Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

Sell any and all rallies in FedEx (FDX) – that’s my quick takeaway from the Chinese communist party publishing a sharp retort to their de-facto mouthpiece of a publication called the Global Times signaling FedEx’s imminent demise in greater China.

The Global Times is often used as thinly veiled statements to a wider global audience and mimics the ideology of the ruling communist party and their main positions on critical issues.

As regards to FedEx’s business in China, it said:

“There are rising calls for China's postal service regulator to cut off FedEx from China market, as Huawei has accused the US express courier of diverting and rerouting its packages.”

FedEx is crushing the Chinese logistics market currently and is the go-to carrier holding firm at 54.6% market share.

They have been around in China for as long as the economic boom has percolated inside the mainland from 1984, far before any of its local competitors were even up and running by a decade or two.

FedEx’s latest acquisition of Dutch-based TNT Express in 2016 solidified its dominance.

Foreign competition is a mainstay of international shipping patterns in China with the top three rounded out by DHL (DPSGY) with a 25.07% market share and United Parcel Service (UPS) with a 16.94% market share.

If these assertive claims do result in FedEx meaningfully losing China revenue, UPS wouldn’t stand to pick up the leftovers and could be put out to pasture by the same issue of hailing from a country that has an active adversarial economic policy against China’s.

If anyone would benefit, it would by DHL, given that Germany has a far less hawkish stance towards China, and they are unwilling to bite off the hand that feeds them.

The current situation is a concerning sign for the future of Germany as an industrial power and ability to sustain itself against China Inc.

It could be somewhat true that Germany has overextended themselves and only time, Made in China 2025 project, and the mood of the Chinese communist party can delay the inevitability of full tech hegemony over their western European counterpart.

The communist party could choose to just bypass DHL altogether and kick out all foreign invaders gifting courier responsibilities to Alibaba-based (BABA) subsidiaries and the likes of ZTO Express (ZTO) who provide express delivery and other value-added logistics services in China.

DHL will hope that China delays any draconian measures and pray that its active partnership with a local logistic firm has real legs.

DHL's revenue sharing agreement with SF Express does not preclude them from the anger of Chinese regulators, but the risk of Chinese regulators favoring local couriers has risen another 25%.

Playing by the rules goes a long way in China, even if they change every day, and for customers across DHL’s target audience of industries including technology, health care, retail, automotive, and e-commerce.

DHL CEO Frank Appel said, "Combined with our global operations standards and network support, the agreement provides a solid foundation to continue exploring further opportunities in China in the coming years."

From an outside perspective, this sounds more like forced cooperation with forced technology transfers with the mainland companies slurping up Germany tech knowhow.

Doing a deal with the devil for access to a 1.3 billion customer market is being put through the ringer.

When I view the snippets through the lens of geopolitics, it’s hard to believe that at such a sensitive time, FedEx would actively “reroute” packages and knowingly approved this behavior, they simply can’t be that clumsy.

The situation smells like an overt show of nationalism by a group of individuals, and it questions the longevity of FedEx operating in China all the same.

FedEx promptly responded confessing:

“We regret that this isolated number of Huawei packages were inadvertently misrouted.”

An unintentional mistake offered a golden opportunity to tie the logistics company to the U.S. government’s aggressive nature and going forward FedEx will remain in a shroud of mystery until investors can get further grips on the rates of growth of their Chinese operations.

If FedEx were afraid about this, then they must be tearing their hair out about the domestic behemoth that is Amazon (AMZN) and their desires to install a full-service logistic service to blanket FedEx from e-commerce deliveries.

This has been the initial premise of my short call on FedEx, which has proved correct, and the regulatory nightmare in China will cast another cloud around its business.

Any strength in FedEx shares will be met with a cascade of selling activity, and as the economy slows down because of tariff-induced headwinds, this is a stock to outright short.

Back to China, FedEx slashed its full-year profit forecast for the second time in three months after reporting weaker-than-expected third quarter earnings.

The Chinese economy is absolutely slowing down, and its effects are impacting surrounding Asian nations.

Manufacturing cuts will cause the number of courier packages to slide in China and there is no telling how bad this trade stand-off could get.

It doesn’t look good for FedEx, and I reiterate my short stance on the company.

Mad Hedge Technology Letter

April 30, 2019

Fiat Lux

Featured Trade:

(AMAZON’S NEW GAME CHANGER)

(AMZN), (WMT), (TGT), (UPS), (FDX)

Amazon’s free 2-day shipping for Prime Customers is on the verge of becoming free 1-day shipping after the company recently announced this new wrinkle to their business model.

Amazon’s competitors should be shivering in their wake.

But it’s not all doom and gloom for the other e-commerce giants, hardly so, the gap up in the fierce competition will do what General Data Protection Regulation (GDPR) rules in Europe did to competition – enclose the existing players off from the smaller fish.

In examining who will be the last man standing, I have come to the conclusion that it will not just be one or two grinding it out in a vacuum, but more like several winners that will all benefit to certain degrees.

The outsized denominating factor in the e-commerce wars is logistics and who can best put this segment together.

E-commerce companies are being bullied into leaner models because of the premium on heavy scaling that will pile on added costs to make 1-day free shipping a reality.

This isn’t selling lemonade on your driveway, getting 1-day shipping to work will be a tough nut to crack.

The result will be the imminent deterioration of FedEx (FDX) and United Parcel Service (UPS) on the expectation that Amazon will crowd them out.

It could be the case that Amazon improves its logistical capabilities to the point that FedEx and UPS will have to sell itself off or risk death by a thousand cuts.

There looks like no navigational path ahead for these two legacy logistic companies because of the nature of being lower down on the value chain.

The only other choice is if FedEx or UPS is able to jump into the e-commerce business themselves by buying a Kroger to maneuver into the integration process through the other side.

Either way, acquiring a supermarket is no guarantee of future success considering the stakes are about to become higher and higher.

I believe that Walmart will respond to Amazon by rolling out free 1-day shipping with no membership fee, boosting its customer experience while attracting and retaining customers.

Walmart is in this fight until the bitter end and they have invested heavily in improving the technological aspects of the company.

Where does this end?

Logistics will perpetually improve as companies drain more money into logistics, and customers will eventually receive their e-commerce packages in a drone less than 1-hour after payment.

Amazon CFO Brian Olsavsky told investors that Amazon is plunking down $800 million over the quarter in its fulfillment network and that number should rise every year as Amazon has targeted logistics as a huge competitive advantage that they must capitalize on and thrive in.

Amazon already has the option for 1-day free shipping in the European Union and Japan where the delivery distances are truncated.

America poses geographical challenges that will cost more to solve and will rely on the deregulation of future drone flights and cooperation with Amazon sellers to deliver this big step up in customer experience.

The constant iteration upgrades in logistics for the past 20 years have made this possible, and I believe Amazon would be well served to bite the bullet and splurge for UPS or FedEx to make it easier on themselves.

It is not shocking there is a scarcity value of logistic carriers and e-commerce giants will need more logistical capacity to execute free 1-day shipping and eventually free 1-hour shopping.

Amazon hasn’t figured out how to transport physical goods through a computer yet, but I am certain, if there was the technology, they would spend unlimited amounts to get it to that point.

The most ironic aspect of the e-commerce wars is that supermarkets, being a part of e-commerce and the logistics behind it, is the most innovative part of technology at this moment.

Tech companies have identified that customers need to eat three times per day as paramount and are sizzling through cash to build this unfathomable logistics system - effectively working miracles and becoming whirling dervishes to seize this part of the economy.

I would probably label automobiles and the self-driving autonomous technology behind logistics as the second most innovative part of technology at this moment.

As for Amazon’s earnings report, it was a mixed bag, but the good in the bag was astounding.

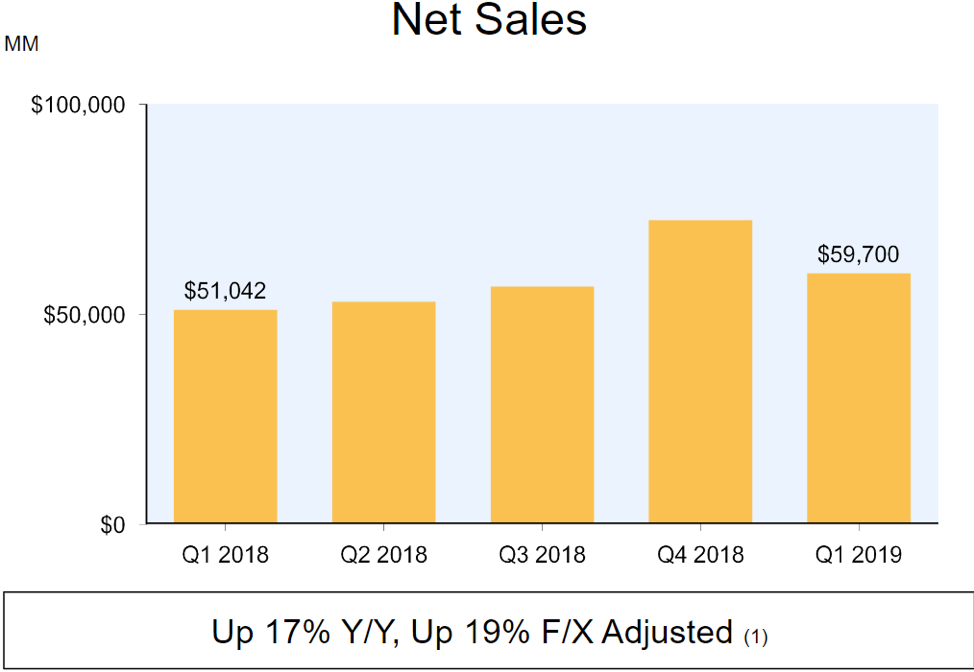

Profitability boosts through the scaling and efficiency savings inflated the bottom line with EPS in Q1 at $7.09 compared to expectations of $4.72.

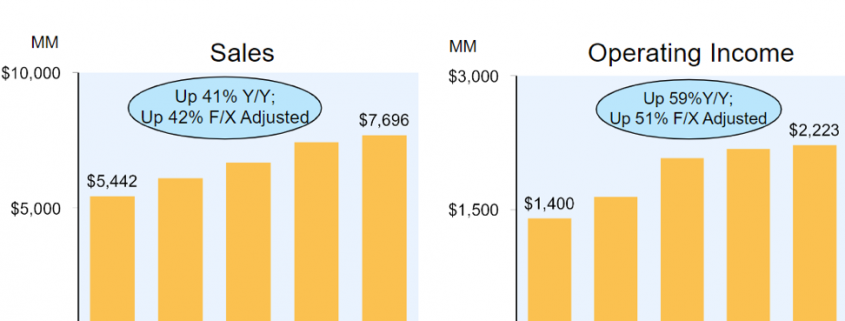

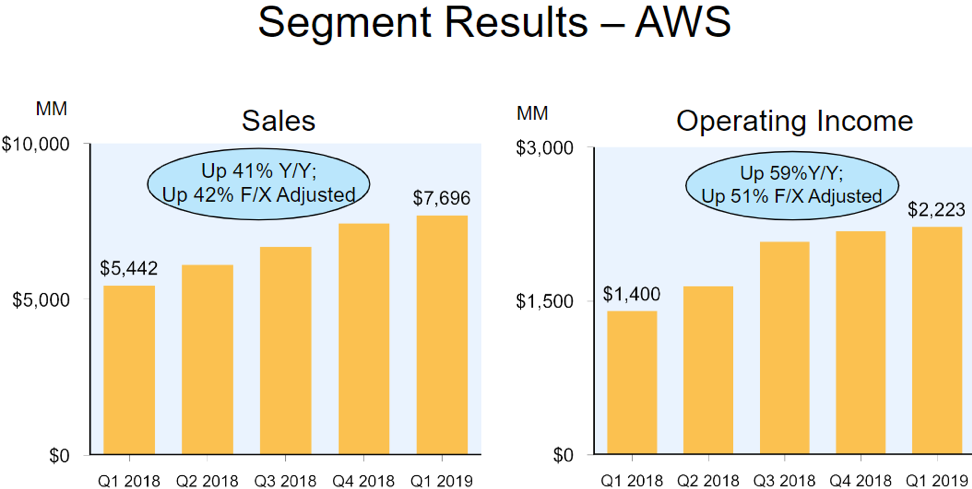

Amazon Web Services (AWS) is still commanding enormous growth rates which is miraculous for a division its size, the cloud unit grew 41% YOY which is down from 49% last year.

On the negative side, the advertising business experienced a sharp slow down growing only 34% YOY to $2.7 billion.

Remember that ad sales were expanding over 100% YOY in prior quarters.

Total Revenue only grew 16.9% which shows how difficult it is to grow at Amazon’s size and brings down the digital ad growth rate almost on par with Facebook.

Walmart and Target will be forced to compete with free 1-day shipping, and this will make their services better as well.

The question is how much pain can investors handle in terms of capital investments?

I believe substantially more.

Walmart and Target shares are poised to move higher on the news because the improvements in their logistical services will widen the gap between the haves and have nots.

These companies are in the midst of persuading investors they should be revalued as tech companies and duly receive growth multiples.

They are doing a great job and imagine how badly this news feels for medium-tier grocers with a minimal digital footprint.

Investors will come to grips that Amazon, Walmart, and Target will pull away from the pack and trade blows with each other.

This time it's Amazon, but it's not the last laugh.

Where does this all lead?

The end game is voice-triggering smart speakers where Amazon and its Echo speaker have a distinctive lead and a market share of around 70%.

Graphic interfaces will exist in only voice-activated form and content will be bundled into voice technology where even managing a Walmart order will require Amazon Echo to register sales.

That type of future is still a way off, but these are the next baby steps in that direction.

In short, revelations of free 1-day shipping to Amazon prime customers is convincingly bullish for Amazon, quite bullish for Walmart, Target, and a death knell for smaller e-commerce platforms and logistic dinosaurs.

Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

If there was ever a canary in the coal mine, we got one with chipmaker Micron (MU) delivering weak earnings results missing on the top line but squeaking through a one-cent beat on the bottom line.

Love them or hate them, chip companies are susceptible to the boom-bust cycle that is a hallmark of the chip industry.

The beginning of the bust stage of the cycle is upon us with management detailing an “inventory adjustment” that put a damper on revenue.

Micron followed that up by reducing capex for next year and it will take 2-3 quarters to work off this bloated inventory channel.

The perpetrator to the inventory backlog is the smartphone industry.

President and CEO of Micron Sanjay Mehrotra particularly noted “high-end smartphones” as the malefactor tugging down the demand.

This is another damming testament to the prospects of Apple’s (AAPL) suppliers Quorvo (QRVO), Skyworks Solutions (SWKS), NXP Semiconductors (NXPI), Cirrus Logic (CRUS), and Lumentum Holdings (LITE) who can’t catch a break.

The last six months have fired a barrage of poison-tipped arrows at their core business and these stocks are squarely in the no-fly zone until Apple and the trade war can conjure up some good news.

To say these shares are oversold is an understatement, but we are in an extreme trading environment with volatility shooting up the wazoo.

Further reducing the glimmer, Chinese tariffs took up a worrying amount of the conference call dialogue. Investors found out that tariffs pinged half a percent of gross margins.

I have been outright bearish the chip industry from the middle part of the year and Micron is heavily reliant on China for about half of its revenues which is a death sentence in December 2018.

As the China risks have spiked after each head fake détente, so have the execution risks to chip companies with an overly reliant manufacturing process in China.

Not only has the execution risk ratcheted up, but the regulatory risk through costly tariffs is now eroding Micron’s margins.

If you thought that was a downer, then FedEx (FDX) made sure the nail was in the coffin by its ghastly earnings report.

The stock sold off hard confirming fears that global growth is decelerating.

Management did not mince their words about the state of the world and investors usually listen because FedEx is a reliable yardstick of the bigger global economy.

CEO of FedEx Fred Smith offered an olive branch painting a picture of a “solid” US economy, but the conundrum is that the US economy and any other country don't exist in a vacuum and that has been highly evident in Britain who is engaging in economic suicide by disengaging from the globalized world.

Smith cited Europe as a stumbling block and blamed the bulk of weak guidance on “bad political choices”, a thinly veiled dig at the poor level of governance carried out around the world lately.

I might chime in that it is quite strange when political parties and sovereign nations adopt the game of chicken as the leading political strategy applying it to everything and anything.

The side effects to business have been startling with management unable to assuage investor sentiment and business plans shredded apart because of impulsive policy moves.

Politicians aren’t grasping fully that stock market moves are inherently tied to the news cycle and the overwhelming volume of bad news that shouldn’t be as bad as it should be, has a multiplier effect on the stock market algos that go haywire.

It truly is the world of the algos and humans are living in their world and not the other way around.

The most important takeaway from FedEx is what they didn’t say.

Early development of the de-facto Amazon Airlines has already cost FedEx up to 3% of total volume growth.

And this is just the beginning.

Amazon is still feeling around for the rocks at the bottom while it tries to cross the river.

Once it masters logistics, expect a radical swivel towards the integration of their own airline into the bulk of Amazon.com’s package deliveries.

And when FedEx’s management claims that the market has gotten it wrong about the Amazon threat, that means the market is completely correct.

The market is always right.

Amazon’s master plan is to vertically integrate every last process down to the last mile, the doorbell, and now the microwave as Amazon has rolled out a myriad of smart home products.

FedEx management has to be blind to understand this won’t damage future sales.

It is materially false if FedEx thinks Amazon is not competing with them, and the sad part of this is there is not much FedEx can do about it.

The shipping giant cut its 2019 earnings forecast between $15.50 and $16.60 per share — from $17.20 to $17.80 a share.

FedEx’s goal of eclipsing $1.5 billion in operating income by fiscal 2020 has been shelved disappointing investors. FedEx cratered 12% on a day that saw the Fed do its best body slam imitation on the market.

The first phase of the logistics swivel is taking delivery of 40 planes and constructing a hub that will be able to operate 100 planes, then it will do as Amazon does with everything – scale it to the hills.

FedEx and UPS have a few years to figure out how to counteract this existential crisis and not decades.

Technology moves that fast now in this interconnected world.

Domestic volume comprises 17% of revenues at UPS and 19% at FedEx, management won’t be able to hide this problem under the carpet as the drag becomes highly visible like a sore thumb.

Analysts expect Amazon Air to offer more than slim savings to its business model saving between $2 to $4 per package next year.

The annual savings add up from $1 billion to $2 billion or 3% to 6% of its global shipping costs.

It is spot-on to admit that over the last few years, the explosion of packages during the holiday shopping season has put higher levels of stress on the U.S. Postal Service, UPS (UPS), and FedEx.

Even though overloaded with business, all three carriers have posted record levels of on-time deliveries and they appear to be handling the surge in volume.

But there will come a moment in time when an inflection point will give Amazon the keys to the car.

They will suddenly stop offering their e-commerce packages to these three carriers and business will drop off a cliff for them.

That is the future these three are confronted with and there is nothing they can do unless they build their own Amazon.com which is a pie in the sky dream at this point.

Amazon is out to prove they can execute the logistic part of their business cheaper and faster than anyone else because of the superior management and mountain of data they can act on.

I believe it will happen.

Part of stretching themselves with a new army of minions in Washington D.C., New York, and Nashville is partly about fulfilling the job of comprehensively and vertically integrating their e-commerce platform.

It will take a horde of workers to make this happen.

If the prophecy from FedEx management comes true and the global economy indeed softens next year, the stock will bear the brunt of the downside momentum and UPS too.

Stay away from the trio of deliverers. There are healthier fishes in the sea.

And as for the chip sector and Apple, wait on the sidelines for some good news.

Mad Hedge Technology Letter

November 14, 2018

Fiat Lux

Featured Trade:

(I NAILED IT)

(AMZN), (GOOGL), (FDX), (UPS), (JCP)

Global Market Comments

September 24, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S FED WEEK),

(SPY), (XLI), (XLV), (XLP), (XLY), (HD), (LOW), (GS), (MS), (TLT),

(UUP), (FXE), (FCX), (EEM), (VIX), (VXX), (UPS), (TGT)

(TEN TIPS FOR SURVIVING A DAY OFF WITH ME)