here and restrict myself to only buying low and selling high. I know this sounds revolutionary, but it should work. Like you, I am not paid according to the volume of Trade Alerts I issue, only on their end results.

However, this market has shown a pronounced tendency to Giveth, and then abruptly Taketh Away. So, if you don?t want to wait until next week to collect your winnings and free up margin, you can put in some high limit orders to sell.

The Gilead Sciences (GILD) February, 2015 $35-$37 in-the-money bear put spread has an intrinsic value here of $5.00, so you can probably get a $4.95 offer done.

The Currency Shares Japanese Yen Trust (FXY) February, 2015 $84-$87 in-the-money vertical bear put spread has an intrinsic of $3.00, so $2.97 probably gets executed. If it doesn?t just re-enter the order tomorrow and try again, or lower your limit by a penny.

Congratulations, and on to the next one.

For me that is going to be an opportunistic short term long position in the S&P 500 (SPY) February 20 expiring options.

It?s rare to see an options spread with only six trading days to expiration offering so much money. But with the Volatility Index (VIX) holding in at a lofty 17.70%, we can take in a nearly 2% profit with a near strike that is a full 2% out of the money.

That means the S&P 500 (SPY) has to drop a hefty $4.60 by Friday next week for you to lose money on this position.

I know that?s not impossible in this uncertain environment. But I think that we are in nothing more than a long, sideways correction in a major long-term major uptrend, so this should work.

Traders are confused and disoriented, thanks to the massive one-way moves in oil and bonds in recent months. Many long tested models have blown up.

So rather than continue to hemorrhage money, they are giving up. The large intraday moves and sky-high volatility may continue. But I don?t expect any large sustainable net moves in the near future.

You are going to have to be especially vigilant with your stop loss on this (SPY) position, which I shall put at $202, as there is so little time left to expiration.

The 50 day moving average at $204 should give us plenty of support on the downside, and enough time to make it to expiration and get out whole.

Since this is a big contract and fairly close to the money, there should be plenty of liquidity right up to the last day, if we have to stop out.

Time for another Dose of Gilead Sciences

It?s All Over for the Yen

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Sovaldi-Pills.jpg298367Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-12 01:05:582015-02-12 01:05:58Hitting Two Home Runs in One Day

This is a stock that could double by the end of 2015. Buy a great performing stock in the top performing sector on a 10% dip.

The stock has over reacted to an earnings report that was fantastic; but carried conservative forward guidance, based on expected future pricing pressure on its blockbuster Hepatitis C drugs, Sovaldi and Harvini.

I am giving a nod to the current high risk, high volatility environment and being very cautious here buy going with strike prices for the options that are well below the 200-day moving average. A very short, 11 trading day expiration gives us some extra protection.

This position should be able to weather some pretty fierce storms.

If you want to be more aggressive and take a longer view, buy the (GILD) April, 2015 $110 calls at $2.20 or better. If we break to a new all time high by the April 17 expiration, as I expect, you could score a 3-5 bagger for these options.

If you don?t do options, just buy the shares and sit on them for the rest of the year.

I spoke to a friend of mine who works for a health care venture capital firm, and I thought I?d pass through a few tidbits.

Gilead Sciences (GILD) is basking in the glow of the most profitable drug launch in history. Its treatment for hepatitis C, launched in 2013, inhibits the RNA polymerase that the hepatitis C virus (HCV) uses to replicate its RNA. It traders? parlance, it kills the bug.

(GILD) has taken in $5.7 billion in sales of this drug during the first half of 2014, and could sell as much as $10-$12 billion for the full year.

The drug is so revolutionary, that it on the scale of medical miracles of decades past, such as Salk vaccine immunizations for polio and penicillin treatments for bacterial infections. So far, Gilead has cured a breathtaking 90% of patients.

Now the company is using various drug combinations that produce even higher success rates with fewer side effects, and may be expended to treat other life threatening diseases. These could take Hepatitis C drug sales as high as $15-$18 billion in 2015.

A big controversy has been its immense cost, which works out to $84,000-$135,000 per patient. This has become a bigger issue with the advent of Obamacare, now that the government is picking up much of the tab.

But, that?s a bargain compared to full treatment of the disease, which can run as high as $350,000 per patient. That is, unless you don?t care if you die.

