Global Market Comments

December 27, 2019

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN),

Global Market Comments

December 27, 2019

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN),

Global Market Comments

October 18, 2019

Fiat Lux

Featured Trade:

(OCTOBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (C), (GM), (IWM), ($RUT), (FB),

(INTC), (AA), (BBY), (M), (RTN), (FCX), GLD)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 16 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: How do you think the S&P 500 (SPX) will behave with the China trade negotiations going on?

A: Nobody really knows; no one has any advantage here and logic or rationality doesn’t seem to apply anymore. It suffices to say it will continue to be up and down, depending on the trade headline of the day. It’s what I call a “close your eyes and trade” market. If it’s down, buy it; if it’s, upsell it.

Q: How long can Trump keep kicking the can down the road?

A: Indefinitely, unless he wants to fold completely. It looks like he was bested in the latest round of negotiations because the Chinese agreed to buy $50 billion worth of food they were going to buy anyway in exchange for a tariff freeze. Of course, you really don’t get a trade deal unless you get a tariff roll back to where they were two years ago.

Q: Did I miss the update on the Citigroup (C) trade?

A: Yes, we came out of Citigroup a week ago for a small profit or a break-even. You should always check our website where we post our trading position sheet every day as a backstop to any trade alerts you’re getting by email. Occasionally emails just go completely missing, swallowed up by the ether. To find it go to www.madhedgefundtrader.com , log in, go to My Account, Global Trading Dispatch, then Current Positions. You can also find my newly updated long-term portfolio here.

Q: How much pain will General Motors (GM) incur from this standoff, and will they ever reach a compromise?

A: Yes, the union somewhat blew it in striking GM when they had incredibly high inventories which the company is desperate to get rid of ahead of a recession. If you wonder where all those great car deals are coming from, that's the reason. All of the car companies want to go into a recession with as little inventory as possible. It's not just GM, it’s everybody with the same problem.

Q: When does the New Daily Position Sheet get posted?

A: About every hour after the close each day. We need time to process our trades, update all the position sheets before getting it posted.

Q: What do you think about Bitcoin?

A: We hate it and don’t want to touch it. It’s unanalyzable, and only the insiders are making money.

Q: Are you predicting a repeat of Fall 2018 going into the end of this year to close at the lows?

A: No, I’m not. A year ago, we were looking at four interest rate increases to come. This year we’re looking at 1 or 2 more interest rate cuts. It’s nowhere near the situation we saw a year ago. The most we’re going to get is a 7% selloff rather than a 20% selloff and if anything, stocks will rise into the yearend then fall.

Q: Why are we trading the Russell 200 (IWM) instead of the ($RUT) Small Cap Index? We pay less commissions to brokers.

A: There's more liquidity in the (IWM). You have to remember that the combined buying power of the trade alert service is about $1 billion. And that’s harder to do with smaller illiquid ETFs like the ($RUT), especially the options.

Q: If this is a “Don’t fight the Fed” rally for investors, where else is there to go but stocks?

A: Nowhere. But it’s happening in the face of an oncoming recession, so it’s not exactly a great investment opportunity, just a trading one. 2009 was a great time not to fight the Fed.

Q: Do you want to buy Facebook (FB) even though there are so many threats of government scrutiny and antitrust breakups?

A: The anti-trust breakups are never going to happen; the government can't even define what Facebook does. There may be more requirements on disclosures, which means nothing because nobody really cares about disclosures—they just click the box and agree to anything. I was actually looking at this as a buy when we had the big selloff at the end of September and instead, I bought four other Tech stocks and (FB) had moved too far when we got around to it. I think there’s upside potential for Facebook, especially if we can move out of this current range.

Q: Would you sell short European banks? It seems like they’re cutting jobs right and left.

A: I always get this question after big market meltdowns. European banks have been underpricing risks for decades and now the chickens are coming home to roost. Some of these things are down 80-90% so it’s too late to sell short. The next financial crisis is going to be in Europe, not here.

Q: Is it time to short Best Buy (BBY) due to the China deal?

A: No, like Macys (M), Best Buy is heavily dependent on imports from China, and the stock has gotten so low it’s hard to short. And the problem for the whole market in general is all the best sectors to short are already destroyed, down 80-90%. There really is nothing left to short, now that all the bad sectors have been going down for nearly two years. There has been a massive bear market in large chunks of the market which no one has really noticed. So, that might be another reason the market is going up—that we’ve run out of things to short.

Q: Do you like Intel (INTC)?

