Finally, the economy is starting to deliver the blockbuster numbers that I have been predicting all year.

The 321,000 gain in the November nonfarm payroll on Friday wasn?t just good, they were fantastic, truly of boom time proportions. It was the best report in nearly three years. The headline unemployment rate stayed at 5.8%, a seven year low.

It vindicates my ultra bullish view for the US economy of a robust 4% GDP growth rate in 2015. It also makes my own out-of-consensus $2,100 yearend target for the S&P 500 a chip shot (everybody and his brother?s target now, but certainly out-of-consensus last January).

There has been a steady drip, drip of data warning that something big was headed our way for the last several months. November auto sales a 17 million annualized rate was a key piece of the puzzle, as consumers cashed in on cheap gas prices to buy low mileage, high profit margin SUV?s. The Chrysler Jeep Cherokee, a piece of crap car if there ever was one, saw sales rocket by a mind-boggling 60%!

It reaffirms my view that the 40% collapse in the price of energy since June is not worth the 10% improvement in stock indexes we have seen so far. It justifies at least a double, probably to be spread over the next three years.

It also looks like Santa Claus will be working overtime this Christmas. Retailers are reporting a vast improvement over last year?s weather compromised sales results. A standout figure in the payroll report was the 50,000 jobs added by the sector. This is much more than just a seasonal influence, as FedEx and UPS pile on new workers.

The market impact was predictable. Treasury bond yields (TLT) spiked 10 basis points, the biggest one-day gain in four years. My position in the short Treasury ETF (TBT) saw a nice pop. Unloved gold (GLD) got slaughtered, again, cratering $25.

Stocks (SPY) didn?t see any big moves, and simply failed to give up their recent humongous gains once again. A major exception was the financials (XLF), egged on by diving bond prices. My long in Bank of America (BAC) saw another new high for the year.

All in all, it was another good day for followers of the Mad Hedge Fund Trader.

To understand how overwhelmingly positive the report was, you have to dive into the weeds. Average hourly earnings were up the most in 17 months. The September payroll report was revised upward from 256,000 to 271,000, while October was boosted from 214,000 to 243,000.

Professional and business services led the pack, up a whopping 86,000. There are serious, non minimum wage jobs. Job gains have averaged an impressive 278,000 over the last three months.

The broader U-6 unemployment rate fell to 11.4%, down from 12.7% a year ago. Most importantly, wage growth is accelerating, and hours worked are at a new cyclical high.

In view of these impressive numbers, it is unlikely that we will see any substantial pullback in share prices for the rest of 2014. For that, we will have to wait until 2015.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Rosie-the-Riverter.jpg353306Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-08 09:28:162014-12-08 09:28:16The November Nonfarm Payroll Report is a Game Changer

Any doubts that my bullish call on global risk markets would play out as promised were blown away on Friday.

That was when the central banks of China and Europe delivered a surprise, one two punch of monetary stimulus for their own troubled economies. The quantitative easing baton has successful been passed from America?s Federal Reserve to central bankers abroad.

The net net for you and I is that stocks and the dollar will continue to appreciate.

Specifically, China came out of the blue with a 0.4% interest rate cut, thus stimulating the world?s largest emerging market.

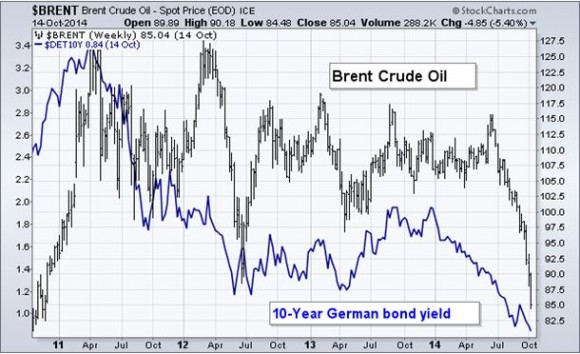

Then the European Central Bank?s president, Mario Draghi, said he would take whatever steps necessary to return the continent to a 2% inflation rate, up from today?s 0.40%. Unbelievably, Spanish ten-year bond yield fell below 2% in a heartbeat and German ten year funds pierced 0.80%.

