I have a request for all of you readers. Please do not nominate me for justice of the Supreme Court.

I have no doubt that I could handle the legal load. A $17 copy of Litigation for Dummies from Amazon would take care of that.

I just don’t think I could get through the approval process. There isn’t a room on Capitol Hill big enough to house all the people who have issues with my high school background.

In 1968, I ran away from home, hitchhiked across the Sahara Desert, was captured by the Russian Army when they invaded Czechoslovakia, and had my front teeth knocked out by a flying cobblestone during a riot in Paris. I pray what went on in Sweden never sees the light of day.

So, I’m afraid you’ll have to look elsewhere to fill a seat in the highest court in the land. Good luck with that.

The most conspicuous market action of the week took place when several broker upgrades of major technology stocks. Amazon (AMZN) was targeted for $2,525, NVIDIA (NVDA) was valued at $400, and JP Morgan, always late to the game (it’s the second mouse that gets the cheese), predicted Apple (AAPL) would hit a lofty $270.

That would make Steve Jobs’ creation worth an eye-popping $1.3 trillion.

The Mad Hedge Market Timing Index dove down to a two-month low at 46. That was enough to prompt me to jump back into the market with a few cautious longs in Amazon and Microsoft (MSFT). The fourth quarter is now upon us and the chase for performance is on. Big, safe tech stocks could well rally well into 2019.

Facebook (FB) announced a major security breach affecting 50 million accounts and the shares tanked by $5. That prompted some to recommend a name change to “Faceplant.”

The economic data is definitely moving from universally strong to mixed, with auto and home sales falling off a cliff. Those are big chunks of the economy that are missing in action. If you’re looking for another reason to lose sleep, oil prices hit a four-year high, topping $80 in Europe.

The trade wars are taking specific bites out of sections of the economy, helping some and damaging others. Expect to pay a lot more for Christmas, and farmers are going to end up with a handful of rotten soybeans in their stockings.

Barrick Gold (ABX) took over Randgold (GOLD) to create the world’s largest gold company. Such activity usually marks long-term bottoms, which has me looking at call spreads in the barbarous relic once again.

With inflation just over the horizon and commodities in general coming out of a six-year bear market, that may not be such a bad idea. Copper (FCX) saw its biggest up day in two years.

The midterms are mercifully only 29 trading days away, and their removal opens the way for a major rally in stocks. It makes no difference who wins. The mere elimination of the uncertainty is worth at least 10% in stock appreciation over the next year.

At this point, the most likely outcome is a gridlocked Congress, with the Republicans holding only two of California’s 52 House seats. And stock markets absolutely LOVE a gridlocked Congress.

Also helping is that company share buybacks are booming, hitting $189 billion in Q2, up 60% YOY, the most in history. At this rate the stock market will completely disappear in 20 years.

On Wednesday, we got our long-expected 25 basis-point interest rate rise from the Federal Reserve. Three more Fed rate hikes are promised in 2019, after a coming December hike, which will take overnight rates up to 3.00% to 3.25%. Wealth is about to transfer from borrowers to savers in a major way.

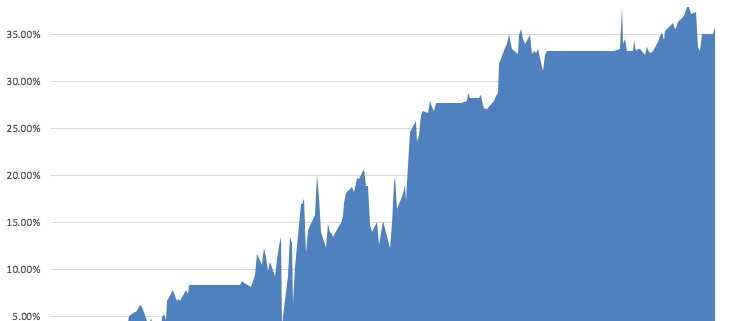

The performance of the Mad Hedge Fund Trader Alert Service eked out a 0.81% return in the final days of September. My 2018 year-to-date performance has retreated to 27.82%, and my trailing one-year return stands at 35.84%.