A: Yes, for the long term. Short term it still could face some headwinds from the China negotiations, where they have a huge business.

Q: Would you buy American Airlines (AA) on the return of Boeing 737 MAX to the fleet?

A: Absolutely, yes. The big American buyers of those planes are really suffering from a shortage of planes. A return of the 737 MAX to the assembly line is great news for the entire industry.

Q: Do you like Raytheon (RTN)?

A: No, Trump has been the defense industry’s best friend. If he exits in the picture, defense will get slaughtered—it will be the first on the chopping block under a future democratic administration. And, if you’re doing nothing but retreating from your allies, you don't need weapons anyway.

Q: Will Freeport McMoRan (FCX) benefit from a trade war resolution?

A: Yes, the fact that it isn't moving now is an indication that a trade war resolution has not been reached. (FCX) has huge exposure to traditional metal bashing industries like they still have in China.

Q: Would you go long or short gold (GLD) here?

A: No, I'm waiting for a bigger dip. If you can get in close to the 200-day moving average at $129.50, that would be the sweet spot. Longer term I still like gold and it is a great recession hedge.

Good Luck and Good Trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 10, 2019

Fiat Lux

SPECIAL ARTIFICIAL INTELLIGENCE ISSUE

Featured Trade:

(NEW PLAYS IN ARTIFICIAL INTELLIGENCE),

(NVDA), (AMD), (ADI), (AMAT), (AVGO), (CRUS),

(CY), (INTC), (LRCX), (MU), (TSM)

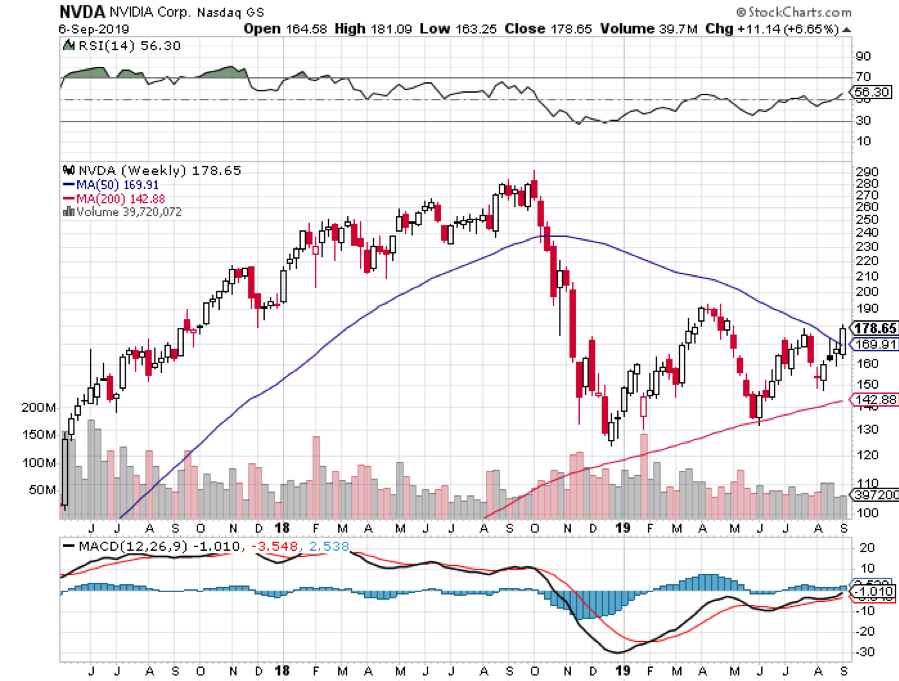

It’s been three years since I published my first Special Report on artificial intelligence and urged readers to buy the processor maker NVIDIA (NVDA) at $68.80.

The stock quadrupled, readers are understandably asking me for my next act in the sector.

The good news is that I have one.

For a start, you could go out and buy NVIDIA again.

With an explosive 50% annual earnings growth, a near-monopoly in super fast processors, and a huge lead over the competition, I think there is another double in the shares that could take the price up to a stratospheric $300. Its newest super-fast graphics card, the Turing, promises to be a real barn burner and dominate the industry yet again.

But I can do better than that.

The good news if you are new to this sector is that the entire AI space has started to broaden out to offer a host of investment opportunities beyond the tiny handful I first mentioned in 2016.

These include legacy chipmakers, survivors of the great Dotcom bust, whose shares have barely moved in years.

Yes, there is such a thing as a cheap AI stock. To find out who they are, read on.

The reason for the expansion of the AI sector is that practically overnight these ultra-sophisticated algorithms have become essential to any company that wants to survive in online commerce or stay in business….period.