For good measure, the Japanese central bank then chimed in, boosting the country?s money supply growth by 33% as promised earlier. Saying is one thing, but doing it is much better, especially when it carries a radical tinge.

The measures make my 2,100 target for the S&P 500 by the end of December a pretty safe bet. Look for a tedious, prolonged sideways grind, followed by rapid headline driven pop. Easy entry points will be few.

It really is one of those ?Close your eyes and buy? type of markets. I doubt we get pullback of less than 3% in the major indexes this year. Volatility will remain muted. All the black swans of landed.

It gets better.

This kind of market action could continue for another three years. After the ?Great Recession?, we are now witnessing the ?Great Recovery?. That means returning to a 3% or better GDP growth rate and 10% annual corporate earnings increases.

Add in 2% a year in dividend yields, and you get a (SPY) that rises by 10% a year. Look at the 100-year average gain for stocks and it comes in remarkably close to this number. Factor in an earnings multiple increase from the current 16, and they will rise faster.

This is all Goldilocks on steroids. Interest rates, the cost of labor, energy, and commodity price inputs stay low, earnings rise, and everybody else in the world sends their money here because it is the best bet going.

I all works for me, and I hope, you too!

It All Works for Me!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-25 01:05:412014-11-25 01:05:41The Yearend Melt Up Has Started!

?Be Fearful When Others Are Greedy, and Greedy When Others Are Fearful.?

That is one of my favorite quotes from Oracle of Omaha, Warren Buffet, and it was never more true than during the past 30 trading days.

It turns out that the lowest risk day to buy stocks in 2014 was October 15, when we saw a giant, capitulation, spike low in the S&P 500 (SPY) down to $182.

That was the most fearful day I can recall over the last three years. You wouldn?t believe how many people I begged not to sell out entire portfolios that day!

So where are we now with the markets? Go back to the beginning of that legendary quote, and the word ?fearful? really stands out.

That means traders are stuck right back in the uncomfortable position in which they have spent most of this year.

Do I try to play catch up here and chase the market for a few extra basis points of performance, even at the risk of enduring another calamitous selloff? Or do I sit here in cash and earn precisely zero and get fired at the end of the year?

It is a choice that would truly vex Salomon. But as a king, at least he had job security.

We are now entering the tag ends of 2014, with only 36 trading days left, including three half days. I think it is safe to say that the trends that have predominated since January 1 will continue. Expect markets to continue to over reward risk takers and over punish risk avoiders.

That means there are only three trades in the world to execute:

1) Buy the US Dollar

A yield advantage for the greenback is sucking in capital from all over the world. Concerns about principal risk is a further driver, creating a ?flight to safety? of prodigious proportions. Thanks to the collapse in energy prices and a ramp up in US domestic production, dollar outflows from America are at decade lows.

This can only mean that we are at the beginning of a multi year bull market in the buck. Sell short the Japanese yen (FXY) and the Euro (FXE), and buy the 2X short yen ETF (YCS), and the 2X short Euro ETF (EUO).

2) Buy US Stocks

The majority of US portfolio managers are still underweight stocks and are desperately trying to get in. Now that the 10% correction is finally behind us, they can afford the luxury of being more aggressive loading up on the dips.

The midterm elections, which saw the Republicans take control of the Senate with a seven seat gain, is a new turbocharger for equities. Congress is now seen as pro business. Since the stock market tripled and corporate profits rocketed with an anti business elected body, imagine how well they will do with a friendly one!

I was hoping for the Senate results to get tied up in runoffs and the courts for a couple of months, triggering a 5% market correction and an opportunity to load the boat once more. It was not to be. What is left for us now is to see the (SPX) grind up to close the year at a 2100 all time high.

Who will be the sector leaders? The usual suspects who have led the charge all year, technology, health care, and financials.

3) Sell Short All Commodities

It is truly impressive to see the entire commodity space collapse all at the same time. This includes oil, natural gas, gold, silver, copper, corn, wheat, soybeans, and the commodity producing currencies of the Australian and Canadian dollars.

They have all been hard hit with a perfect storm; overwhelming supply of product, a strong dollar, and weak demand caused by a slowing global economy. The story is the same everywhere.