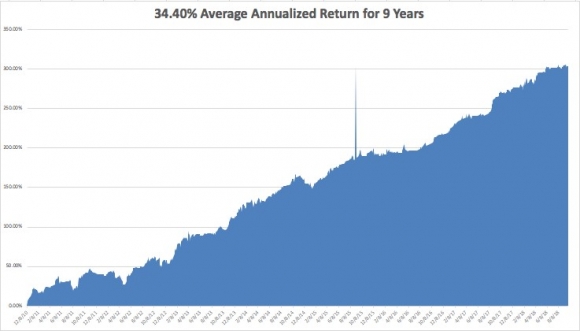

My nine-year return appreciated to 304.29%. The average annualized return stands at 34.40%. I hope you all feel like you’re getting your money’s worth.

This coming week will bring the jobspalooza on the data front. On Monday, October 1, at 9:45 AM, we learn the August PMI Manufacturing Survey.

On Tuesday, October 2, nothing of note takes place.

On Wednesday October 3 at 8:15 AM, the first of the big three jobs numbers is out with the ADP Employment Report of private sector hiring. At 10:00 AM, the August PMI Services is published.

Thursday, October 4 leads with the Weekly Jobless Claims at 8:30 AM EST, which rose 13,000 last week to 214,000. At 10:00 AM, September Factory Orders is released.

On Friday, October 5, at 8:30 AM, we learn the September Nonfarm Payroll Report. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, it’s fire season now, and that can only mean one thing: 1,000 goats have appeared in my front yard.

The country hires them every year to eat the wild grass on the hillside leading up to my house. Five days later there is no grass left, but a mountain of goat poop and a much lesser chance that a wildfire will burn down my house.

Ah, the pleasures of owning a home in California!

Good luck and good trading.

We’re Taking Calls Now

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/trailing-one-year-image-1-1-e1538166658317.jpg365580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-10-01 01:07:252018-10-04 13:06:00The Market Outlook for the Week Ahead, or Don’t Nominate Me!

Global Market Comments

September 27, 2018 Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL), (TUESDAY, OCTOBER 16, 2018, MIAMI, FL,

GLOBAL STRATEGY LUNCHEON)

In a flurry of deals, the music streaming industries consolidation is powering on as some of the industry’s biggest players have completed new acquisitions.

Is there a new King of the Castle?

Not yet.

In any case, the shakeout still allows Spotify to claim itself as the No. 1 company in the music streaming industry, but Apple (AAPL) and Sirius XM (SIRI) have gained.

There is still work to be done for the trailing duo but it is a step in the right direction.

Apple’s deal with Shazam, which just gained approval, was consummated last December, but was held up by European regulators over antitrust problems.

The Europeans have clamped down on American tech companies of late forcing them to play nicer after decades of running riot inside the region.

The Shazam app analyzes then pinpoints titles from music, movies, and television shows based on a brief sample through the device’s microphone.

If your neighbors are blasting the tunes upstairs at a Friday night shindig and you want to find out what song is causing you to lose sleep at night, just turn on your microphone and upload it into Shazam.

Shazam will tell you exactly the song’s title and the artist’s name.

Even dating back to 2013, this app was among the top 10 most popular apps in the world.

In 2018, Shazam has carved out a user base of more than 150 million monthly average users (MAU) and growing.

Shazam is used more than 20 million times per day.

An opportunity lies in urging Shazam users to then adopt Apple music.

Interestingly enough, to upgrade the quality of the app’s functionality, Apple is stripping away digital ads in Shazam.

Apple has made an unrelenting attempt to avoid introducing lower grade tech that could potentially taint its clean-cut brand.

Recently enough, film producers have complained that Apple is completely averse to any content with gratuitous violence, excessive drug use, and candid sex scenes.

Apple wants to cultivate and sell its pristine image.

Digital ads also fail to make the cut.

This spotless image boosts Apple’s pricing power along with the high quality of products that has seen Apple retain its place as the producer of the best smartphone in the world.

Other smart phone brands are still in catchup mode with a brand image significantly inferior to Apple’s.

And Apple CEO Tim Cook isn’t even interested in monetizing Apple music, and is more focused on “doing the right thing” for it.