Those of us who have been in this business for more than 15 minutes have seen this pattern before, and the resulting impact on share prices: the Boeing 707, the personal computer, Windows, the Internet, and the smart cell phone.

AI is everywhere.

In the old days, visiting a website and window-shopping their products was easy. You just clicked around a few times and then moved on to the next site.

Now if you click on a product once, that site will follow you around relentlessly for months, appearing in the margins of your emails, offering you endless discounts and special deals.

I bought a Dell computer six months ago, and it is still pounding away at me with better offers. I feel like such a dummy buying a machine at the first price asked.

That is all AI.

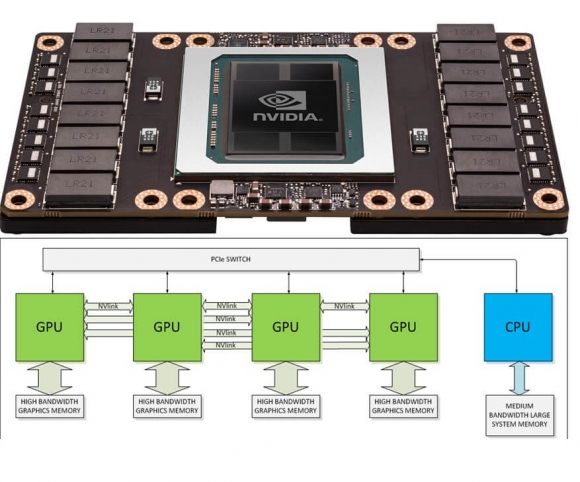

The auto industry is now a major growth industry for AI. Even a simple garden-variety vehicle needs 100 chips just to operate.

The gull-wing doors on my new Tesla Model X each has its own learning program. They never open the same way twice.

In fact, when I first picked up the car last year, the salesman warned by saying it would be “stupid” for the first 3,000 miles.

It had to “learn” how to drive before I let it attempt any sophisticated self-driving maneuvers, like backing into a parking space on a crowded street.

I let it park itself in my garage now. I have only had a heart attack once.

With US annual auto production at 16.7 million units annualized, and global car and commercial vehicle production at a record 94.64 million, that is a lot of processors.

I have been covering Silicon Valley since it was a verdant, sun-kissed peach orchard in Northern California.

I have to say that in the half-century that I have followed the technology industry, I have never seen the principals, gurus, and visionaries so excited about a major new trend like AI.

Asking if AI is relevant now is like pondering the future of Thomas Edison’s new electricity invention in 1890.

If you think that AI still belongs in the realm of science fiction, you obviously didn’t get the memo. It is all around us all the time, 24/7. You just don’t know it yet.

And here’s the rub.

It is impossible to invest purely in AI.

All-new AI startups comprise small teams of experts from private labs and universities financed by big venture capital firms like Sequoia Capital, Kleiner Perkins, and Andreeson Horowitz.

After developing software for a year or two, they are sold on to major technology firms at huge premiums. They never see the light of day in the form of a public listing.

Alphabet (GOOGL) acquired Britain-based Deep Mind in 2014. Later that year, Google’s AlphaGo program defeated the world’s top-ranked Go player.

In 2016, Microsoft (MSFT) purchased Equivio, a small firm that applies AI to advanced document searches on the Internet.

Amazon (AMZN) recently bought out Orbeus, a startup known for machine learning tools for image recognition.

Amazon’s Jeff Bezos now says that his Amazon Fresh home food delivery service is using AI to grade strawberries.

Really!

We’re not talking small potatoes here.

The global artificial intelligence market is expected to grow at an annual rate of 44.3% a year to $23.5 billion by 2025.

Nearly half of all applications now use some form of AI that by 2020 will earn businesses an extra $60 billion a year in profits.

And from what I have learned from speaking to the major players over the last few weeks, I am convinced that these are low numbers by an order of magnitude.

I have been following developments in artificial intelligence since the 1960s.

There were those feeble computer dating attempts in the early seventies where we all had to prepare IBM punch cards.

I was matched with an annoyingly aggressive bleach blonde real estate agent. (Really?). Her only real qualification was that she was female.

It took decades and tens of thousands of programming man-hours before IBM’s Deep Blue could become a chess grandmaster in 1996, defeating Gary Kasparov.

Big Blue’s latest effort came to us with Watson in 2007, an 85,000-watt behemoth with 90 servers and 15 terabytes of data, or three quarters of the content of the entire Library of Congress.

