Global Market Comments

May 6, 2020

Fiat Lux

Featured Trade:

(NOW THE FAT LEADY IS REALLY SINGING FOR THE BOND MARKET),

(TLT), (TBT)

Global Market Comments

May 6, 2020

Fiat Lux

Featured Trade:

(NOW THE FAT LEADY IS REALLY SINGING FOR THE BOND MARKET),

(TLT), (TBT)

The most significant market development so far in 2020 has not been the epic stock market crash and rebound, the nonstop rally in tech stocks (NASDQ), the rebound of gold (GLD), or negative oil prices, although that is quite a list.

It has been the recent peaking of the bond market (TLT), which a few weeks ago was probing all-time highs.

I love it when my short, medium, and long-term calls play out according to script. I absolutely hate it when they happen so fast that I and my readers are unable to get in at decent prices.

That is what has happened with my short call for the (TLT), which has been performing a near-perfect swan dive since April. The move has been enough to boost me back into positive numbers for 2020.

The yield on the ten-year Treasury bond has soared from 3.25% in 2018 to an intraday low of 0.31% in March.

Lucky borrowers who demanded rate locks in real estate financings at the end of January are now thanking their lucky stars. We may be saying goodbye to the 3% handle on 5/1 ARMS for the rest of our lives.

The technical damage has been near-fatal. The writing is on the wall. A 1.00% yield for the ten-year is now easily on the menu for 2020, if not 2.00% or 3.0%.

This is crucially important for financial markets, as interest rates are the well spring from which all other market trends arise.

Wiser thinkers are peeved that the promised bleeding of federal tax revenues is causing the annual budget deficit to balloon from a low of a $450 billion annual rate in 2016 to $1.2 trillion last year and over $5 trillion in 2020.

Add in the bond purchases from the Fed’s new promise of $8 trillion in quantitative easing and you get true government borrowing of $13 trillion for 2020. It will all end in tears for bond and US dollar holders.

And don’t forget the president, who recently threatened to default on US Treasury bonds, just as the Treasury was trying to float $3 trillion in new issues. It is a short seller’s dream come true.

As rates rise, so does the debt service costs of the world’s largest borrower, the US government. The burden will soar in a hockey stick-like manner, currently at 4% of the total budget.

What is of far greater concern is what the tax bill does to the National Debt, taking it from $24 trillion to $32 trillion over the next year, a staggering rise of 50%. Even Tojo and Hitler couldn’t get the US to buy that much. If we get the higher figure, then we are looking not at another recession, but at yet another 1930-style depression.

Better teach your kids to drive for UBER early, as they are the ones who are going to have to pay off this gargantuan debt. That is if (UBER) is still around.

So what the heck are you supposed to do now? Keep selling those bond rallies, even the little ones. It will be the closest thing to a rich uncle you will ever have, if you don’t already have one.

Make your year now because the longer you put it off, the harder it will be to get.

Global Market Comments

May 4, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT BOTTOM IS THE ONE YOU BUY),

(SPY), (SDS), (TLT), (TBT), (F), (GM), (TSLA), (S), (JCP), (M)

It was only a year ago that I was driving around New Zealand with my kids, admiring the bucolic mountainous scenery, with Herb Albert and the Tijuana brass blasting out over the radio. Believe me, the tunes are not the first choice of a 15-year-old.

Today, it is all a distant memory, with any kind of international travel now unthinkable. For me, that is like a jail sentence. It is all a reminder of how well we had it before and how bleak is the immediate future.

Stock traders have certainly been put through a meat grinder. The best and worst months in market history were packed back to back, down 39% and then up 37%. At the March 23 low, the Dow average had fallen by 11,400 in a mere six weeks. Those who lived through the 1929 crash have lost their bragging rights, if there are any left.

However, like my college professor used to say, “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

Most of the index gains were achieved by just five FANG stocks. Virtually all of the gains were from “stay at home” companies taking in windfalls from cutting-edge online business models. The “recovery” had a good week, and that was about it.

The other obvious development is that if any business was in trouble before the health crisis, you can safely write them off now. That includes retailers like Sears (S), JC Penny’s (JCP), Macy’s (M), almost all brick-and-mortar clothing sellers, and the small and medium-sized energy industry.

The worst economic data points since the black plague are about to hit the tape. Some 30 million in newly unemployed is nothing to dismiss, and that number grows to 40 million if you include discouraged workers.

That is 25% of the workforce, the same as peak joblessness during the great depression. But $14 trillion in QE and fiscal stimulus is about to hit the market too.