Yes, the job of every company is to be in the black, but the No. 1 responsibility for a modern tech company is to grow and grow profusely.

Tech investors pay for growth, period.

As investors have seen with Netflix, companies can always raise prices after seizing market share because of the stranglehold on eyeballs inside a walled garden.

That potent formula has been the bread and butter of powerful tech companies of late.

Spotify is a captive of the music industry, of which it is entirely dependent for its source of goods, in this case songs.

At the same time, the music industry has fought tooth and nail to destroy the likes of Spotify, which benefits immensely from distributing the content it creates.

History is littered with failed music streaming services outgunned in the courtroom. Pandora (P) is the biggest public name out there whose share price has tanked over the long haul.

Pandora has created a proprietary algorithm offering song recommendations to listeners, but it is more or less an online music streaming app heavily reliant on a freemium pricing model with ads.

Sirius XM Holdings, a satellite radio company, signaled its intent in the music streaming business by taking a 19% in Pandora’s business last year.

It has followed that up now by completing a full takeover of the Oakland, California company for $3.5 billion.

This move adds 75 million users to its 36 million usership on Sirius and, in my view, the main objective is an eyeball grab to buy more listeners dragging them into its walled garden.

To triple a user base instantly to 75 million listeners is a boon for Sirius, which now has the firepower to legitimately compete with Spotify.

Pandora has been shopping itself around for the past two years, and companies such as Facebook were whispered to be eyeing this company.

Facebook chose to focus on developing dating and romance functions on its platform, and has mainly ignored the music streaming possibilities.

More critically, it allows Sirius to diversify out of the car space where satellite radio is predominantly used.

As much as Americans love to drive, the home is where they rest, and sleep, and Pandora will unlock a path into the home of listeners.

Synergies between home audio through Pandora, and car audio through Sirius should be evident over time.

The music streaming industry, such as the television streaming industry, has become fiercely competitive as of late. And this is a prudent move for Sirius to buy a new customer base at the same time as moving into the home.

The trend of tech companies penetrating the home and making it as smart as possible is revived constantly.

This piece of news isn’t as earth-shattering as Amazon’s (AMZN) smart home product launch event, but nonetheless indicates another leg up in competition for fresh user growth and its data.

This M&A surge is occurring amid a backdrop of the music industry’s obsession to exterminate Spotify and the other music streaming companies.

They are on a mission to force up the royalties these Internet giants must pay to pad their pockets and protect their interests.

Royalties are the music streaming companies’ main cost, and for Spotify, these royalty payments eat up 78% of total revenue.

But that does not mean Spotify is a bad company or even a bad stock.

Every company has its share of pitfalls. Throw in the mix that Amazon (AMZN) and Apple have music streaming services that do not even need to make a profit, and you will understand why some might be wary about putting new money to work in music streaming business stocks.

The primary reason that Spotify shares will outperform for the foreseeable future is because it is the preeminent music streaming platform.

Also, there is favorable latitude to make way toward the goal of monetization, and ample space to improve gross margins.

Global streaming revenue growth has gone ballistic as the migration to mobile devices and cord cutting has exacerbated the monetization prospects of the music industry.

Streaming revenue was a shade under $2 billion in 2013, and continued to post a growth trajectory of more than 40% each year since.

As it stands now, total global streaming revenue registered just a tick under $7 billion per year in 2017, and that was an improvement of 41.1% from 2016.

The choice among choices is Spotify in 2018.

The company was dogged by many years of famous artists removing their proprietary content from the platform citing unfavorable terms.

Eventually, almost all artists have relented and reinstalled their music on Spotify. They depend on alternative moneymaking avenues to compensate for lack of royalties, mainly live music.

Spotify has seized even more industry power with its new function of completely bypassing the music industry altogether, by offering a way for aspiring artists to directly upload music content onto its online platform.

Crushing the middleman has been a widespread theme in the tech industry for the past few decades, and the music industry is no different.

As technology has hyper-accelerated, the cost of producing music has plummeted giving access to just about anyone who has any talent.