The machine can read a staggering 1 million books a second. IBM has so far poured $15 billion into the project.

In 2011, Watson defeated the top-rated Jeopardy game show contestant by answering the question “What city’s national museum lost the “Lion of Nimrod.” The answer was “What is Baghdad” (I knew that!).

Today, Watson is on loan to the University of North Carolina at Chapel Hill where it has been deployed to cure cancer.

It took scientists a week to teach Watson how to read medical literature. In the second week, it read every paper published on cancer, some 25 million.

By the third week, it was proposing customized cures for advanced cancer patients, which achieved a 33% success rate.

After all, it can read all of the 8,000 cancer papers that are published every day from around the world IN SECONDS!

Scientists say that Watson has so far reached only 1% of its true potential.

It gets better than that.

A clinic can now biopsy your tumor, sequence its DNA, design a custom protein that will target and destroy your personal tumor, mass-produce it, inject it in your tumor, and cure you of cancer in a month.

This is being done with human volunteers in clinical trials NOW.

Expect this procedure to go retail and be made available to you in about five years. And by that, I mean cheap, locally available, and covered by your health insurance policy.

I believe that Watson and its future offspring will cure the major human maladies within a decade. My generation will probably be the last to suffer serious disease.

It isn’t just Watson that will take us the great leap forward in computing. By 2020, you will be able to buy a low-end laptop for $500 that can hold ALL KNOWLEDGE ACCUMULATED IN HUMAN HISTORY!

They better hurry. That body of knowledge is doubling every 18 months!

It is a key part of my argument that the US will enjoy a Golden Age and see a return of the “Roaring Twenties” during the 2020s.

If you have in any way been involved in the stock market for the past five years, AI has invaded your life.

High frequency trading and hedge funds now account for 70% of the daily trading volume on the major stock exchanges, and almost all of this is AI-driven.

Having spent my entire life trading stocks, I can confirm that in recent years the market’s character has dramatically changed, and not for the better. Call it trading untouched by human hands.

Algorithms are trading against algorithms, and whoever wins the nuclear arms race brings home the big bucks.

You used to need degrees in Finance and Economics, or perhaps an MBA, to become a professional fund manager. Now it’s a Ph.D. in Computer Science.

Remember the May 2010 flash crash when the Dow Average plunged 1,100 points in minutes wiping out $4.1 billion in equity value? AI’s fingerprints were all over that.

In 2016, the British pound lost 6% of its value in a mere two minutes, a move unprecedented in the history of foreign exchange markets. The culprit was AI.

Don’t expect the path forward to AI to be an easy one.

Indeed, the machines already have the power of life and death over all of us.

No less figures than Nobel Prize winner Dr. Stephen Hawking and Tesla’s Elon Musk have warned that computers and the Internet may have the power to pose a threat to human existence within a decade.

They are especially concerned about the militarization of powerful robots, something I know the US Defense Department is hell-bent on developing.

As I write this, the only thing preventing a drone attacking a village in Afghanistan is an Army corporal hitting a red button on a console in Nevada.

In the future, antivirus software won’t be needed to protect your computer. It will be essential to protect you FROM your computer.

You know that massive denial of service attack that hit the United States on October 21, 2016?

I asked one of my friends at security giant Palo Alto Networks (PANW) if it was the Russians again. He replied, “You better hope it’s the Russians.”

The implication is that the Internet may have launched the attack itself.

Now, about that stock recommendation.

Since we aren’t venture capitalists, we can’t buy into pure AI firms in their early stages. And I’m too old to get a Ph.D. in computer science.

We, therefore, have to be sneaky and get in through the back door via an indirect play which still has plenty of upside leverage.

My current favorite among the AI alternative stocks is Advanced Micro Devices (AMD).

If Intel only piques your appetite for AI stocks and you feel you need another serving, I have listed below ten names that will benefit mightily from this once-a-century opportunity.

AI Stock to BUY

Advanced Micro Devices (AMD)

Analogue Devices Communication (ADI)

Applied Materials (AMAT)

Broadcom (AVGO)

Cirrus Logic (CRUS)

Cypress Semiconductor (CY)

Intel (INTC)

Lam Research (LRCX)

Micron Technology (MU)

Taiwan Semiconductor (TSM)

If you’re really lazy, you can just buy a basket of semiconductor stocks through an industry-specific ETF.

The largest is the VanEck Vectors Semiconductor ETF (SMH), with $1.3 billion in assets under management. For a prospectus on the fund, please click here.

Or you could just stick with NVIDIA.

No matter how you want to slice and dice it, AI should be a dominant factor in your IRA, 401k, or benefit plan.

And you are a trader by nature, this will be a great sector to trade around.

As for your computer, you better start leaving it unplugged at night.

You never know.

![]()

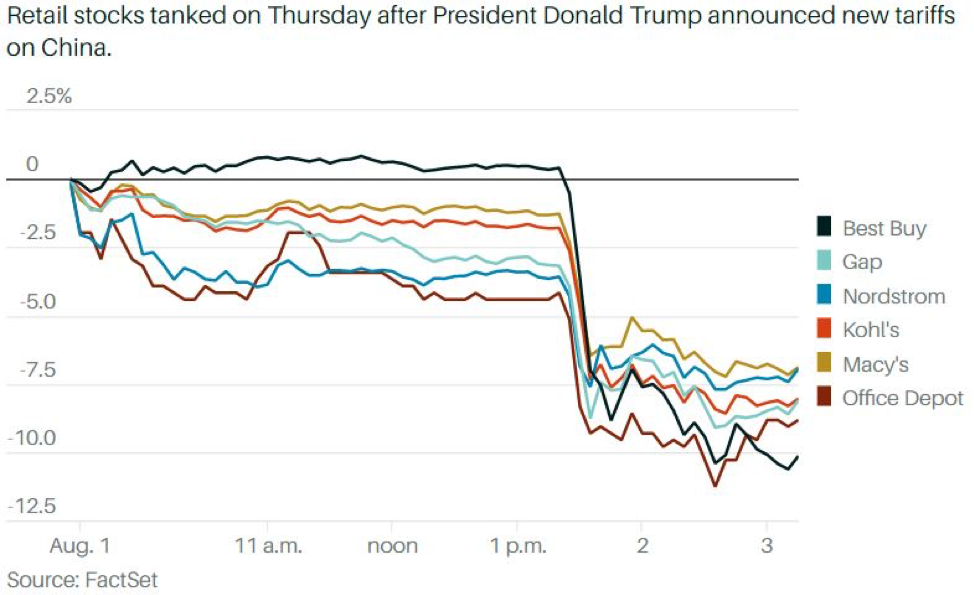

Mad Hedge Technology Letter

August 5, 2019

Fiat Lux

Featured Trade:

(THE CHINA TARIFF BOMBSHELL AND TECHNOLOGY),

(AAPL), (NVDA), (INTC), (MU), (WDC), (BBY)

With one little tweet, the state of technology and the companies that rely on the public markets that serve them went haywire.

U.S. President Donald Trump levied another 10% on the $300 billion that had not been tariffed up yet compounding the misery for anyone who has any vested interest in trade with mainland China.

The tariffs will take effect on September 1st.

How does this shake out for American technology?

Any brand tech name that has substantial supply chain operations can kiss their stay in the Middle Kingdom goodbye.

If management didn’t understand that before, then it's clear as night that they need to shift their supply chain out of the reaches of the Chinese communist party.

The U.S. Administration tripling down on China being our archnemesis means that any sort of cross-border economic trade or cultural exchange will be viewed through the prism of warped geopolitics.

The U.S. President Donald Trump has in fact taken a page out of the Chinese playbook turning everything he sees and touches into a transactional tool for what he is pursuing at the time or in the future.

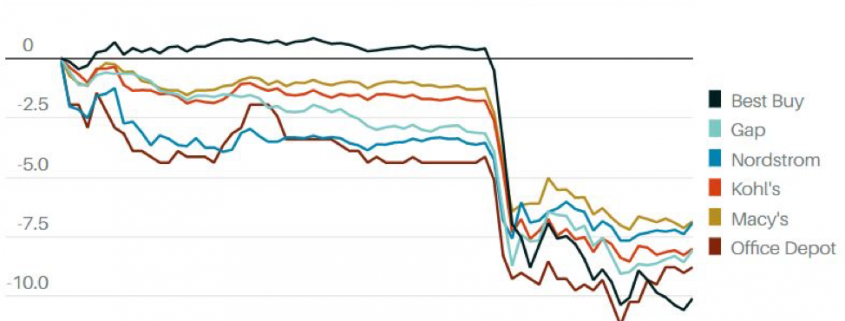

Specific companies facing the wrath of the tariffs are companies as conspicuous as Apple filtering down to the SMEs that make local business local.

Semiconductor chips are a huge loser in this new development as the price of electronic goods will rise with the tariffs.