Commodity collapses always last longer and deeper than you imagine possible because you cannot turn off production by simply flipping a switch, as you can with the paper assets of stocks and bonds. Cutting off supplies means freezing capital spending worth hundreds of billions of dollars spread over decades, no easy task.

So, before you purchase a hard asset of any kind, lie down and take a long nap first. And please stop emailing me asking if this is the bottom for all of the above. It isn?t.

4) Sell All Bonds

There is a fourth secular trend that began exactly on October 15, right after the market opening. The ten year Treasury bond (TLT) hit a yield of 1.86%. This is a secondary low in yields, high in prices, after the 1.39% yield we saw in 2012. This means we are now two years into a 30-year bear market for all fixed income securities.

However, don?t expect a crash like we saw during the 1970?s, when yields soared up to 13%. Expect a slow grind up in interest rates, often spending 3-6 months in tedious, narrow, sleep inducing ranges.

This makes your entry points on the short side important. Only buy the short Treasury bond ETF (TBT) on substantial dips, lest hair starts growing on the position.

There is one other alternative if you have been following the Trade Alerts of the Mad Hedge Fund Trader all year.

Quit trading and take the rest of the year off. Start your Christmas shopping early. Contribute to retail sales and the national GDP. You earned it. The 42% profit you have earned so far is of heroic proportions.

Let?s hope for more of the same in 2015!

https://www.madhedgefundtrader.com/wp-content/uploads/2011/10/johnthomas00.png378251Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-07 01:04:292014-11-07 01:04:29How to Trade the Rest of 2014

Those who woke up early Friday morning may be forgiven for blinking at their screens quite a few times.

The Japanese yen (FXY), (YCS) was down by an incredible 3%, the Dow Average futures were trading at an all time high of $17,400, and the S&P 500 was just short of a new peak at $202.

The Japanese stock market blasted 5% to the upside, taking the Wisdom Tree Japan Hedged Equity ETF (DXJ) up a staggering 8%.

Was this a trick or treat?

It only took a few seconds for me to learn that this was all in reaction to bold moves announced by the Bank of Japan overnight. In one fell swoop, they boosted their target for monetary expansion this fiscal year from Y60 trillion to Y80 trillion, an instant gain of 33%, or $200 billion.

Prorate this number for the difference in out two nations? GDP?s, and that is like the Federal Reserve announcing a new $700 billion monetary stimulus program out of the blue. Quantitative easing is not dead. The baton has merely been passed from the US to Europe and Japan.

The bottom line for us? Asset prices everywhere go higher.

Of course, readers of the Mad Hedge Fund Trader knew all this was coming.

While taking profits yesterday on my Japan yen put spread, I cautioned holders of the ProShares Ultra Short Yen ETF (YCS) to hang on because the beleaguered Japanese currency was headed much lower.

Those who did so were richly rewarded with a one-day pop of $4.50 overnight to $79.50, an all time high.

Parsing through the BOJ statement, it?s clear that these spectacular, once a decade moves were justified.

When the Japanese government implemented a poorly conceived tax increase in April, the BOJ sat on its hands.

After sleeping through most of the year, the hand of Japanese central bank was finally forced by simultaneous weakness in Europe. It is now implementing the Fed QE policy lock, stock, and barrel, given the proven excellent results here in the US. They are only five years late!

An even bigger blockbuster was another announcement made by Japan?s government controlled Pension Investment Corp. that it was totally reshuffling its massive $1.2 trillion investment portfolio.

It is doubling its allocation to international equities from $150 billion to $300 billion. Given the dire conditions in Europe, you can count on most of that money going into the US stocks. That explains our gap up in the (SPX) this morning, and a similar move down in bonds (TLT), (TBT).

Here is their new Model Portfolio:

Domestic Bonds 35% Domestic Stocks 25% International Stocks 25% International Bonds 15%

Total 100%

The net effect of all of this is to effect an epochal move out of bonds and into stocks, and also to increase international investments at the expense of domestic ones.

I believe this is the beginning of a prolonged world-wide investment trend.

The bottom line for us traders here is that the Japanese action opens up the possibility of an entire ?RISK ON? leg upward. This is occurring on top of one of the sharpest legs up in market history.

All of a sudden, my yearend target of $2,100 for the S&P 500 is firmly back on the table. If you have any outstanding short positions on your books, it is better to cover them at the earliest opportunity.

Tally Ho!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Risk-e1414788138459.jpg201400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-03 01:06:022014-11-03 01:06:02Japanese Yen Melts Down to 12-Year Low!

The talking heads on TV have been working overtime speculating on where the worst move down in the stock market in three years will take us.

It all may sound like intelligent prognosticating to you.

As for me, I know they are guessing.

So I shall share with you my ten benchmark indicators that you can closely track to decide for yourself whether stocks are headed for perdition, or are soaring skyward once again.

1) Ten year Treasury bond yields start to rise, and break out above 2.30% (they are now at 2.18%).

2) The US dollar begins to appreciate once again, taking the Euro ETF (FXE) below $125.

3) Inflation expectations start to rise in Europe. Watch the monthly CPI numbers out of France and Italy, which have recently been negative.

4) Fed funds futures start to rise from near zero.

5) The price of crude oil stabilizes. Watch Brent, which will have the sharpest move up once recovery begins.

6) The small cap index, the Russell 2000 (IWM), starts to outperform the S&P 500 (SPY) on the upside. Smaller companies led the retreat on the downside, and should lead a new recovery as traders like me cover shorts (I already have).

7) Cyclical stocks, like airlines (DAL) outperform defensive stocks like soap and shampoo makers (PG) we already captured this with a (DAL) Trade Alert.

8) The junk bond market (HYG) starts to appreciate.

9) The macro data stream delivers a series of positive numbers.

10) People quit talking about the market bottom, and start opining about the next market top.

As you have probably figured out buy now with my flurry of recent Trade Alerts, I am leaning towards the probability that the bottom for stocks is already in. It?s all about oil.

I spent my weekend running numbers on the impact that cheap energy will have on the economy, and they are truly staggering. I list a few points below:

1) If oil stays down in this area, it will deliver a savings of $12,000 per family in gasoline, heating bills (being from California, I have only heard about these) and electricity.

2) The increased spending this will generate will add 1% to US GDP growth next year, as the cost of energy is pervasive through all industries, either directly, or indirectly.

3) This amounts to a $1.1 trillion stimulus package for the US economy, larger than the one we got in 2009. Think of it as a QE 4.

I rest my case.

Watch the Signs (My Infrared Picture)

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Infrared-Picture.jpg296400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-21 01:05:192014-10-21 01:05:1910 Signs of a Market Bottom

I have an arrangement with several large hedge funds where they pay me a small fortune every month for the privilege of calling me one day a year.

Wednesday was that day.

It was a day when the $20 billion hedge fund waited on hold while I got off the phone with the $100 billion hedge fund. And that?s not including urgent calls from the White House, the office of the Joint Chiefs, and the Federal Reserve.

Of course, no one needs to tell these guys how to chew gum. They were interested to know if they were missing anything.

The advice I gave them was very short and simple: ?Keep your eye on the economic data, and ignore everything else.?

You can palpably feel the tension when enduring crisis like these. The Internet noticeably slows down. Transatlantic and Transpacific phone lines get clogged up. Traffic on our website, www.madhedgefundtrader.com, rises tenfold.

So do plaintive emails from followers, everyone of which I attempt to answer quickly. To save time, I will give a generic answer to all of you in advance: ?No, it is not time to stop out of your ProShares Ultra Short 20+ Treasury Bond ETF (TBT) position at the $46 handle.? We are at a multiyear peak in bonds, and this is absolutely not the place to puke out. That?s why I always keep my positions small.

You have to allow room for markets to breathe and still be able to hang on when it goes against you. It is also nice to have the dry powder to double up.

I know some of you are suffering from sleepless nights, so I?ll make it easy for you. We have hit bottom for the year. This is the best time in three years to buy stocks, just in case you forgot to load up at any time since 2011. Ditto for bonds on the sell side.

Earnings started coming out last week, and many companies have been delivering blockbuster reports, as I expected. Over all, I think we can expect total S&P 500 earnings to rise by $11.

This means that, given the market?s recent 10% plunge, stocks are now selling at 12.5 X 2015 earnings. That is a rare bargain. It is a chance to buy shares at 2011 valuations. Don?t blink and miss it.

The big driver hasn?t been the Ebola virus, the risk of which has been wildly exaggerated by the media, but the collapse of the price of oil.

I think we got very close to a bottom of the entire move this morning when we tickled $80. I take North Dakota fracking pioneer John Hamm?s view: If this isn?t the bottom, it is close, and wherever the bottom, we will race right back up to $100 sometime next year on China?s insatiable demand.

That means you buy stocks right now.

For a fuller explanation of the fundamentally bullish argument for the stock market, please click here?10 Reasons Why the Bull Market is Still Alive?.

Now Is the Time to Have a Gunslinger Working on Your Behalf

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/John-Thomas-Young-Man-Armed-e1413493245303.jpg400282Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-17 01:05:252014-10-17 01:05:25The Bottom Building Process Has Begun

When I was a young, clueless investment banker at Morgan Stanley 30 years ago, the head of equity sales took me aside to give me some fatherly advice. Never touch the airlines.

The profitability of this industry was totally dependent on fuel costs, interest rates and the state of the economy, and management hadn't the slightest idea of what any of these were going to do. If I were ever tempted to buy an airline stock, I should lie down and take a long nap first.

At the time, the industry had just been deregulated, and was still dominated by giants like Pan Am, TWA, Eastern Air, Western, Laker, Braniff, and a new low cost upstart called People Express. None of these companies exist today. It was the best investment advice that I ever got.

If you total up the P&L's of all of the US airlines that ever existed since Orville and Wilber Wright first flew in 1903 (their pictures are on my new anti-terrorism edition commercial pilots license), it is a giant negative number, well in excess of $100 billion. This is despite the massive government subsidies that have prevailed for much of the industry's existence.

The sector today is hugely leveraged, capital intensive, heavily regulated, highly unionized, offers customers terrible service, and is constantly flirting with, or is in bankruptcy. Its track record is horrendous. It is a prime terrorist target. A worse nightmare of an industry never existed.

I became all too aware of the travails of this business while operating my own charter airline in Europe as a sideline to my investment business during the 1980?s.

The amount of paperwork involved in a single international flight was excruciating. Every country piled on fees and taxes wherever possible. The French air traffic controllers were always on strike, the Swiss were arrogant, and the Italians unintelligible and out of fuel.

The Greek military controllers once lost me over the Aegean Sea for two hours, while the Yugoslavs sent out two MIG fighter jets to intercept me. As for the US? Did you know that every rivet going into an American built aircraft must first be inspected by the government and painted yellow before it can be used in manufacture?

While flying a Red Cross mission into Croatia, I got shot down by the Serbians, crash landed at a small Austrian Alpine river, and lost a disc in my back. I had to make a $300 donation to the Zell Am Zee fire department Christmas fund to get their crane to lift my damaged aircraft out of the river (see picture below). Talk about killing the competition!

Anyway, I diverge.

So you may be shocked to hear that I think there is a great opportunity here in airline stocks. A Darwinian weeding out has taken place over the last 30 years that has concentrated the industry so much that it would attract the interest of antitrust lawyers, if consumers weren?t such huge beneficiaries.

With the American-US Air (AAL) deal done, the top four carriers (along with United-Continental (UAL), Delta (DAL), and Southwest (LUV) will control 90% of the market.

That is up from 60% only five years ago. The industry has fewer seats than in 1982; while inflation adjusted fares are down 40%. Analysts are referring to this as the industry?s new ?oligopoly advantage.?

Any surprise bump up in oil prices is met with a blizzard of higher fares, baggage fees, and fuel surcharges. I can't remember the last time I saw an empty seat on a plane, and I travel a lot. Lost luggage rates are near all time lows because so few now check in bags. Interest rates staying at zero don?t hurt either.