Which brings us to the urgent question of the day: What to do now?

It’s a vexing issue because this is not your father’s stock market. This is not even the market we’d grown used to only six months ago. All I can say is that the virology course I took 50 years ago today is worth its weight in gold.

I think you would be mad not to count a second Covid-19 wave into your calculations. This could occur in weeks, or in months, after the summer respite. This makes a second run at the lows a sure thing. I don’t think we’ll make it, but a loss of half the recent gains is entirely possible.

That takes us back down to a Dow Average of 21,000, or an S&P 500 (SPX) of 2,400.

If you are a long term investor looking to rebuild your retirement nest egg, there are only two sectors left in the market, Tech and Biotech & Healthcare. Looking at anything else is both risky and speculative. So, if we do get another meltdown, these are the only areas you should target.

If I am wrong, the market will probably bounce along sideways in a narrow range for months. That is a dream scenario if you pursue a vertical bull and bear call and put option spread strategy that I have been offering up to followers for the past decade.

Pending Home Sales Were Down a Staggering 20.8% in March and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell. The way homebuilder stocks like (LEN) and (KBH) are trading, I’d say your home will be worth a lot more in a year when the huge demographic push resumes. I’m not selling.

The 60,000 peak in deaths proposed by the administration only weeks ago is now looking wildly optimistic. Their worst-case scenario of 200,000 deaths, the announcement of which set the March 23 bottom of the Dow Average at 18,200, is now likely.

It will take place when the epidemic peaks in the southern and midwestern states that never sheltered in place or went in late and are coming out early. That second wave may well create a second bottom in stock prices, and that is the one you jump into and buy with both hands.

US Corona Deaths topped 66,000 last week, more than we lost after a decade of the Vietnam War. Total cases exceed one million.

Bank of America sees negative 30% GDP this quarter annualized, so says CEO Brian Moynihan. His economists expect negative 9% in Q3 and plus 30% in Q4. Suffice it to say, this is the ultra-optimistic case. Q4 doesn’t include the millions of businesses that will disappear because the Paycheck Protection Plan is failing so badly. Most government aid will take three to six months to hit the economy.

US GDP crashed 4.8% in Q1, the worst quarter since the depths of the 2008 Great Recession. Q2 will be far worse. We are now officially in recession, which should last 3-4 quarters. But is it already in the price? Next week’s April Nonfarm Payroll report should be a real humdinger.

Ford (F) lost $5 billion in Q2, and there is no guidance about the future. Avoid (F) on pain of death. Late to electric, they may not make it this time. They’re still in the buggy whip business.

Weekly Jobless Claims topped 3.8 million, bringing the six-week total to a staggering 30 million, more than those lost at the peak of the Great Depression. Florida, California, and Georgia led with applications. This implies a U-6 Unemployment rate of 25% with next week’s April Nonfarm Payroll Report. And the Dow Average is up 37% since March 23?

The Bond Market crashed on a Trump threat to default on US Treasury bonds, of which China owns $900 billion. It’s Trump’s retaliation for the Middle Kingdom spawning the Coronavirus, which he calls the “Chinese virus.” The (TLT) dropped three points on the news. Good thing I am triple short a market that is about to get crushed by massive government borrowing.

A glut of imported autos is parked at sea, steaming in circles, awaiting a recovery in the US economy. They are no doubt finding company with imported oil tankers. So many unwanted cars coming in the land-based storage areas were overflowing. It’s tough to see (F) and (GM) recovering from this. Keep buying made in the USA (TSLA) on dips, which is headed to $2,500 a share.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years, up a blistering +8.05%. We are now only 6.67% short of a new all-time high. The 100 new subscribers who came in the previous week are sitting pretty and must think I’m some sort of guru.

My aggressive triple weighting in short bond positions came in big time when Trump threatened to default on US debt. My shorts in the S&P 500 (SPY) helped. I took profits on my last long there the previous week. (SDS), another short play, clawed back some losses.