No need to rent a sound studio for thousands of dollars per hour anymore in West Hollywood, and the music industry knows it.

It could be possible that the next cohort of viral artists will never cough over a dime to the music industry, and the bulk of the profits will be collected by a music streaming titan that distributes their content online.

How does Spotify make money?

It earns its crust of bread through paid subscriptions but lures in eyeballs using an ad-supported free version of its platform.

Naturally, the paid version is ad-less, and this subscription is around $5 to $15 per month.

In the second quarter, Spotify’s paid subscription volume surpassed 83 million, a sharp uptick of 40% YOY.

Ad-supported users came in at more than 101 million, even under the damage that General Data Protection Regulation (GDPR) did to western tech companies.

The ad-supported subscribers rose 23% YOY, and the paid version expects between 85 million to 88 million paid subscribers in the third quarter.

Many of the new paid subscribers are converts from its free model.

Spotify is poised to increase revenue between 20% to 30% for the rest of 2018.

The rise of Spotify's developing data division could extract an additional $580 million of revenue in 2023, making up 2% of total revenue.

When Spotify did go public, the robust price action was with conviction, making major investors - such as China’s Tencent, which possess a 9.1% stake and Tiger Global Management, which owns 7.2% - happy stakeholders.

In the last quarter’s earnings report, Spotify CFO Barry McCarthy reiterated the company’s goal to push gross margins from the mid-20% range to “gross margins in the 30% to 35% range.”

A jump in gross margins would go a long way in making Spotify appear more profitable, and that is the imminent goal right now.

Bask in the glow of the growth sweet spot Spotify finds itself in right now.

For the time being, the music division of Amazon and Apple are just a side note, even with Apple’s purchase of Shazam.

But Apple is vigorously improving its service products as its software and services segment moves from strength to strength, but that doesn’t particularly mean Apple Music.

Investors must sit on their hands to see how Sirius’s acquisition of Pandora plays out. These are by no means two extraordinary companies, and a major overhaul is required to make these two mediocre companies into one overperformer.

If you had to choose among Sirius, Pandora, or Spotify, then cautiously leg into a few shares of Spotify to test the waters.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-26 01:06:522018-09-25 19:15:38Did Sirius Open up Pandora’s Box?

Do you want to get in on the ground floor of another major new trend?

Well, here’s another new trend. Get this one right and your retirement funds should multiple like rabbits.

There have been some pretty amazing announcements by governments lately.

The United Kingdom has banned the use of gasoline-powered engines by 2040.

China is considering doing the same by 2035.

And now the State of California is targeting 100% alternative energy use by 2040. That’s only 22 years away.

The only unknown is what such a planned obsolescence program will look like, and how soon it will be implemented.

With 20% of the U.S. car market, don’t take the Golden State’s ruminations lightly.

California was the first state to require safety glass, seat belts, and catalytic converters, and the other 49 eventually had to follow. Some 20% of the market is just too big to ignore.

The death of the car is now upon us, and it is still early, very early.

This is a very big deal.

Earlier in my lifetime, car production directly and indirectly accounted for about one-third of the U.S. economy.

Much of the growth during our earlier Golden Ages, in the 1920s and the 1950s, were driven by a never-ending cycle of upgrades of our favorite form of transportation, and the countless ancillary products and services needed to support them. Tail fins, radios, and tons of chrome assured you always had to have the next new model.

Today, 253 million automobiles and trucks prowl America’s roads, about half the world’s total, with an average age of 11.4 years.

The demise of this crucial industry started during the 2008 crash, when (GM) and Chrysler (owned by Fiat) went bankrupt. Only more conservatively run, family owned Ford (F) survived on its own.

The government stepped in with massive bailouts. That was the cheaper option for the Feds, as the cost of benefits for an entire unemployed industry was far greater than the cost of the companies absorbed.

If it hadn’t done so, the auto industry would have decamped for a new base near the technology hubs in California, and today would be a decade closer to their futures than they are now.

And remember, the government made billions of dollars of profits from its brief foray into the auto industry as an investor. It was one of the best returns on investment in history in major size.

I’ll breakout the major directions the industry is now taking. Hint: It doesn’t have much to do with traditional metal bashing.

