Mad Hedge Technology Letter

October 21, 2019

Fiat Lux

Featured Trade:

(THE CLOUD BASICS)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

October 21, 2019

Fiat Lux

Featured Trade:

(THE CLOUD BASICS)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry and still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley, you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies regardless of their size prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Mad Hedge Technology Letter

October 18, 2019

Fiat Lux

Featured Trade:

(THE ROAD OUT OF SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

In a new study, 44% of Millennials plan to move out of the Bay Area in the “next few years.”

In the same study, 8% of Millennials will move out of the Californian tech peninsula within the next 365 days.

Tech companies are in serious danger of stagnating because they won’t be able to hire the talent needed to keep their companies afloat while the number of foreign HB-1 visas has dried up.

All of this could come home to roost and early cracks can be found in the local housing migratory trends.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money has made living with a roof over your head a tall order.

The area has also become squalid like some third world countries due to the homeless problem that is growing faster than any software company.

Salesforce Founder and CEO Marc Benioff has lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing forever.

He has also urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as government policy stiffens.

I have walked around the streets of San Francisco myself.

Places around Powell Bart station close to the Tenderloin district are eyesores littered with used syringes that lay in the gutter.

South of Market Street (SoMa) isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there anymore.

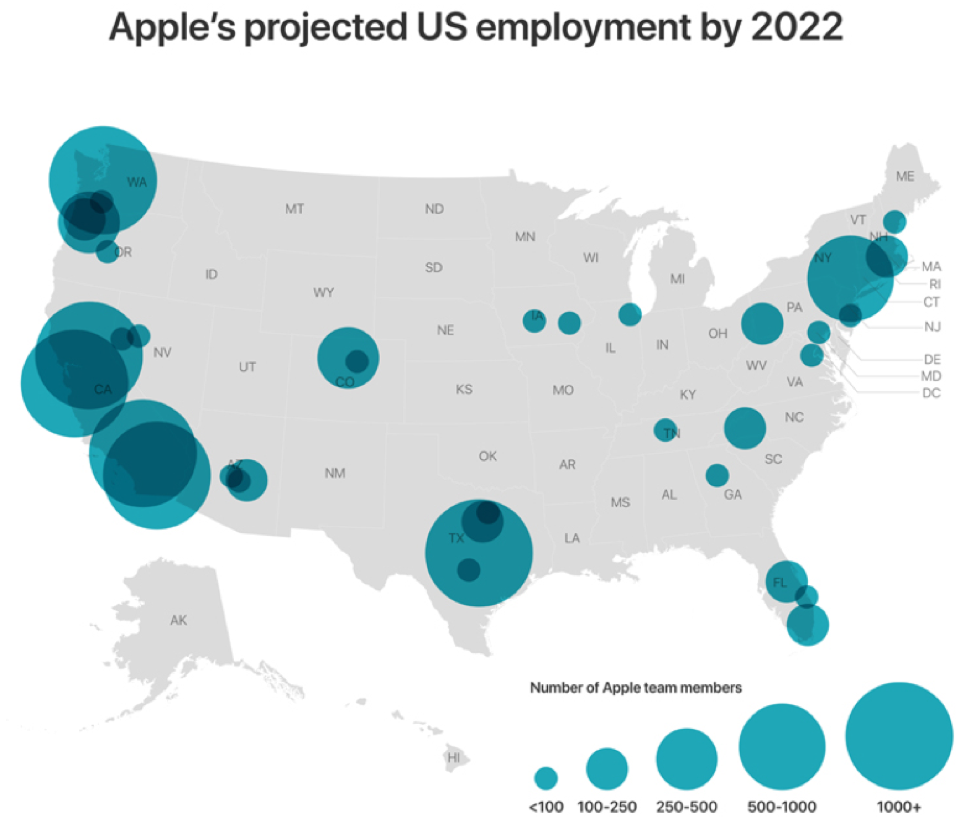

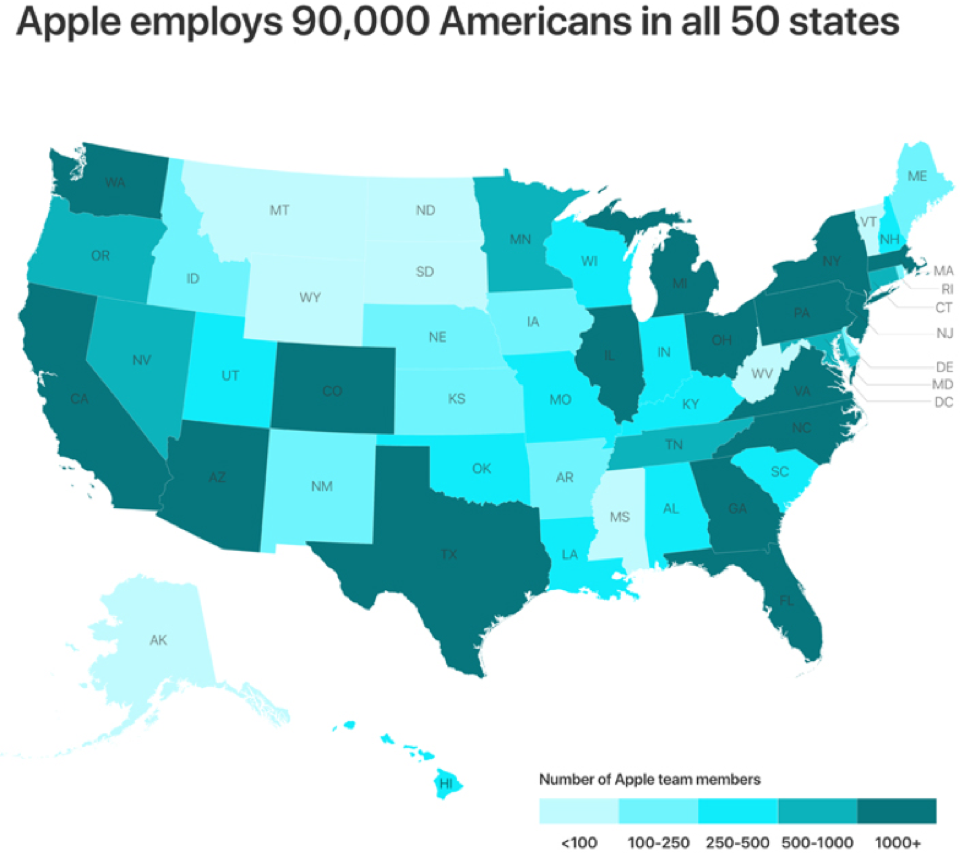

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas, and Amazon adding 500 employees in Nashville, Tennessee are all about.

Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Jobs simply flock to where the talent is.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area escaping the sky-high housing.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to take the first step onto the property ladder.

These are some of the practical issues that tech has failed to address, and part of the problem with unfettered capitalism which doesn’t consider quality of life.

No wonder why Silicon Valley real estate has dropped in the past year, people and their paychecks are on the way out.

Global Market Comments

October 14, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or UNICORNS AND CANDY CANE)

(AAPL), (FDX), (SPY), (IWM), (USO), (WMT), (AAPL), (GOOGL),

(X), (JPM), (WFC), (C), (BAC)

I have to tell you that flip-flopping from extreme optimism to extreme pessimism and back is a trader’s dream come true. Volatility is our bread and butter.

Long term followers know that when volatility is low, I struggle to make 1% or 2% a month. When it is high, I make 10% to 20%, as I have for two of the last three months.

That is what the month of October has delivered so far.

To see how well this works, the S&P 500 is dead unchanged so far this month, while the Mad Hedge Fund Trader alert service is up a gangbuster 10% and we are now 70% in cash.

While the market is unchanged in two years, risk has been continuously rising. That's because year on year earnings growth has fallen from 26% to zero. That means with an unchanged index, stocks are 26% more expensive.

Entire chunks of the market have been in a bear market since 2017, including industrials, autos, energy, and retailers. US Steel (X), which the president’s tariffs were supposed to rescue, has crashed 80% since the beginning of 2018.

The great irony here is that while the Dow Average is just short of an all-time high, all of the good short positions have already been exhausted. In short, there is nothing to do.

So, the wise thing to do here is to use the 1,200-point rally since Thursday to raise cash you can put to work during the next round of disappointment, which always comes. If we do forge to new highs, they will be incremental ones at best. That’s when you let your passive indexing friends pick up the next bar tab, who unintentionally caught the move.