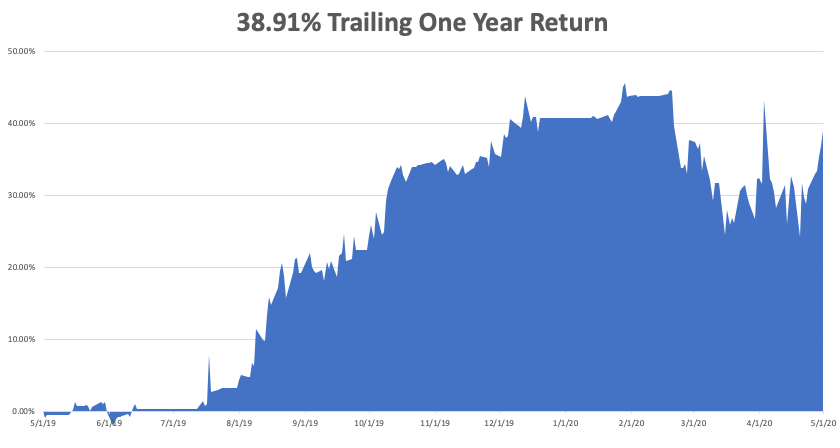

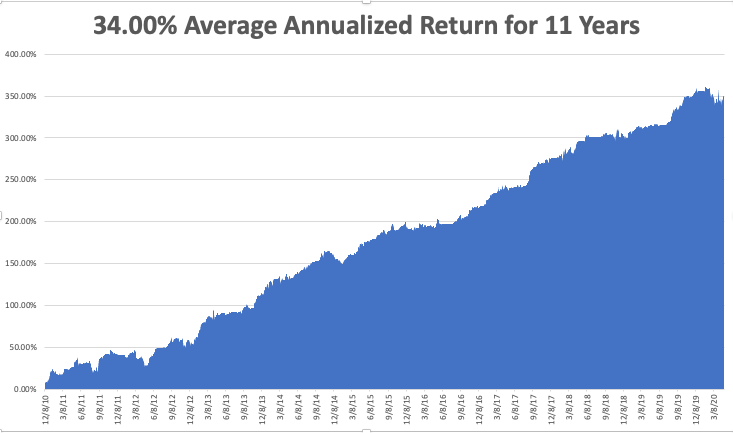

We closed out up a blockbuster +4.55% in April and May is up +2.11%, taking my 2020 YTD return up to only -1.75%. That compares to a loss for the Dow Average of -18.20% from the February top. My trailing one-year return returned to 38.91%. My ten-year average annualized profit returned to +34.00%.

This week, Q1 earnings reports continue and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 4 at 9:00 AM, the US Factories Orders for March are out and are expected to be disastrous. Berkshire Hathaway (BRK/B) and Eli Lilly (LLY) report.

On Tuesday, May 5 at 11:00 AM, the US Crude Oil Stocks are published and will be another bomb. Netflix (NFLX) and Coca-Cola (KO) report.

On Wednesday, May 6, at 7:15 AM, API Private Sector Employment Report is released. Lan Research (LRCX) and Electronic Arts (EA) announce earnings.

On Thursday, May 7 at 8:30 AM, another horrible Weekly Jobless Claims are out. Bristol Myers Squibb (BMY) reports.

On Friday, May 8, the April Nonfarm Payroll Report is printed, the worst unemployment rate since the Great Depression. AbbVie (ABBV) reports.

As for me, to battle cabin fever, I am setting up a tent in my back yard and staying there tonight, just to change the scenery. The girls need one more campout to qualify for camping merit badge, an important Eagle Scout one, and this will qualify.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With the May 15 options expiration only ten trading days away, there is a heightened probability that your short options position gets called away.

We have the good fortune of having a large number of deep in-the-money call and put options spreads about to expire at their maximum profit points, five to be precise.

If that happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position with less risk. You just won the lottery, literally.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money put option spread, it contains two elements: a long put and a short put. The long put you own, but the short put can get assigned, or called away at any time and delivered to its rightful owner.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it.

All you have to do was call your broker and instruct him to exercise your long position in your May puts to close out your short position in the May puts.

Puts are a right to sell shares at a fixed price before a fixed date, and one option contract is exercisable into 100 shares.

Sounds like a good trade to me.

Weird stuff like this happens in the run-up to options expirations.

A put owner may need to sell a long stock position right at the close, and exercising his long Put is the only way to execute it.

Ordinary shares may not be available in the market, or maybe a limit order didn’t get done by the stock market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, puts even get exercised by accident. There are still a few humans left in this market to blow it.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Global Market Comments

April 20, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT’S A FED PUT WORTH?),

(INDU), (SPX), (TLT), (ZM), (TDOC),

(NFLX), (UAL), (WYNN), (CCL)

What is a Fed put worth?

That the question that traders and investors alike are pondering.