The real kicker here is that stock in an airline is, in effect, a free undated put on the price of oil. If the price of oil stays in the $80 handle for a prolonged period of time, which it should, or continues to fall, airline stocks will rocket. This is on top of a $27 plunge in the price of Texas tea, the largest single cost item for the airline industry.

If you are looking for another indirect play, look at the bond market. With a new Boeing 787 Dreamliner costing up to $300 million each, airlines are massive borrowers of capital. With interest rates at all time lows, another huge source of costs have just been lifted off the airlines? backs.

The Ebola virus is an additional sweetener (if you could use such a term for a deadly disease), because it is enabling us to buy the stock down 30% than it would be otherwise. Delta Airlines (DAL) just so happened to be the airline that brought the first Ebola carrier to the US, so it has suffered the most. As frightening as this disease is (I studied it in my Army bacteriological warfare days), I doubt we will see more than a dozen cases in the US.

At least we are finally getting something for our $120 billion investment in Homeland Security since 2002. How much do you want to bet that they don?t cut the budget for the Center for Disease Control (CDC) this year, as they have for the past dozen!

On top of the massive fuel savings, a recovering US economy should boost profitability, given its recent maniacal pursuit of controlling costs. Some airlines have become so cost conscious that they are no longer painting their planes to gain fuel savings from carrying 100 pounds less weight! Just the missing pretzels alone should be worth a few cents a share in earnings.

This is not just a US development, but an international one. The International Air Transport Association (IATA) has just raised its forecast of member earnings from $7.6 billion in 2012 to $10.6 billion in 2013, a gain of 40%. The biggest earnings are based in Asia (China Southern Airlines, China Eastern Airlines, Air China), followed by those in the US, with $3.6 billion in profits.

Add all this together, and the conclusion is clear. The checklist is complete, the IFR clearance is in hand, and it is now time to push the throttles to the firewall for the airline stocks and get this bird off the ground.

And no, I didn't get free frequent flier points for writing this piece.

Meet the New Big Four

Maybe I Should Try Hedge Fund Trading?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/John-Thomas-Croatia-e1413407848662.jpg280400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-16 01:03:132014-10-16 01:03:13Delta Airlines is Cleared for Takeoff

Well, so much for the 200 day moving average! It?s like that girlfriend who has been ferociously loyal for the last year, and suddenly she is busy every weekend and never returns phone calls.

Not that this ever happens to me. Ahem.

I knew there would be trouble when the perma bulls on TV told me the market would bounce hard off this inviolable line in the sand, with the (SPX) at 1,905. I cut my bullish equity positions by two thirds on the first market rally and never looked back.

For proof that you still make beginner mistakes after 45 years in the business, take a look at how I handled my Tesla (TSLA) position last week. Elon Musk teased us all with his ?D? tweet two weeks ago, and the stock levitated magically while all other momentum stocks were being mercilessly thrown overboard.

?Women and traders? first comes to mind.

Did I sell into the rumor and capture the 80 basis point profit I had in hand? Nope. I held on until yesterday morning and bailed after a $40 plunge in the stock, taking a 1.62% hit.

This happened while the rest of Texas was coming down with Ebola Virus. I fall victim to the bout of over confidence whenever my Trade Alert success rate exceeds 90%, as it recently has done. I start to believe my own research, always a fatal flaw.

Fortunately, I?m still running double shorts in the S&P 500 (SPY) and the Russell 2000 (IWM) to hedge these losses. The ?Hedge? in ?Mad Hedge Fund Trader? is a well-earned one, I assure you.

You would think I would get hate mail for making such a stupid mistake. Au contraire! Readers thanked me for pulling the plug so quickly and with all humility. It appears that when most other newsletters put out a bad call they develop a sudden case of amnesia, leaving their customers to thrash about in bloody, shark-invested waters on their own.

Not here!

So, should we be burning up the Internet trunk lines with frenzied clicks to unload our long-term stock portfolios?

I think not. Here are ten reasons why I believe the bull market in shares is still alive and well:

1) Stocks are selling at only 14 X 2015 earnings, in the middle of the historic range.