Partly in response to these complaints, the company is making the drug available at deep discounts in 91 emerging nations that account for 50% of all Hepatitis C cases globally. What it loses on margins there it will make back in volume.

With any luck, we may see hepatitis C wiped out in my lifetime, as I have already seen with smallpox (I saw some of the last few live cases in kids in Nepal in 1976).

All of this makes the stock appear a bargain at its current $99.01 price. At a multiple of a subterranean 11X earnings, the stock should hit $140 next year.

You all know that health care is one of my three core industries to bet on for the long term (there others are energy and technology).

The short-term driver of the share price for (GILD) is obviously whether the health care sector is in, or out of vogue. But for the long term Gilead looks like a good bet to me.

And I don?t even have hepatitis, or Ebola.

Time for Another Dose of Gilead Sciences

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Sovaldi-Pills.jpg298367Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-05 09:31:422015-02-05 09:31:42Going Back Into Gilead Sciences

When is the Mad Hedge Fund Trader a genius, and when is he a complete moron?

That is the question readers have to ask themselves whenever their smart phones ping, and a new Trade Alert appears on their screens.

I have to confess that I wonder myself sometimes.

So I thought I would run my 2014 numbers to find out when I was a hero, and when I was a goat.

The good news is that I was a hero most of the time, and a goat only occasionally. Here is the cumulative profit and loss for the 75 Trade Alerts that I closed during calendar 2014, listed by asset class.

Profit by Asset Class

Foreign Exchange 15.12% Equities 12.52% Fixed Income 7.28% Energy 1.4% Volatility -1.68%

Total 37.64%

Foreign exchange trading was my big winner for 2014, accounting for nearly half of my profits. My most successful trade of the year was in my short position in the Euro (FXE), (EUO).

I piled on a double position at the end of July, just as it became apparent that the beleaguered European currency was about to break out of a multi month sideway move into a pronounced new downtrend.

I then kept rolling the strikes down every month. Those who bought the short Euro 2X ETF (EUO) made even more.

The fundamentals for the Euro were bad and steadily worsening. It helped that I was there for two months during the summer and could clearly see how grotesquely overvalued the currency was. $20 for a cappuccino? Mama mia!

Nothing beats on the ground, first hand research.

Stocks generated another third of my profits last year and also accounted for my largest number of Trade Alerts.

I correctly identified technology and biotech as the lead sectors for the year, weaving in and out of Apple (AAPL) and Gilead Sciences (GILD) on many occasions. I also nailed the recovery of the US auto industry (GM), (F).

I safely stayed away from the energy sector until the very end of the year, when oil hit the $50 handle. I also prudently avoided commodities like the plague.

Unfortunately, I was wrong on the bond market for the entire year. That didn?t stop me from making money on the short side on price spikes, with fixed income chipping a healthy 7.28% into the kitty.

It was only at the end of the year, when the prices accelerated their northward trend that they started to cost me money. My saving grace was that I kept positions small throughout, doubling up on a single occasion and then coming right back out.

My one trade in the energy sector for the year was on the short side, in natural gas (UNG), selling the simple molecule at the $5.50 level. With gas now plumbing the depths at $2.90, I should have followed up with more Trade Alerts. But hey, a 1.4% gain is better than a poke in the eye with a sharp stick.

In which asset class was I wrong every single time? Both of the volatility (VIX) trades I did in 2014 lost money, for a total of -1.68%. I got caught in one of many downdrafts that saw volatility hugging the floor for most of the year, giving it to me in the shorts with the (VXX).

All in all, it was a pretty good year.

What was my best trade of 2014? I made 2.75% with a short position in the S&P 500 in July, during one of the market?s periodic 5% corrections.

And my worst trade of 2014? I got hit with a 6.63% speeding ticket with a long position in the same index. But I lived to fight another day.

After a rocky start, 2015 promises to be another great year. That is, provided you ignore my advice on volatility.

Here is a complete list of every trade I closed last year, sorted by asset class, from best to worse.

Date

Position

Asset Class

Long/short

?

?

?

?

?

?

7/25/14

(SPY) 8/$202.50 - $202.50 put spread

equities

long

?

?

?

?

?

2.75%

10/16/14

(GILD) 11/$80-$85 call spread

equities

long

?

?

?

?

?

2.57%

5/19/14

(TLT) 7/$116-$119 put spread

fixed income

long

?

?

?

?

?

2.48%

4/4/14

(IWM) 8/$113 puts

equities

long

?

?

?

?

?

2.38%

7/10/14

(AAPL) 8/$85-$90 call spread

equities

long

?

?

?

?

?

2.30%

2/3/14

(TLT) 6/$106 puts

equities

long

?

?

?

?

?

2.27%

9/19/14

(IWM) 11/$117-$120 put spread

equities

long

?

?

?

?

?

2.26%

10/7/14

(FXE) 11/$127-$129 put spread

foreign exchange

long

?

?

?

?

?

2.22%

9/26/14

(IWM) 11/$116-$119 put spread

equities

long

?

?

?

?

?

2.21%

4/17/14

(TLT) 5/$114-$117 put spread

fixed income

long

?

?

?

?

?

2.10%

8/7/14

(FXE) 9/$133-$135 put spread

foreign exchange

long

?

?

?

?

?

2.07%

10/2/14

(BAC) 11/$15-$16 call spread

equities

long

?

?

?

?

?

2.04%

4/9/14

(SPY) 5/$191-$194 put spread

equities

long

?

?

?

?

?

2.02%

10/15/14

(DAL) 11/$25-$27 call spread

equities

long

?

?

?

?

?

1.89%

9/25/14

(FXE) 11/$128-$130 put spread

foreign exchange

long

?

?

?

?

?

1.86%

6/6/14

(JPM) 7/$52.50-$55.00 call spread

equities

long

?

?

?

?

?

1.81%

4/4/14

(SPY) 5/$193-$196 put spread

equities

long

?

?

?

?

?

1.81%

3/14/14

(TLT) 4/$111-$114 put spread

fixed income

long

?

?

?

?

?

1.68%

10/17/14

(AAPL) 11/$87.50-$92.50 call spread

equities

long

?

?

?

?

?

1.56%

10/15/14

(SPY) 11/$168-$173 call spread

equities

long

?

?

?

?

?

1.51%

7/3/14

(FXE) 8/$138 put spread

foreign exchange

long

?

?

?

?

?

1.51%

10/9/14

(FXE) 11/$128-$130 put spread

foreign exchange

long

?

?

?

?

?

1.48%

9/19/14

(FXE) 10/$128-$130 put spread

foreign exchange

long

?

?

?

?

?

1.45%

10/22/14

(SPY) 11/$179-$183 call spread

equities

long

?

?

?

?

?

1.44%

5/29/14

(TLT) 7/$118-$121 put spread

fixed income

long

?

?

?

?

?

1.44%

2/24/14

(UNG) 7/$26 puts

energy

long

?

?

?

?

?

1.40%

2/24/14

(BAC) 3/$15-$16 call spread

equities

long

?

?

?

?

?

1.39%

6/23/14

(SPY) 7/$202 put spread

equities

long

?

?

?

?

?

1.37%

9/29/14

(SPY) 10/$202-$205 Put spread

equities

long

?

?

?

?

?

1.29%

5/20/14

(AAPL) 7/$540 $570 call spread

equities

long

?

?

?

?

?

1.22%

9/26/14

(SPY) 10/$202-$205 Put spread

equities

long

?

?

?

?

?

1.22%

5/22/14

(GOOGL) 7/$480-$520 call spread

equities

long

?

?

?

?

?

1.16%

5/19/14

(FXY) 7/$98-$101 put spread

foreign exchange

long

?

?

?

?

?

1.14%

1/15/14

(T) 2/$35-$37 put spread

equities

long

?

?

?

?

?

1.08%

3/3/14

(TLT) 3/$111-$114 put spread

fixed income

long

?

?

?

?

?

1.07%

1/28/14

(AAPL) 2/$460-$490 call spread

equities

long

?

?

?

?

?

1.06%

4/24/14

(SPY) 5/$192-$195 put spread

equities

long

?

?

?

?

?

1.05%

6/6/14

(CAT) 7/$97.50-$100 call spread

equities

long

?

?

?

?

?

1.04%

7/23/14

(FXE) 8/$134-$136 put spread

foreign exchange

long

?

?

?

?

?