The Car as a Peripheral

The important thing about a car today is not the car, but the various doodads, doohickeys, gizmos, and gadgets they stick in them.

In this category you can include 24/7 4G wireless, full Internet access, mapping software, artificial intelligence, and learning programs.

(GM) is now installing more than 100 microprocessors in its vehicles to control and monitor various functions.

Good luck doing your own tune-ups.

The Car as a Service

When you think about it, automobile ownership is a wildly inefficient use of capital. It is usually a family’s second largest expense, after their home, running $30,000 to $80,000.

It then sits unused in garages or public parking for 96% to 98% of the day. Insurance, maintenance, and liability costs can be off the charts.

What if your car was used 24/7, as is machinery in well-run industrial plants? Your cost drops by 96% to 98% to the point where it is almost free.

The sharing economy is the way to accomplish this.

We are already seeing several start-ups attempting to achieve this in major U.S. cities, such as Zipcar, Car2Go, Getaround, RelayRides, and City CarShare.

What happens to conventional car companies when consumers shift from ownership to sharing? Demand plunges by 96% to 98%.

Perhaps that is why auto shares (GM), (F) have performed so abysmally this year relative to technology and the main market.

Self-Driving Technology

This is the hottest development area in the industry, with Apple (AAPL), Alphabet (GOOG), and the big European carmakers committing thousands of engineers.

Let’s say your car is now comfortably driving you to work, allowing you to read the morning papers and catch up on your email. Or maybe you’re lazy and would rather watch the season finale of Game of Thrones.

What else is possible?

How about if, instead of parking, your car drops you off, saving that exorbitant fee.

Then it joins Uber, picking up local riders and paying for its own way. It then dutifully returns to pick you up at your office when it’s time to go home.

Since the crash rate for computers is vastly lower than for humans, car insurance rates will collapse, gutting that industry.

Ditto for life insurance, as 35,000 people a year will no longer die in car crashes.

Half of all emergency room visits are the result of car accidents, so that business disappears too, dramatically shrinking health care costs in the process.

I have been letting my new Tesla S-1 drive me since last year, and I can assure you that the car can drive better than I can, especially at night.

What better way to get home after I have downed a bottle of Caymus cabernet at a city restaurant?

Driverless electric cars are totally silent, increasing the value of land near freeways.

Nor do they require much maintenance, as they have so few moving parts. Exit the car repair industry.

I could go on and on, but you get the general idea.

For more on the topic, please read “Test Driving Tesla's Self Driving Technology” by clicking here.

Virtual Reality

After 30 years of inadequate infrastructure budgets, trying to get into any America city center is a complete nightmare.

Only last week, a cattle truck turned over on the Golden Gate Bridge, bringing traffic to a halt. Fortunately, a cowboy traveling to a nearby rodeo was able to unload his horse and lasso the errant critters (no, it wasn’t me!).

Even if you get into the city, you will be greeted by a $40 tab for a parking space. Hopefully, no one will smash your windows and steal your laptop (happened to me last year).

Why bother?

Thirty years ago, teleconferencing services pitched themselves as replacing the airplane.

Today, we are taking the next step, using Skype and GoToMeeting to conduct even local meetings, as we do at the Mad Hedge Fund Trader.

Virtual reality is clearly the next step, providing a 3D, 360 degree experience that makes you feel like you and your products are actually there.

Better to leave that car in the garage where it can get a top up on its charge. BART is cheaper anyway, when it runs.

New Materials

We are probably five years away from adopting the carbon fiber technology now used in the aircraft industry for mass-market cars. Carbon has one-tenth the weight of steel, with five times the strength.

The next great leap forward for electric cars won’t be through better batteries. It will come through a 70% reduction of the mass of a car, tripling ranges with existing technology.

San Francisco Becomes the Car Capital of the World

This will definitely NOT happen, as sky-high rents assure that the city by the bay will never attract large, labor-intensive industries.

Instead, the industry will develop much as the one for smartphones. The high value-added aspects, design and programming, will stay in California.

The assembly of the chassis, the body, and the rest of the vehicle will be best done in low-cost, tax-free states with a lot of land, such as Texas and Nevada.