2) The $23 plunge in oil prices we have enjoyed over the last five months amounts to a gigantic tax cut for the world economy, and could add a full 1% to US GDP growth, which has essentially come out of nowhere. Saudi Arabia told us today that this could go on for another year. Remember, it is our oil that is crushing prices.

3) The Christmas selling seasons is setting up to be a strong one, thanks to a friendly calendar and renewed consumer confidence. This is why retailers and credit card companies like American Express (AXP) have been reviving.

4) The November 4 midterm elections are still a big unknown for the market to discount. The next day could signal the beginning of the yearend bull market.

5) I think we are seeing the final blow off top in the bond market. A reversal would be very stock friendly, especially for financials (BAC).

6) Mergers and acquisitions are continuing at a torrid pace. This is happening because companies see each other as cheap, not expensive, and usually happens at market bottoms.

7) Those who aren?t merging are buying their own stock back with both hands, like Apple, at a staggering $400 billion annualized rate.

8) Volatility spikes (VIX) also signal market bottoms (see chart below). We are nearing another top with the closely followed indicator closing at $24.64 today, a high for the past two years.

9) Capital spending is accelerating, not only in technology, but across most other industries as well. This is why the IMF boosted its growth forecast for America next year to 3.8%, and that is probably a low number.

10) Ever heard of ?Sell in May and Go Away?? Well, ?Buy in November and stay put? is also true. That is only weeks away. October is usually the worst month of the year to sell and is not the path to untold riches.

The big question now is how much additional pain we have to suffer before the promised turnaround occurs.

My colleague, Mad Day Trader Jim Parker, went over his screens with a fine tooth comb and came up with $1,846 and $1,810 for the (SPX). Similarly, NASDAQ could trade down to the $3,700-$3,800 range.

My personal favorite is on the calendar, the Midterm elections on November 4. Whatever the outcome, we could see an upside explosion that lasts for six months, once thus unknown disappears. Not only could this make your year in 2014, but 2015 as well.

And I already know who is going to win! It is gridlock, whether the Democrats control one House of congress, or none!

Do You Think They Carry Ebola Virus?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/John-Thoms-Black-Swans-e1413901799656.jpg337400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-14 09:48:062014-10-14 09:48:0610 Reasons Why the Bull Market is Still Alive

It looks we are going to have to start watching the appalling Zombie shows on TV and in the movies. That is so we can gain tips on how to survive the coming Apocalypse that will unfold when the Ebola virus escapes Texas and spreads nationally.

I?m not worried. I?m actually pretty good with a bow and arrow.

Thank you United Airlines!

I happy to report that the total return for my followers so far in 2014 has topped 35%, compared to a pitiful 1% gain for the Dow Average during the same period.

In September, my paid Trade Alert followers have posted a blockbuster 5.01% in gains. This is on the heels of a red-hot August, when readers took in a blistering 5.86% profit.

The nearly four year return is now at an amazing 157.8%, compared to a far more modest increase for the Dow Average during the same period of only 37%.

That brings my averaged annualized return up to 39.7%. Not bad in this zero interest rate world. It appears better to reach for capital gains than the paltry yields out there.

This has been the profit since my groundbreaking trade mentoring service was first launched in 2010. Thousands of followers now earn a full time living solely from my Trade Alerts, a development of which I am immensely proud.

It has been pedal to the metal on the short side for me since the Alibaba IPO debuted on September 19. I have seen this time and again over four decades of trading.

Wall Street gets so greedy, and takes out so much money for itself, there is nothing left for the rest of us poor traders and investors. They literally kill the goose that lays the golden egg. Share prices have nowhere left to go but downward.

Add to that Apple?s iPhone 6 launch on September 8 and the market had nothing left to look for. The end result has been the worst trading conditions in two years. However, my double short positions in the S&P 500 (SPY) and the Russell 2000 (IWM) provided the lifeboat I needed.

The one long stock position I did have, in Tesla (TSLA), is profitable, thanks to a constant drip, drip of leaks about the imminent release of the Model X SUV. The Internet is also burgeoning with rumors concerning details about the $40,000 next generation Tesla 3, which will enable the company to take over the world, at least the automotive part.

Finally, after spending two months touring dreary economic prospects on the Continent, I doubled up my short positions in the Euro (FXE), (EUO).