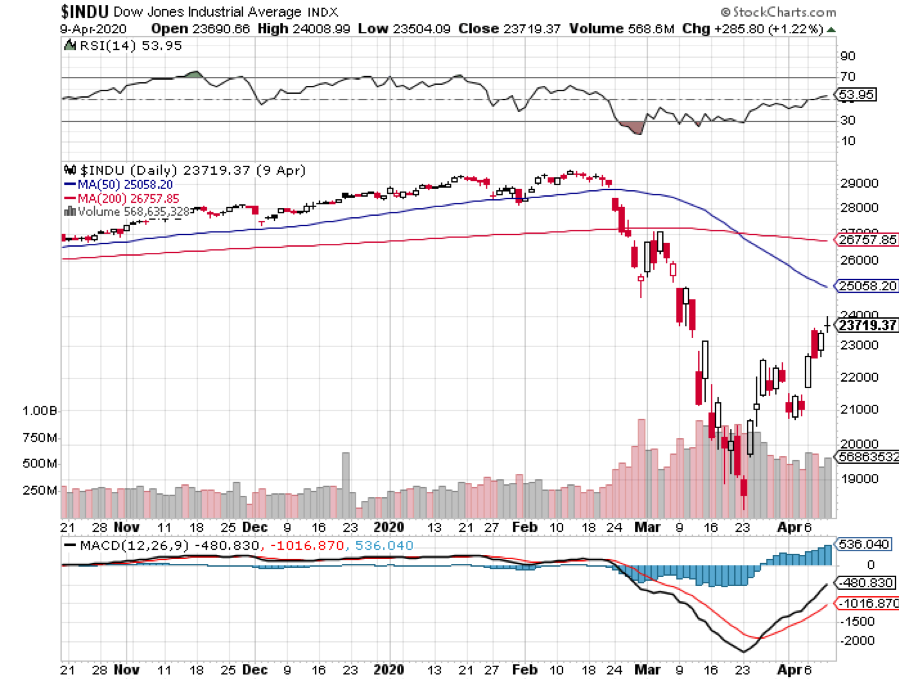

If the government had taken no action whatsoever in the face of the Corona pandemic the Dow average would easily be at 15,000 today, if not 12,000.

After all, the economic collapse we have seen has been even greater than the Great Depression. More than 22 million unemployed in four weeks? Back then, the Dow Average fell by 90%.

Enter the Feds.

Throw in $6 trillion in expected fiscal spending and $8-$0 trillion in Federal Reserve stabilization of the money markets and quantitative easing, and it makes a heck of a difference. As a result, the national debt will rocket from $23 trillion to at least $32 trillion by next year, a far faster increase than seen after Pearl Harbor.

Stocks love this.

In the past three weeks, the Dow Average has jumped an eye-popping 35% from 18,000 to over 24,000. We are likely trading at 25 X 2020 earnings, but that is just a guess at best. Nobody knows, with essentially all companies withdrawing guidance. On a valuation basis, stocks are now more expensive than at any time since 1929.

You can be excused for being confused, befuddled, and gob-sacked.

All of this adds up to a value of the Fed put of 9,000 in Dow Average terms, 17,000 in a worst-case scenario, and 27,000 if you want to go back to 1933 share valuations.

Stocks here are now priced for perfection. To buy shares here, you are making the following rosy assumptions:

1) The Corona epidemic is peaking and it is clear sailing from here.

2) Shelters-in-place ends in two weeks.

3) Critical shortages of medical supplies end.

4) US Deaths top out at 60,000 from the current 40,000, the most optimistic White House forecast.

4) Business will immediately bounce back to pre-epidemic levels

5) Domestic and international travel resume immediately

If all of the above take place, then at a stretch, shares are justified at maintaining current levels and will churn sideways from here.

Here is what is more likely:

1) We are nowhere close to a peak, especially in states that never sheltered-in-place, and there could be a secondary peak in the fall. At 2,000 a day, US deaths will easily top 100,000 in a month.

2) Shelters-in-place will extend to June in the most populous states.

3) Medical supply shortages will continue for the indefinite future, with 50 states bidding against each other to buy fake masks from China.

4) Dozens of large companies and perhaps a quarter of the country’s 30 million small businesses will go bankrupt before the recovery begins.

5) There is no sign that domestic and international travels are getting off the runway anytime soon.