In the meantime, we will be bracing ourselves for the big bank earnings due out this week which are supposed to be dismal at best. JP Morgan (JPM), Wells Fargo (WFC), and Citigroup (C) are out on Tuesday and Bank of America (BAC) publishes on Wednesday.

That’s when we find out how much of this move has been about unicorns and candy canes, and how much is real.

Trump demoed his Own trade talks, creating a technology blacklist and banning US pension investment into the Middle Kingdom. He also hints he’ll take a small deal rather than a big one. Great for American farmers but leaves intellectual property and forced joint ventures on the table, throwing the California economy under the bus. I knew it would end this way. It’s very market negative. Without a trade deal, there is no way to avoid a US recession in 2020.

The Inverted Yield Curve is flashing “recession.” The three-month Treasury yield has been above the 10-year bond yield since May, and that always says a downturn is coming. The time to batten down the hatches is now.

US Producer Prices plunged in September, down 0.3%, the worst since January. It’s another recession indicator but also pushes the Fed to lower rates further.

Inflation was Zero in September, with the Consumer Price Index up 1.8% YOY. Slowing economy due to the trade war gets the blame, but I think that accelerating technology gets the bigger blame.

New Job Openings hit an 18-month low, down 123,000 to 7.05 million in August, as employers pull back in anticipation of the coming recession. Trade war gets the blame. The smart people don’t hire ahead of a recession.

FedEx (FDX) is dead money, says a Bernstein analyst, citing failing domestic and international sales. No pulling any punches, he said “The bull thesis has been shredded.” Not what you want to hear from this classic recession leading indicator. Nobody ships anything during a slowdown.

Loss of SALT Deductions cost you $1 trillion, or about 4% per home, according to an analysis by Standard & Poor’s. Quite simply, losing the ability to deduct state and local tax deductions creates a higher after-tax cost of carry that reduces your asset value. If you bought a home in 2017 you lost half of your equity almost immediately. The east and west coast were especially hard hit.

Fed to expand balance sheet to deal with the short-term repo funding crisis, which periodically has been driving overnight interest rates up to an incredible 5%. Massive government borrowing is starting to break the existing financial system. What they’re really doing is trying to head off to the next recession.

The Fed September minutes came out, and traders seem to be expecting more rate cuts than the Fed is. Trade is still the overriding concern. The next meeting is October 29-30. It could all end in tears.

Apple (AAPL) raised iPhone 11 Production by 10%, to 8 million more units, according Asian parts suppliers. Great news for its $1,089 top priced product ahead of the Christmas rush. It turns out that an Apple app is helping Hong Kong protesters manage demonstrations. I’m keeping my long, letting the shares run to a new all-time high. Buy (AAPL) on the dips.