If you want a name that lies in the heart of electronic consumer goods, then BestBuy (BBY) would encapsulate this thesis and unsurprisingly they were taken out to the back of the woodshed and taught a lesson dropping 10% on the news.

Any technology outfit that imports goods from China will be hit as well and this means semiconductor chips along the lines of Nvidia (NVDA), Intel (INTC), Western Digital (WDC) and Micron (MU) among others.

Chips are the meat and bones that go into end products like iPads and a slew of smart devices.

Demand will be hit because of the cost of producing these types of consumer products will rise.

The softness is showing up in the numbers with Apple’s iPhone revenue down 12% year-over-year.

Samsung of Korea also showed that this isn’t just an American problem with their semiconductor division’s operating profits down 71% year-over-year.

The Korean conglomerate is in a spat with the Japanese government over war crimes from the second world war causing the Japanese government to bottleneck the supply of chemicals needed to produce high-level semiconductor chips.

The export restriction will drag down SK Hynix display business who is one of the largest producers of DRAM chips and also a Korean company.

Consumers are also using their phones longer with Apple iPhone customers holding their device up to 4 years delaying the refresh cycle.

The company that Steve Jobs built will have to repurpose themselves for a brave new tech landscape that includes heavier regulation, trade tariffs, and device saturation.

When investors talk about the “low hanging fruit,” at this point, Apple isn’t one of them.

And if you think the services business is a cakewalk, ponder about how many apps and behemoths that spit out a whole lineup of apps.

Apple still has its ecosystem and should guard it with its life, this is the same ecosystem that can charge Google around $10 billion per year to slap on Google search as the primary search engine on Apple devices.

Expect tech to telegraph a deceleration in revenue for the last quarter and next year.

The tech environment is brittle at this point and uncertainty wafts in the air like a hot stack of pancakes.

Global Market Comments

July 29, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE BAD OMENS ARE THERE),

(INTC), (GOOGL), (AMZN), (JPM), (FXB),

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS), (TLT)

The Omens are there.

I am normally a pretty positive guy.

But I was having a beer at Schwarzee at the base of the Matterhorn the other day, just having completed the climb up to the Hornli Hut at 10,758 feet. I carefully watched with my binoculars three helicopters circle the summit of the mountain, around the Solvay Hut.

These were not sightseeing tours. The pilots were taking great risks to retrieve bodies.

I learned at the Bergfuhrerverein Zermatt the next day that one of their men was taking up an American client to the summit. The man reached for a handhold and the rock broke loose, taking both men to their deaths. The Mountain Guide Service of Zermatt is a lot like the US Marine Corps. They always retrieve their dead.

It is an accident that could have happened to anyone. I have been over that route many times. If there was ever an omen of trouble to come, this was it.

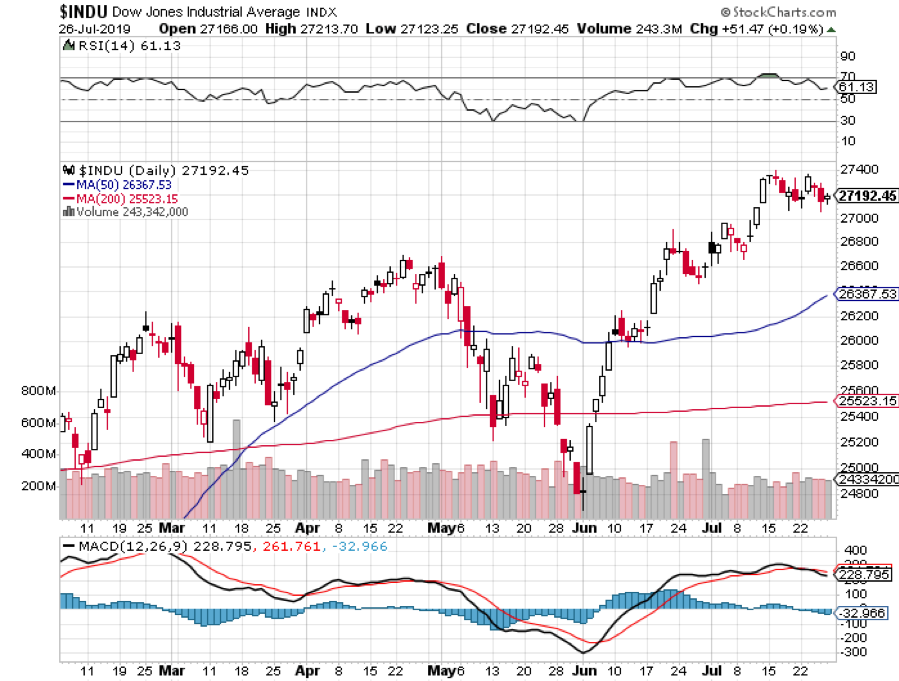

The markets are sending out a few foreboding warnings of their own. Friday’s Q2 GDP report came in at a better than expected 2.1%, versus 3.1% in Q1.

Yet the Dow Average was up only a meager 51.47 points when it should have gained 500. It is an old market nostrum that if markets can’t rally on good news, you get the hell out of Dodge. Zermatt too.

It is the slowest US growth in two years. The trade war gets the blame, with falling exports offsetting healthy consumer spending. With the $1.5 trillion tax cut now spent, nothing is left but the debt. 2020 recession fears are running rampant, so paying all-time highs for stock prices is not a great idea.

You might be celebrating last week’s budget deal which heads off a September government shutdown. But it boosts the national debt from $22 to $24 trillion, or $72,000 per American. As with everything else with this administration, a short-term gain is achieved at a very high long-term cost.

Boris Johnson, the pro-Brexit activist, was named UK prime minister. It virtually guarantees a recession there and will act as an additional drag on the US economy. Global businesses will accelerate their departure from London to Paris and Berlin.

The end result may be a disunited kingdom, with Scotland declaring independence in order to stay in the EC, and Northern Ireland splitting off to create a united emerald island. The stock market there will crater and the pound (FXB) will go to parity against the greenback.

The European economy is already in a downward spiral, with German economic data flat on its back. GDP growth has shrunk from 2.0% to 0.7%. It seems we are not buying enough Mercedes, BMWs, and Volkswagens.

Yields on ten-year German bunds hit close to an all-time low at -0.39%. The Euro (FXE) is looking at a breakdown through parity. The country’s largest financial institution, Deutsche Bank, is about to go under. No one here wants to touch equities there. It’s all about finding more bonds.

Soaring Chip Stocks took NASDAQ to new high. I have to admit I missed this one, not expecting a recovery until the China trade war ended. Chip prices are still falling, and volume is shrinking. We still love (AMD), (MU), and (NVDA) long term as obviously do current buyers.

Existing Home Sales fell off a cliff, down 1.7% in June to a seasonally adjusted 5.27 million units. Median Home Prices jumped 4.7% to $287,400. A shortage of entry-level units at decent prices get the blame. Ultra-low interest rates are having no impact.

JP Morgan (JPM) expects stocks to dive in Q3, driven by earnings downgrades for 2020. Who am I to argue with Jamie Diamond? Don’t lose what you made in H1 chasing rich stocks in H2. Everyone I know is bailing on the market and I am 100% cash going into this week’s Fed meeting up 18.33% year-to-date. I made 3.06% in July in only two weeks.

Alphabet (GOOGL) beat big time, sending the shares up 8% in aftermarket trading. Q2 revenues soared 19% YOY to an eye-popping $39.7 billion. It’s the biggest gain in the stock in four years, to $1,226. The laggard FANG finally catches up. The weak first quarter is now long forgotten.

Amazon (AMZN) delivered a rare miss, as heavy investment spending on more market share offset sales growth, taking the shares down 1%. Amazon Prime membership now tops 100 million. Q3 is also looking weak.

Intel (INTC) surged on chip stockpiling, taking the stock up 5% to $54.70. Customers in China stockpiled chips ahead of a worsening trade war. Q3 forecasts are looking even better. Sale of its 5G modem chip business to Apple is seen as a huge positive.

I've finally headed home, after a peripatetic six-week, 18-flight trip around the world meeting clients. I bailed on the continent just in time to escape a record heatwave, with Paris hitting 105 degrees and London 101, where it was so hot that people were passing out on the non-air conditioned underground.

Avoid energy stocks. The outcry over global warming is about to get very loud. I’ll write a more detailed report on the trip when I get a break in the market.