Those positions came home big time when the European Central Bank adopted my view and implanted an aggressive program of quantitative easing and interest rate cuts. Hint: we are now only one week into five more years of Euro QE!

The only position I have currently bedeviling me is a premature short in the Treasury bond market in the form of the ProShares Ultra Short 20+ Treasury ETF (TBT). Still, I only have a 40 basis point hickey there.

Against seven remaining profitable positions, I?ll take that all day long. And I plan to double up on the (TBT) when the timing is ripe.

Quite a few followers were able to move fast enough to cash in on the move. To read the plaudits yourself, please go to my testimonials page by clicking here. They are all real, and new ones come in almost every day.

Watch this space, because the crack team at Mad Hedge Fund Trader has more new products and services cooking in the oven. You?ll hear about them as soon as they are out of beta testing.

The coming year promises to deliver a harvest of new trading opportunities. The big driver will be a global synchronized recovery that promises to drive markets into the stratosphere by the end of 2014.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011, 14.87% in 2012, and 67.45% in 2013.

Our flagship product,?Mad Hedge Fund Trader PRO, costs $4,500 a year. ?It includes?Global Trading Dispatch?(my trade alert service and daily newsletter). You get a real-time trading portfolio, an enormous research database, and live biweekly strategy webinars. You also get Jim Parker?s?Mad Day Trader?service and?The Opening Bell with Jim Parker.

To subscribe, please go to my website at?www.madhedgefundtrader.com, click on ?Memberships? located on the second tier of tabs.

Waiting for a High Level Contact

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas4.jpg325331Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-03 01:05:282014-10-03 01:05:28Mad Hedge Fund Trader Tops 30% Gain in 2014

If you want to delve into the case against the long-term future of US Treasury bonds in all their darkness, consider these arguments.

The US has not had a history of excessive debt since the Revolutionary War, except during WWII, when it briefly exceeded 100% of GDP.

That abruptly changed in 2001, when George W. Bush took office. In short order, the new president implemented massive tax cuts, provided expanded Medicare benefits for seniors, and launched two wars, causing budget deficits to explode at the fastest rate in history.

To accomplish this, strict ?pay as you go? rules enforced by the previous Clinton administration were scrapped. The net net was to double the national debt to $10.5 trillion in a mere eight years.

Another $6.5 trillion in Keynesian reflationary deficit spending by President Obama since then has taken matters from bad to worse. The Congressional Budget Office is now forecasting that, with the current spending trajectory and the 2010 tax compromise, total debt will reach $23 trillion by 2020, or some 130% of today?s GDP, 1.6 times the WWII peak.

By then, the Treasury will have to pay a staggering $5 trillion a year just to roll over maturing debt. What?s more, these figures greatly understate the severity of the problem.

They do not include another $9 trillion in debts guaranteed by the federal government, such as bonds issued by home mortgage providers, Fannie Mae and Freddie Mac. State and local governments owe another $3 trillion. Double interest rates, a certainty if wages finally start to rise and our debt service burden doubles as well.

It is unlikely that the warring parties in Congress will kiss and make up anytime soon, especially if we continue with a gridlocked congress after the November midterm elections. It is therefore likely that the capital markets will emerge as the sole source of any fiscal discipline, with the return of the ?bond vigilantes? to US shores after their prolonged sojourn in Europe. If you don?t believe me, just look at how bond owners have fared this week. Ouch!

Since foreign investors hold 50% of our debt, policy responses will not be dictated by the US, but by the Mandarins in Beijing and Tokyo. They could enforce a cut back in defense spending from the current annual $700 billion by simply refusing to buy anymore of our bonds.

The outcome will permanently lower standards of living for middle class Americans and reduce our influence on the global stage.

But don?t get mad about our national debt debacle, get even. Make a killing profiting from the coming collapse of the US Treasury market through buying the leveraged short Treasury bond ETF, the (TBT). Just pick your entry point carefully so you don?t get shaken out in a correction.

Looks Like I Can?t Afford the Next War

00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-09-19 01:03:462014-09-19 01:03:46The Structural Bear Case for Treasury Bonds

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.