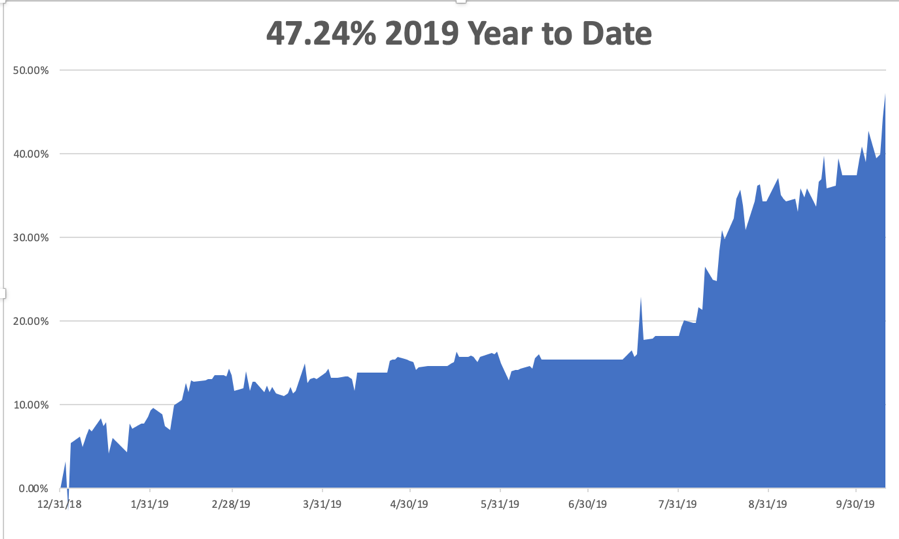

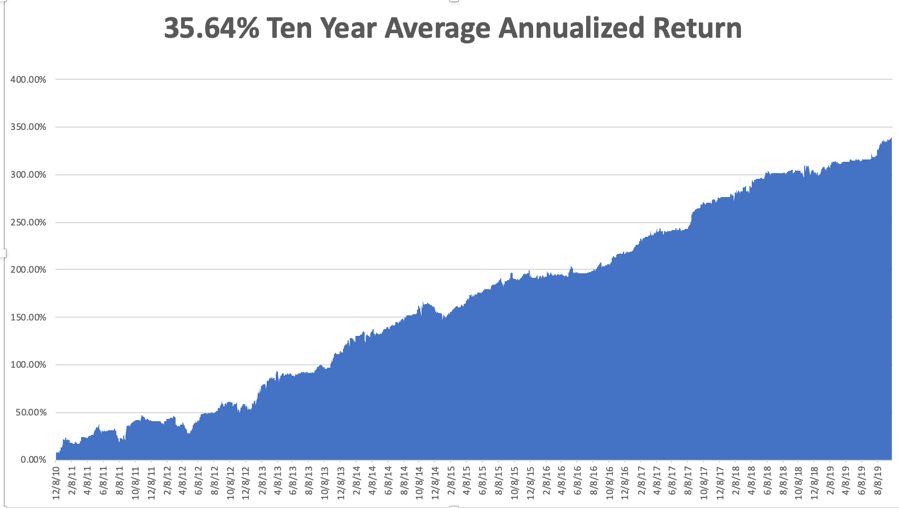

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of +347.48% and my year-to-date accelerated to +47.24%. The tricky and volatile month of October started out with a roar +9.82%. My ten-year average annualized profit bobbed up to +35.64%.

Some 26 out of the last 27 trade alerts have made money, a success rate of 94%! Underpromise and overdeliver, that's the business I have been in all my life. It works. This is rapidly turning into the best year of the decade for me. It is all the result of me writing three newsletters a day.

I used the recession fear-induced selloff after October 1 to pile on a large aggressive short-dated portfolio which I will run into expiration. I am 60% long with the (SPY), (IWM), (USO), (WMT), (AAPL), and (GOOGL). I am 10% short with one position in the (IWM) giving me a net risk position of 50% long. All of them are working.

The coming week is pretty non-eventful of the data front. Maybe the stock market will be non-eventful as well.

On Monday, October 14, nothing of note is published.

On Tuesday, October 15 at 8:30 AM, the New York Empire State Manufacturing Index is released. JP Morgan (JPM), Wells Fargo (WFC), and Citigroup (C) kick off the Q3 earnings season with reports.

On Wednesday, October 16, at 8:30 AM, we learn the September Retail Sales. Bank of America (BAC) and CSX Corp. (CSX) report.

On Thursday, October 17 at 8:30 AM, the Housing Starts for September are out. Morgan Stanley (MS) reports.

On Friday, October 18 at 8:30 AM, the Baker Hughes Rig Count is released at 2:00 PM. Schlumberger (SLB), American Express (AXP), and Coca-Cola (KO) report.

As for me, I’ll be going to Costco to restock the fridge after last week’s two-day voluntary power outage by PG&E. Expecting Armageddon, I finished off all the Jack Daniels and chocolate in the house. We managed to eat all of our frozen burritos, pork chops, steaks, and ice cream in a mere 48 hours. But that’s what happens when you have two teenagers.

Hopefully, it will rain soon for the first time in six months bringing these outages to an end.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 7, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WILL HE OR WON’T HE?)

(INDU), (USO), (TM), (SCHW), (AMTD), (ETFC), (SPY), (IWM), (USO), (WMT), (AAPL), (GOOGL), (SPY), (C)

Once again, the markets are playing out like a cheap Saturday afternoon matinee. We are sitting on the edge of our seats wondering if our hero will triumph or perish.