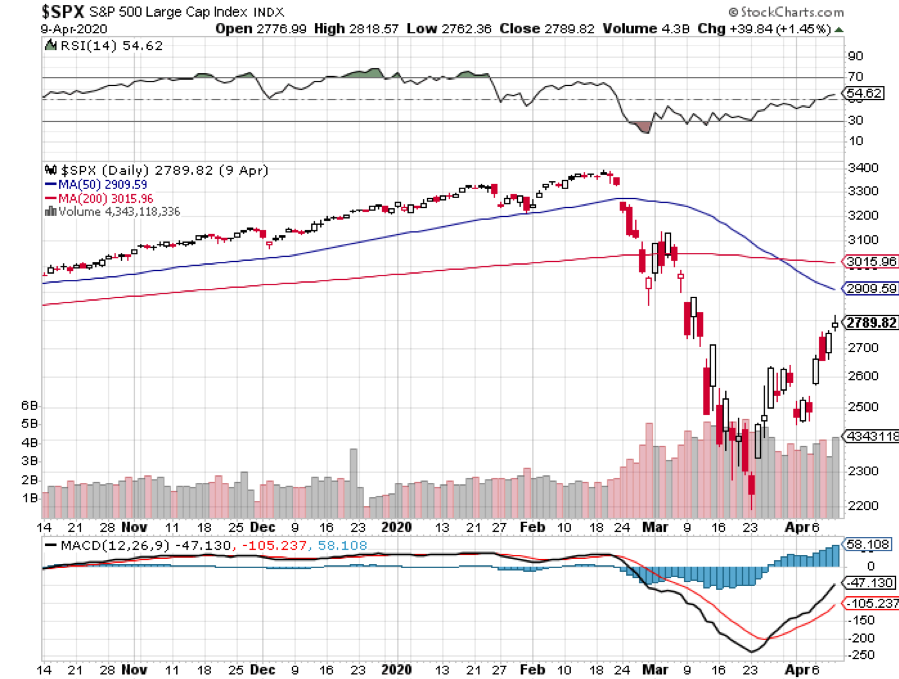

If that is the case, then stocks here that are wildly overpriced are due for a retest of the Dow 18,000 and (SPX) 2,400 lows.

No matter what happens, traders should be cognizant of an enormous bifurcation of the market that has taken place.

Stay at Home stocks, like Zoom (ZM), Teladoc (TDOC), and Netflix (NFLX), have spectacularly outperformed the market. Many of these had already been recommended by the Mad Hedge Technology letter and the Mad Hedge Biotech & Healthcare letter because they were leaders in their own technologies (click here).

The problem with these companies is that they are all expensive, in some cases trading at hundreds of times their earnings.

Then there are the Reopening Stocks that will deliver outsized returns once we make it to the downslope of the epidemic. These include United Airlines (UAL), Wynn Hotels (WYNN), and Carnival Cruise Lines (CCL), which we heavily sold short near the market top, and led the recovery of the last three weeks.

The problem with these companies is that they may have to go bankrupt first, or at least accept a heavy government ownership and dilution of existing shareholders before they return to normal.

It’s a quandary that would vex Solomon.

I always tell people, if you want to make an easy, reliable, and safe living, get a job at the Post Office. Avoid the stock market.

OPEC cut oil production by 10 million barrels/day, for two months, and then 8 million barrels a day for the rest of the year. Oil prices plunged anyway to a 20-year low at $18.50 a barrel, as it only puts a small dent in the 34 million barrel a day oversupply. It only postpones the day when many energy companies go bankrupt.

The Economy could be turning on and off for 18 months, believes Fed governor Neil Kashkari. He may be partly right. I am expecting two Coronavirus waves to lead to two shutdowns in the spring and fall, and the stock market may reflect the same. If so, stocks are wildly overpriced here, and the bear market could last another year. Sell shorts, or at least add hedges, and buy the (SDS).

US Budget Deficit to top $3.8 trillion this year, the most since WWII. We were already headed for a monster $1.5 trillion in red ink before the virus hit. Now we are pouring gasoline on the fire. It'sis my worst-case scenario, I had the national debt rising from $23 trillion today to $30 trillion in a decade. It looks like that will happen by next year.

Only 90,000 cleared US airport security in one day, down from a typical 2.2 million, or down 95%. It appears that 90,000 people a day don’t care if they get Covid-19 or have already had it. Some 80% of all flights globally are grounded, with many countries now stranded. With massive debt loads, it is only a question of how soon the big US airlines go bankrupt and how much the government gets to own on the way back up. Don’t buy any airlines no matter how cheap they get.

US Retails Sales collapsed by 8.7% as the paycheck-free economics takes hold. The March Empire State Manufacturing Index crashed to a record low of 78% and March Industrial Production is off 5.4%, the lowest since 1946. The parade of the worst economic data in history has begun. And we go into this with stocks at record high valuations, more expensive than they were in January.