0.99%

8/18/14

(FXE) 9/$133-$135 put spread

foreign exchange

long

?

?

?

?

?

0.94%

11/4/14

(BAC) 12/$15-$16 call spread

equities

long

?

?

?

?

?

0.88%

4/9/14

(SPY) 6/$193-$196 put spread

equities

long

?

?

?

?

?

0.88%

7/25/14

(SPY) 8/$202.50 -205 put spread

equities

long

?

?

?

?

?

0.88%

6/6/14

(MSFT) 7/$38-$40 call spread

equities

long

?

?

?

?

?

0.87%

10/23/14

(FXY) 11/$92-$95 puts spread

foreign exchange

long

?

?

?

?

?

0.86%

7/23/14

(TLT) 8/$117-$120 put spread

fixed income

long

?

?

?

?

?

0.81%

3/5/14

(DAL) 4/$30-$32 Call spread

equities

long

?

?

?

?

?

0.76%

4/10/14

(VXX) long volatility ETN

equities

long

?

?

?

?

?

0.76%

1/30/14

(UNG) 7/$23 puts

equities

long

?

?

?

?

?

0.66%

4/1/14

(FXY) 5/$96-$99 put spread

foreign currency

long

?

?

?

?

?

0.60%

1/15/14

(TLT) 2/$108-$111 put spread

equities

long

?

?

?

?

?

0.47%

3/6/14

(EBAY) 4/$52.50- $55 call spread

equities

long

?

?

?

?

?

0.24%

10/14/14

(TBT) short Treasury Bond ETF

fixed income

long

?

?

?

?

?

0.22%

3/28/14

(VXX) long volatility ETN

equities

long

?

?

?

?

?

0.20%

7/17/14

(TBT) short Treasury Bond ETF

fixed income

long

?

?

?

?

?

0.08%

3/26/14

(VXX) long volatility ETN

equities

long

?

?

?

?

?

0.06%

7/8/14

(TLT) 8/$115-$118 put spread

fixed income

long

?

?

?

?

?

-0.18%

4/28/14

(SPY) 5/$189-$192 put spread

equities

long

?

?

?

?

?

-0.45%

3/5/14

(GE) 4/$24-$25 call spread

equities

long

?

?

?

?

?

-0.73%

4/28/14

(VXX) long volatility ETN

volatility

long

?

?

?

?

?

-0.81%

4/24/14

(TLT) 5/$113-$116 put spread

fixed income

long

?

?

?

?

?

-0.87%

4/28/14

(VXX) long volatility ETN

volatility

long

?

?

?

?

?

-0.87%

6/6/14

(IBM) 7/$180-$185 call spread

equities

long

?

?

?

?

?

-1.27%

9/30/14

(SPY) 11/$185-$190 call spread

equities

long

?

?

?

?

?

-1.51%

10/9/14

(TLT) 11/$122-$125 put spread

fixed income

long

?

?

?

?

?

-1.55%

9/24/14

(TSLA) 11/$200 call spread

equities

long

?

?

?

?

?

-1.62%

2/27/14

(SPY) 3/$189-$192 put spread

equities

long

?

?

?

?

?

-1.67%

3/6/14

(BAC) 4/$16 calls

equities

long

?

?

?

?

?

-2.01%

10/14/14

(SPY) 10/$180-$184 call spread

equities

short

?

?

?

?

?

-2.13%

11/14/14

(BABA) 12/$100-$105 call spread

equities

short

?

?

?

?

?

-2.38%

10/20/14

(SPY) 11/$197-$202 call spread

equities

short

?

?

?

?

?

-2.72%

7/3/14

(GM) 8/$33-$35 call spread

equities

long

?

?

?

?

?

-2.91%

3/7/14

(GM) 4/$34-$36 call spread

equities

long

?

?

?

?

?

-2.96%

11/25/14

(SCTY) 12/47.50-$52.50 call spread

equities

long

?

?

?

?

?

-3.63%

10/20/14

(SPY) 11/$197-$202 call spread

equities

short

?

?

?

?

?

-4.22%

4/14/14

(SPY) 5/$188-$191 put spread

equities

long

?

?

?

?

?

-6.63%

What a Year!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-15 09:01:572015-01-15 09:01:572014 Trade Alert Review

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.