The same can be said about financial markets this week. Will a trade deal finally get inked and prompt the Dow Average to soar 2,000 points? Or will they fail once again, delivering a 2,000-point swan dive?

I vote for the latter, then the former.

Still, I saw this rally coming a mile off as the Trump put option kicked in big time. That's why I piled on an aggressive 60% long position right at last week’s low. Carpe Diem. Seize the Day. Only the bold are rewarded.

Or as Britain’s SAS would say, “Who dares, wins.”

It takes a lot of cajones to trade a market that hasn’t moved in two years, let alone take in a 55% profit during that time. But you didn’t hire me to sit on my hands, play scared, and catch up on my Shakespeare.

I think markets will eventually hit new all-time highs sometime this year. The game is to see how low you can get in before that happens without getting your head handed to you first.

Last week saw seriously dueling narratives. The economic data couldn’t be worse, pointing firmly towards a recession. But the administration went into full blown “jawbone” mode, talking up the rosy prospects of an imminent China trade deal at every turn.

This was all against a Ukraine scandal that reeled wildly out of control by the day. Is there a country that Trump DIDN’T ask for assistance in his reelection campaign? Now we know why the president was at the United Nations last week.

The September Nonfarm Payroll Report came in at a weakish 136,000, with the Headline Unemployment rate at 3.5%, a new 50-year low.

Average hourly earnings fell. Apparently, it is easy to get a job but impossible to get a pay raise. July and August were revised up by 45,000 jobs.

Healthcare was up by 39,000 and Professional and Business Services 34,000. Manufacturing fell by 2,000 and retail by 11,0000. The U-6 “discouraged worker” long term unemployment rate is at 6.9%.

The US Manufacturing Purchasing Managers Index collapsed in August from 49.7 to 47.9, triggering a 400-point dive in the Dow average. This is the worst report since 2009. Manufacturing, some 11% of the US economy, is clearly in recession, thanks to the trade war-induced loss of foreign markets. A strong dollar that overprices our goods doesn’t help either.

The Services PMI Hit a three-year low, from 53.1 to 50.4, with almost all economic data points now shouting “recession.” The only question is whether it will be shallow or deep. I vote for the former.

Consumer Spending was flat in August. That’s a big problem since the average Joe is now the sole factor driving the economy. Everything else is pulling back. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, edged up 0.1% last month as an increase in outlays on recreational goods and motor vehicles was offset by a decrease in spending at restaurants and hotels.

The Transports, a classic leading sector for the market, have been delivering horrific price action this year giving up all of its gains relative to the S&P 500 since the 2009 crash.

Oil (USO) got crushed on recession fears, down a stunning 19.68% in three weeks. The global supply glut continues. Over production and fading demand is not a great formula for prices.

Toyota Auto Sales (TM) cratered by 16.5% in September, to 169,356 vehicles in another pre-recession indicator. It’s the worst month since January during a normally strong time of the year. The deals out there now are incredible.

Online Brokerage stocks were demolished on the Charles Schwab (SCHW) move to cut brokerage fees to zero. TD Ameritrade (AMTD) followed the next day and was spanked for 23%, and E*TRADE (ETFC) punched for 17. These are cataclysmic one0-day stock moves and signal the end of traditional stock brokerage.

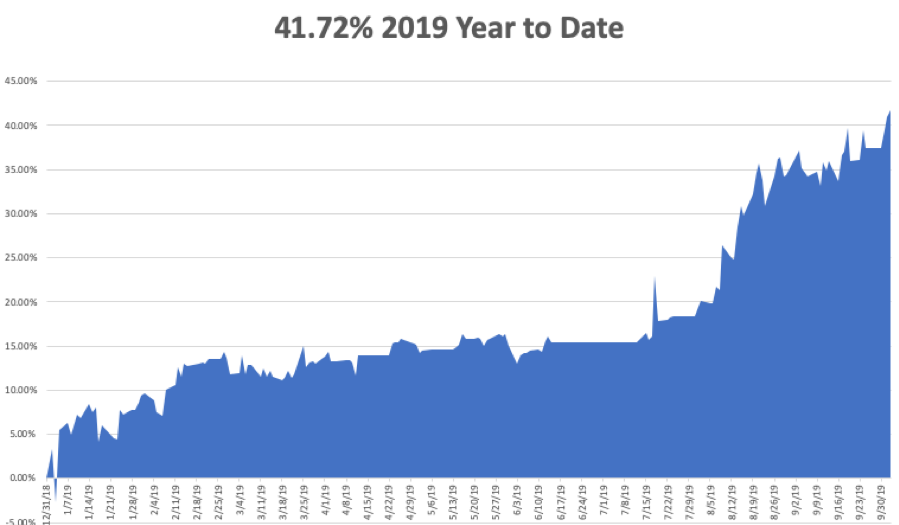

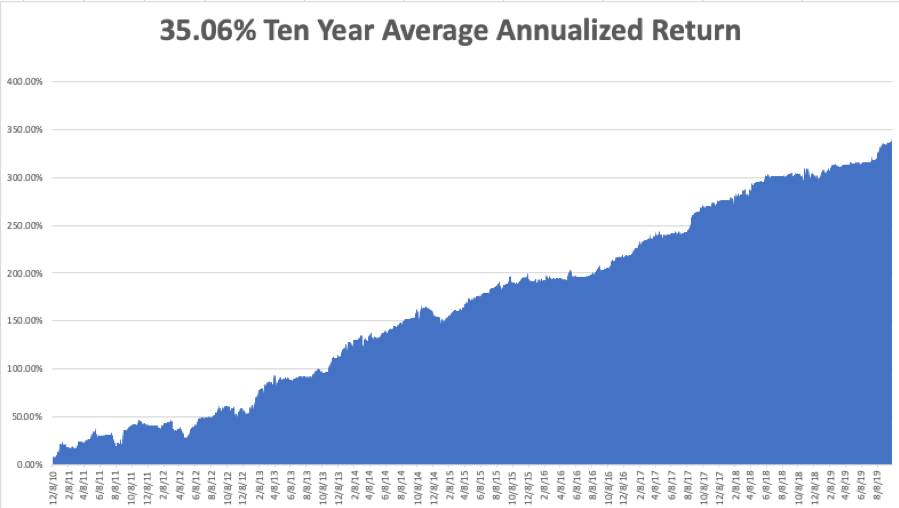

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of 341.86% and my year-to-date accelerated to +41.72%. The tricky and volatile month of October started out with a roar +5.40%. My ten-year average annualized profit bobbed up to +35.06%.

Some 26 out of the last 27 trade alerts have made money, a success rate of 96.29%! Under promise and over deliver, that's the business I have been in all my life. It works.

I used the recession-induced selloff since October 1 to pile on a large aggressive short dated portfolio. I am 60% long with the (SPY), (IWM), (USO), (WMT), (AAPL), and (GOOGL). I am 20% short with positions in the (SPY) and (C), giving me a net risk position of 40% long.

The coming week is all about the September jobs reports. It seems like we just went through those.

On Monday, October 7 at 9:00 AM, the US Consumer Credit figures for August are out.

On Tuesday, October 8 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, October 9, at 2:00 PM, we learn the Fed FOMC Minutes from the September meeting.

On Thursday, October 10 at 8:30 AM, the US Inflation Rate is published. US-China trade talks may, or may not resume.

On Friday, October 11 at 8:30 AM, the University of Michigan Consumer Sentiment for October is announced.

The Baker Hughes Rig Count is released at 2:00 PM.

As for me, I’m still recovering from running a swimming merit badge class for 60 kids last weekend. Some who showed up couldn’t swim, while others arrived with no swim suits, prompting a quick foray into the lost and found.

One kid jumped in and went straight to the bottom, prompting an urgent rescue. Another was floundering after 15 yards. When I pulled him out and sent him to the dressing room, he started crying, saying his dad would be mad. I replied, “Your dad will be madder if you drown.”

I never felt so needed in my life.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 3, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S MAJOR BREAKTHROUGH IN QUANTUM COMPUTING),

(GOOGL), (IBM)

(AI AND THE NEW HEALTHCARE),

(XLV), (BMY), (AMGN)

Global Market Comments

September 16, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or CHOPPY WEATHER AHEAD),

(SPY), (TLT), (FB), (GOOGL), (M), (C),

(XOM), (NFLX), (DIS), (FXE), (FXI)