Goldman Sachs says this depression will be four times worse than the Great Recession of 2008-2009, likely falling 35% annualized in Q2. Unemployment will hit 15% or higher, but stocks will not retest the March lows. The bounce back in H2 will be bigger than any seen. It more or less corresponds to my view. They must have some smart people at (GS).

March Homebuilder Confidence brings the biggest crash in history, down 42 points to a reading of only 30. It's the greatest decline since the 35-year history of the index. The last time we were this low was in June 2012. Some 21% of builders are reporting virus disruption.

Housing Starts collapsed a stunning 22.3% in March, the worst one-month figure ever recorded. Social distancing makes open houses impossible. But this will be one sector that leads us out of the depression. There is still a chronic generational housing shortage.

Weekly Jobless Claims topped 5.1 million, taking the grim four-week tally to a staggering 21 million. Out of the frying pan, into the fire.

Gilead Sciences (GILD) drug sent stocks soaring, up 900 points overnight. Its Remdesivir brought rapid recovery in already infected patients at the University of Chicago in a phase three trial. The market is hypersensitive to any good Corona news. Sell into the rally.

China GDP took a 6.8% hit in Q1 as the Corona pandemic takes its toll. Services are recovering faster than manufacturing, which is why the smog has not come back yet. And international trade has ground down to zero. Public transit has been abandoned for private cars. It could be a preview to our own recovery.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $18 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance recovered nicely this week, thanks to some frenetic trading. I used the Monday 700-point dive in the market to cover most of my bearish positions and add short-dated longs in Apple (AAPL) and Facebook (FB).

Finally, I dove back into selling short the US bond market on the assumption that unprecedented borrowing will destroy prices.

My short volatility positions (VXX) were hammered again, even though volatility declined on the week. There seems to be heavy short selling of deep out-of-the-money puts on the assumption that the Volatility Index (VIX) won’t rise above $50 again.

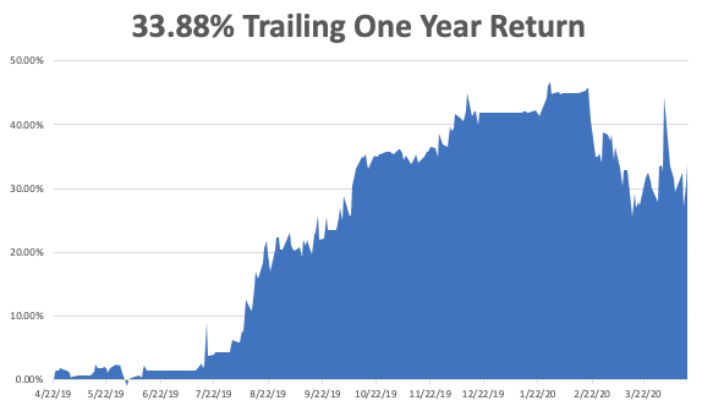

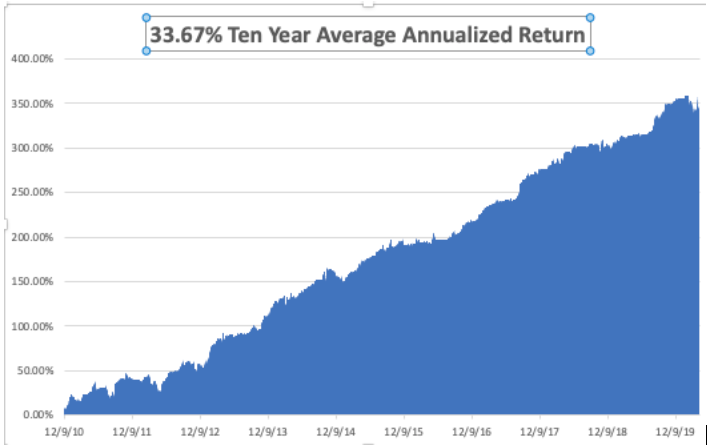

We are now up +0.45% in April, taking my 2020 YTD return down to -7.97%. That compares to a loss for the Dow Average of -15% from the February top. My trailing one-year return returned to 33.88%. My ten-year average annualized profit returned to +33.67%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, April 20 at 7:30 AM, the Chicago Fed National Activity Index comes out.

On Tuesday, April 21 at 9:00 AM, the March Existing Homes Sales are released.

On Wednesday, April 22, at 9:30 AM, the Cushing Crude Oil Stocks are announced.