What will happen to Detroit? It has already become a favored destination of new venture capital financial start-ups - the cost of offices and housing is virtually free.

Seems Alive to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/JT-and-tesla-image-5-e1537903604840.jpg247350MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-26 01:06:462018-09-25 19:33:07Say Goodbye to That Gas Guzzler

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 19 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Do you expect a correction in the near term?

A: Yes. In fact, we may even see it in October. Markets (SPY) have been in extreme, overbought territory for a month now, the macro background is terrible, trade wars are accelerating, and interest rates are rising sharply. The only thing holding the market up is the prospect of one more quarter of good earnings, which companies start reporting next month. So once that’s out of the way, be careful, because people are just hanging on to the last final quarter before they sell.

Q: I just got out of my cannabis stock, what should I do now?

A: Thank your lucky stars you got away with that—it was an awful trade and you made money on it anyway. Stay away in droves. After all, the cannabis industry is all about growing a weed and how hard is that? This means the barriers to entry are zero. In fact, I’m thinking of growing some in my own backyard. My tomatoes do well, so why not Mary Jane?

Q: The Volatility Index (VIX) is now at $11.79—should I buy?

A: No, the rule of thumb for the (VIX) is to wait for it to sit on a bottom for one to two weeks and let some time decay work itself out. You’ll see that in the ETF, the iPath S&P 500 VIX Short-Term Futures ETN (VXX). When it stops breaking to new lows, that means it’s ready for another bounce. I would wait.

Q: What do you think about banks here? Is it time to get in?

A: No, these are not promising charts. If anything, I’d say Goldman Sachs (GS) is getting ready to do a head and shoulders and go to new lows. I would stay away from financials unless I see more positive evidence. The industry is ripe for disruption from fintech, which has already started. That’s said, they are way overdue for a dead cat bounce. That’s a trade, not an investment.

Q: Would you short Alibaba (BABA) and Baidu (BIDU) here?

A: No. Shorting is what I would have done six months ago; now it’s far too late. If anything, I would be a buyer of those stocks here, based on the possibility that we will see progress or an end to the trade war in the next couple of months. If the trade wars continue, they will put the U.S. in recession next year, and then you don’t want to own stocks anywhere.

Q: Is Apple (AAPL) going to get hit by the trade wars?

A: So far, this has not been the case, but they are whistling past the graveyard right now—an obvious target in the trade wars from both sides. For instance, the U.S. could suddenly start applying a 25% import duty to iPhones from China, which would make your $1,000 phone a $1,250 phone. Similarly, the Chinese could hit it in China, restricting their manufacturing in one way or another. I’m being very cautious of Apple for this reason. The stock already has one $10 drop just because of this worry.

Q:Can the U.S. ban China from selling bonds?

A: No, they can’t. The global U.S. Treasury bond market (TLT) is international by nature—there is no way to stop the selling. It would take a state of war to reach the point where the Fed actually seizes China’s U.S. Treasury bond holdings. The last time that happened was when Iran seized the U.S. embassy in Tehran in 1979. Iran didn’t get its money back until the Iran Nuclear Deal in 2015. Before that you have to go back to WWII, when the U.S. seized all German and Japanese assets. They never got those back.

Q:What are your thoughts on the chip sector?

A: Stay away short-term because of the China trade war, but it’s a great buy on the long term. These stocks, like NVIDIA (NVDA) and Micron Technology (MU) have another double in them. The fundamentals are outrageously good.

Q:Is the market crazy, or what?

A: Yes, it is crazy, which is why I’m keeping 90% cash and 10% on the short side. But “Markets can remain irrational longer than you can stay liquid,” as my friend John Maynard Keynes used to say.

Q: What’s your take on the Consumer Staples sector (XLP)?

A: It will likely go up for the rest of the year, into the Christmas period; it’s a fairly safe sector. The uptrend will remain until it doesn’t.

Q: Should we buy TBT now?

A: No, the time to buy the ProShares Ultra Short 20+ Year Treasury ETF (TBT) was two months ago. Now is the time to sell and take profits. I don’t think 10-year U.S. Treasury yields (TLT) are going above 3.11% in this cycle, and we are now at 3.07%. Buy low and sell high, that’s how you make the money, not the opposite.

Q: Does this webinar get posted on the website?

A: Yes, but you have to log in to access it. Then hover your cursor over My Account and a drop-down menu magically appears. Click on Global Trading Dispatch, then the Webinars button, and the last nine years of webinars appear. Pick the webinar you want and click on the “PLAY” arrow. Just give us a couple of hours to get it up.

Q: Can Chinese companies use Southeast Asia as a conduit to export to the U.S.?

A: Yes. This is an old trick to bypass trade restrictions. For example, most of the Chinese steel coming into the U.S. is through third countries, like Singapore. Eventually they do get found out, at which point companies or imports from Vietnam will be identified as Chinese origin and get hit with the import duties anyway, but it could take a year or two for those illegal imports to get discovered. This has been going on ever since trade started.

Q: Will the currency crisis in Argentina and Turkey spread to a global contagion?

A: Yes, and this could be another cause of a global recession late next year. The canaries in the coal live there (EEM).

Q: Would you use the DOJ probe to buy into Tesla (TSLA)?

A: No, buy the car, not the stock as it is untradeable. This is in fact the third DOJ investigation Tesla has undergone since Trump came into office. The last one was over how they handled the $400 million they have in deposits for their 400,000 orders. It turns out it was all held in an escrow account. There are easier ways to make money. It’s a black swan a day with Tesla. This is what happens when you disrupt about half of the U.S. GDP all at once, including autos, the national dealer network, big oil, and advertising. All of these are among the largest campaign donors in the U.S.

Last quarter’s earnings report sent Netflix shares nosediving to the depths of the ocean floor, and the wreckage saw Netflix’s stock down 24% in 5 weeks.

The short-term weakness in shares was justified after Netflix miscalculated on their quarterly subscriber numbers.

Netflix is still a buy because the wreckage can be salvaged.

In fact, it was never a wreckage to begin with because Netflix boasts the highest grade online streaming product in the industry.

An industry that is benefitting from massive secular tailwinds at its back, from cord cutters and the widespread pivot to mobile platforms.

Netflix has the best product on the market because they have the best strategy – throw $8 billion on content alone and hire the best production team money can buy to churn out content.

The method to their madness has worked and the haul of 23 Emmy’s was a result of this winning formula.

The 23 Emmy’s tied HBO, whose premier series Game of Thrones is still captivating audiences with its mix of graphic sexual exploits and violent tropes.

Several of Netflix’s award winners saluted Netflix’s hands-off approach, who allow these highly paid production specialists the creative freedom to inspire audiences.

For all of Hollywood’s razzmatazz, director’s and actor’s number one major gripe has been that the leash is tight with minimal wiggle room.

It’s not straightforward to change a culture that has developed over a century.

Cross-pollinating Silicon Valley’s lean business model with Hollywood top-grade content was the trick that removed the shackles from the director’s ankles.

The end-product has been the main beneficiary.

Scoping out Netflix’s end of year lineup has viewers drooling.

The tail end of the year sees Netflix reintroduce some hard-hitting content from Orange Is The New Black, Ozark, Daredevil, Narcos, and Making a Murderer, side by side with fresh content involving Simpsons creator Matt Groening and blockbuster names like Jonah Hill and Emma Stone.

As well as shelling out $8 billion for original content, Netflix upped its marketing budget from $1.28 billion to $2 billion in 2018.

The $2 billion budget is a classy touch but at this point, this product more or less sells itself.

The brand awareness is that far-reaching.

The platform is optimized by tweaking Netflix’s proprietary recommendation algorithm herding the audience into viewing more content that the algorithm deems likely viewable.

The man who is in charge of this is Greg Peters - Netflix chief product officer.

Kelly Bennett, Netflix chief marketing officer, will work with Peters to wield the massive $2 billion marketing budget in the most effective way possible.

To insulate the company from any potential Facebook-like data slipups, Netflix poached Rachel Whetstone from Facebook to head up the public relations division.

Who said there were no winners from Facebook’s PR disaster?

Whetstone’s professional year of hell offers valuable insight into how not to pull another Facebook (FB) stinker.

She previously worked for Google and Uber and is a veteran PR spinner.

Earlier this year CEO Reed Hastings detailed the possibility of using ads in Netflix’s ad-less platform by saying this about why Netflix has no ads:

“It is a core differentiator and again we're having great success on the commercial-free path. That's what our brand is about. So we're going to continue to expand the relevance of a commercial free service around the world and make that so popular that consumers are very used to it and appreciate Netflix.”

The relevancy of his statement is more meaningful now after a recently released report confirming that Netflix is testing the usage of ads to promote its content.

This would be a huge shift in the company’s ethos, and if the algorithms give Hastings the green light, this could alienate a big chunk of their subscriber base.

In a survey conducted about the implementation of ads, 23% said they would quit the service if ads are rolled out onto Netflix’s platform.

Only 41% said they would “definitely” or “probably” keep Netflix if ads are introduced.

In the same survey, if Netflix lowers the monthly cost by $3 while integrating ads, the cancellation rate falls from 23% to 16%, and half said they would keep Netflix.

The most important number of the survey was that only 8% would cancel if they increased monthly prices by $2, but if it went up by $5, 23% would say goodbye to the streaming service.

All signs point to an incremental price increase in the near future, partly helping to offset the mind-boggling amount of content spend this year.

Netflix subscribers are still willing to absorb price increases which is a great sign for future profitability.

But it is also worth mentioning that Netflix is a profitable company now, and margins have been slowly creeping up for the past few years.

The tests demonstrate that Hastings is serious about profitability at a time when the premier profit machines in tech are Apple (AAPL) and Alphabet (GOOGL).

These two behemoths blaze the trail for the tech sector and offer important lessons on the potential future profitability of Netflix.

It will take time for Netflix to reach that level of profitability, but the pillars are in place to ramp up the monetization drive.

The treasure trove of data will surely help decision making for the management, but to make their platform more like Facebook (FB) would be a huge error of epic proportions.

It’s proven that digital ads are annoying like a swath of mosquitoes trapped in your bedroom at 2am.

To dilute the quality of their product would fly in the face of what the company represents.

So how on earth will Netflix’s shares go from the mid-$300’s and reach the glorious heights of $400-plus and stay there?

One word – India.

It’s no secret that Netflix has been charging hard to rev up international business.

India is the trump card.

India boasts around 78 million middle class dwellers who can afford Netflix’s service.

In the next two years, it’s feasible that 10% of this socioeconomic class could be tuning into Netflix.

That foothold into India could mushroom, and potentially expand with an audience whose DNA is comprised of a strong film culture.

As broad-brand broadband expansion and smartphone penetration heating up in India, Netflix’s timely arrival could make Netflix look genius.

Their arrival coincides with a slew of American tech companies looking to tap revenue out of the largest democracy in Asia.

The unrealized potential cannot be ignored.

Netflix has primed their strategy by focusing on locally-produced content that will resonate with the Indian viewer.

Netflix’s India strategy started red hot with crime thriller Sacred Games imbued with a level of unfiltered, real filmmaking unseen in India.

The dark crime drama is already facing a legal battle concerning its lusty, foul-mouthed content that presses on the outer limits of what modern Indian society can handle.

The stereotype breaking series directed by Vikramaditya Motwane and Anurag Kashyap is Netflix’s first Indian feather in their cap as Netflix looks to accelerate the momentum.

Netflix has not produced back to back quarters where they failed to meet subscriber growth forecasts since 2012.

I firmly believe Netflix will continue this successful streak and beat subscriber estimates in the third quarter.

Initial indications show that Indians have gravitated towards Netflix’s original content, and with the 2018 Russian World Cup in the history books, the path has opened up for some nice surprises to the upside.

"Health care and education, in my view, are next up for fundamental software-based transformation." – Said Silicon Valley Venture Capitalist Marc Andreessen

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Netflix-India-e1537382336566.png248400MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-09-20 01:05:372018-09-19 21:07:00The Bull Case for Netflix

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.