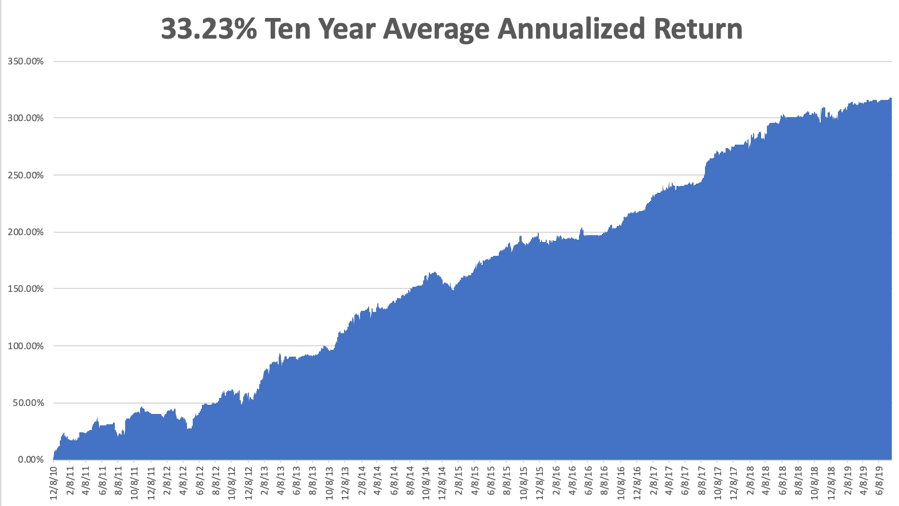

My strategy of avoiding stocks and only investing in weak dollar plays like bonds (TLT), foreign exchange (FXA), and copper (FCX) performed well. After spending a few weeks out of the market, it’s amazing how clear things become. The clouds lift and the fog disperses.

My Global Trading Dispatch has hit a new high for the year at +18.33% and has earned a robust 3.09% so far in July. Nothing like coming out of the blocks for an uncertain H2 on a hot streak. I’m inclined to stay in cash until the Fed interest rate decision on Wednesday.

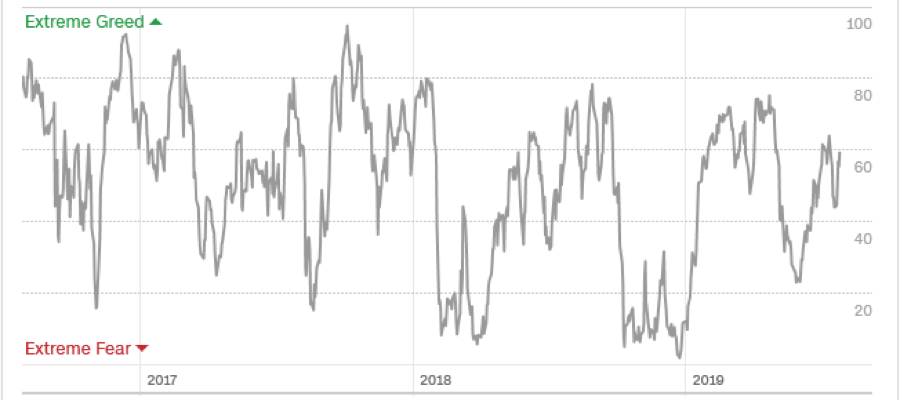

My ten-year average annualized profit bobbed up to +33.23%. With the markets now in the process of peaking out for the short term, I am now 100% in cash with Global Trading Dispatch and 100% cash in the Mad Hedge Tech Letter. If there is one thing supporting the market now, it is the fact that my Mad Hedge Market Timing Index has pulled back to a neutral 60. It’s a Goldilocks level, not too hot and not too cold.

The coming week will be a big one on the data front, with one big bombshell on Wednesday and the Payroll data on Friday.

On Monday, July 29, the Dallas Fed Manufacturing Index is out.

On Tuesday, July 30, we get June Pending Home Sales. A new Case Shiller S&P National Home Price Index is published. Look for YOY gains to shrink.

On Wednesday, July 31, at 8:30 AM, learn the ADP Private Employment Report. At 2:00 PM, the Fed interest rate decision is released and an extended press conference follows. If they don’t cut rates, there will be hell to pay.

On Thursday, August 1 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, August 2 at 8:30 AM, we get the July Nonfarm Payroll Report. Recent numbers have been hot so that is likely to continue.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, by the time you read this, I will have walked the 25 minutes from my Alpine chalet down to the Zermatt Bahnhoff, ridden the picturesque cog railway down to Brig, and picked up an express train through the 12-mile long Simplon Tunnel to Milan, Italy.

Then I’ll spend the rest of the weekend winging my way home to San Francisco in cramped conditions on Air Italy. Yes, I had to get a few more cappuccinos and a good Italian dinner before coming home.

Now, on with the task of doubling my performance by yearend.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

July 3, 2019

Fiat Lux

Featured Trade:

(CHIPS ARE BACK FROM THE DEAD)

(XLNX), (HUAWEI), (AAPL), (AMD), (TXN), (QCOM), (ADI), (NVDA), (INTC)