On Thursday, April 23 at 8:30 AM, Weekly Jobless Claims will announce another blockbuster number.

On Friday, April 24 at 7:30 AM, US Durable Goods for March are printed. The Baker Hughes Rig Count follows at 2:00 PM. Expect these figures to crash as well.

As for me, I am sitting here eating a pineapple upside-down cake that my daughter just whipped up. It's my favorite cake made by my mother, which I always got on my birthday.

Of course, I have to wash the dishes. If anyone wants to supplement their trading income, housekeeper and domestic and wants to live in mansions at Lake Tahoe and San Francisco, please contact customer support immediately.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 14, 2020

Fiat Lux

Featured Trade:

(APRIL 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (SPY), (SDS), (BA), (VIX), (VXX), (GLD), (GDX),

(GOLD), (NEM), (QCOM), (HYG), (JNK)

(WHY SENIORS NEVER CHANGE THEIR PASSWORDS)

Global Market Comments

April 13, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE BEAR MARKET RALLY IS OVER),

(INDU), (SPX), (TLT), (VIX, (VXX), (GLD), (JPM), (AMZN), (MSFT)

The Bear market rally is over, or at least that’s what Asian stock futures are screaming at us, and the shorts are piling back on….again.

For the first time in 16 years, I did not have to get up at 6:00 AM to hide Easter eggs. It’s not because my kids don’t believe in the Easter Bunny anymore. They’ll believe in anything that delivers them a free chocolate bunny. It’s because I couldn’t get any eggs. Much of the country’s egg production is being diverted into vaccine production for testing, of which, along with antivirals, there are more than 300 worldwide.

Enough of the happy talk.

It was a classic bear market rally we saw over the past two weeks in every way, retracing 50% of the loss this year. Junk stocks, like hotels, airlines, and cruise lines led, while quality big tech lagged. That’s the exact opposite of what you want to see for a new bull market.

At the Friday high, the Dow (IND) was down only 17% from the February all-time high at a two-decade 20X valuation high.

The US is now losing 2,000 citizens a day to the Coronavirus. That’s how many we lost at the peak of the Vietnam War in a month. We are suffering another 9/11 every day of the week.

More than 16.8 million have lost jobs in three weeks, more than all those gained in six years. Of all American companies with fewer than 500 employees, 54% have closed! JP Morgan (JPM) has just cut its forecast for Q2 GDP from a 25% loss to an end of world 40% decline on an annualized bases.

New York is losing 800 people a day and is burying many of them in mass graves. Bread lines have formed in countless major cities. And you think 17% is enough for a discount for stocks, given that a near-total shutdown will continue for another five weeks?

Are you out of your freaking mind?

Which leads me to believe that another retest in the lows is in the work, no matter how much government money is headed our way.

For a start, it will be three months before the Fed handouts show any meaningful impact on the economy. Second, we are due for a second wave of the virus in the fall, once the initial shelter-in-place ends. Markets will likely behave the same.

In the meantime, long term analysts of the global economic structure are going dizzy with possible permanent changes. I am in the process of writing a couple of pieces on this if I can only get away from the market long enough to do so.

It seems like half the country has lost their jobs, while the other half are now working double time without pay, like myself.

The market was stunned by 6.1 million in Weekly Jobless Claims, taking the implied Unemployment Rate to over 14%, more than seen during the 2008-2009 Great Recession. One out of four Americans will lose their jobs or suffer a serious pay cut in the next two months. At this rate, we will top the Great Depression peak of 25 million in two weeks.

The Fed launched a second $2.3 trillion rescue program, this time lending to states, local municipalities, and buying oil industry junk bonds. More money was made available to small businesses. Jay Powell is redefining what it means to be a central bank, but no one is complaining. It was worth one 500-point rally in the Dow Average, which we have already given back. At this point, almost the entire country is living on welfare.

Stocks soared firefly on falling death rates. Chinese cases are falling after the border closed, Italy and Madrid are going flat, and San Francisco is looking good. There is still a massive, but extremely nervous bid under the market. I’m selling into this rally. We will continue to chop in a (SPX) $2180-$2800 range for the foreseeable future.

Trump says there’s a light at the end of the tunnel, but he doesn’t tell you that the light is an oncoming express train. At the very least, the number of deaths will rise at least tenfold from here. That’s how many we lost in the Korean War. It hasn’t even hit the unsheltered states in the Midwest yet.

Gold (GLD) is making a run another all-time highs, topping $1,700. Expect everyone’s favorite hedge to go ballistic. QE infinity and zero interest rates will eventually bring hyperinflation and render the US dollar worthless. Gold production is falling due to the virus. Anything else you need to know?

Mortgage defaults are up 18-fold. People can’t even get through to their banks to tell them they are not going to pay. This is the next financial crisis. Fannie Mae and Freddie Mac are going to go broke….again.

Can the US government spend money fast enough, given that it has been shrinking for three years? I’m not getting my check until September. It’s not easy to spend $2 trillion in a hurry. I can’t even spend a billion in a hurry. It’s darn hard and I’ve tried. It suggests any recovery will be slower and lasts longer.

Here’s the bearish view on the economy, with Barclay’s Bank looking for an “L” shaped recovery, which means no recovery at all. I’m looking more for a square root type recovery, which means a sharp bounce back to a lower rate of growth. And there may be two “square roots” back to back.

Bond giant PIMCO predicts 30% GDP loss in Q2 on an annualized basis. Everyone staying home doing jigsaw puzzles isn’t doing much for our economic growth. This may end up becoming the most positive forecast out there.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $20 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had a tough week, destroying my performance back to positive numbers for the year. That is thanks to my piling on the shorts in a steadily rising market. This brings short term pain, but medium-term ecstasy.

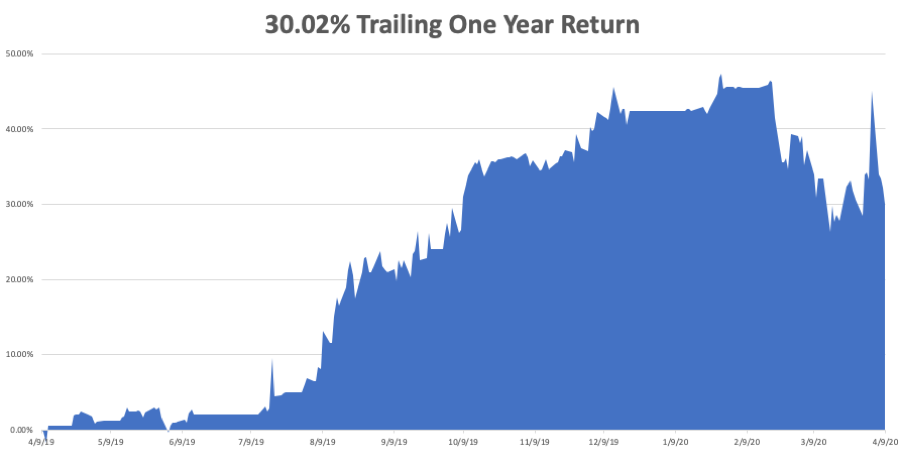

We are now down -3.99% in April, taking my 2020 YTD return down to -12.41%. That compares to an incredible loss for the Dow Average of -17% from the February top. My trailing one-year return sank to 30.02%. My ten-year average annualized profit was pared back to +33.51%.

My short volatility positions (VXX) were hammered even in a rising market, which means no one believes the rally, including me.

I took nice profits on two very deep in-the-money, very short dated call spreads in Amazon (AMZN) and Microsoft (MSFT), the two safest companies in the entire market, betting that we don’t go to new lows in the next nine trading days. As the market rose, I continued to add to my short position with the 2X ProShares Ultra Short S&P 500 (SDS).

This week, we get the first look at Q1 earnings. All economic data points will be out of date and utterly meaningless this week. The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, April 13 Citigroup (C) and JP Morgan (JPM) report earnings.

On Tuesday, April 14 at 11:30 AM, the API Crude Oil Stocks are announced.

On Wednesday, April 15, at 2:00 PM, the New York State Manufacturing Index is released.

On Thursday, April 16 at 8:30 AM, Weekly Jobless Claims are announced. The number could top 6,000,000 again. At 7:30 AM, US Housing Starts for March are published.

On Friday, April 17 at 7:30 AM, the Baker Hughes Rig Count is released at 2:00 PM. Expect these figures to crash as well.

As for me, before the market carnage of the coming week ensues, I shall be sitting down with my kids and touring the National Gallery of Art in Washington DC. Many art museums have now opened up their collections online, for free. There is a special exhibition of “Degas at the Opera.” Please enjoy by clicking here.

Next to come will be the Louvre in Paris (click here), and the National Museum of the Marine Corps in Triangle, VA (click here). I have them tracing the dog tags I brought back from Guadalcanal. I bet some of my old weapons are in there.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader