Mad Hedge Technology Letter

October 25, 2021

Fiat Lux

Featured Trade:

(HOW TO PLAY THE TECH EARNINGS SEASON)

(MSFT), (FB), (GOOGL), (AAPL), (SNAP)

Mad Hedge Technology Letter

October 25, 2021

Fiat Lux

Featured Trade:

(HOW TO PLAY THE TECH EARNINGS SEASON)

(MSFT), (FB), (GOOGL), (AAPL), (SNAP)

The big guns of tech are coming up to the plate for earnings and they could use a strong showing as big tech’s narrative is on the ropes.

They are still the apex warriors of the stock market, and that position is hardly under threat, but there are whispers of a slowdown.

A recipe of high expectations mixed with cruddy forecasts could give us a dip to buy into.

This is what our portfolio would love to be gifted.

Don’t forget we have already seen some misses from tech companies like Snap (SNAP) which plunged 27% after warning that customers are cutting back on digital advertising spending.

The fallout sent other ad tech companies like Twitter and Google significantly lower.

This never used to happen to these companies and that’s important to point out because we just exited an era where ad tech companies could do no wrong.

Now it almost seems like they can’t do no right.

Readers got spoilt, earnings after earnings, these tech companies used to knock it out of the park and much of that high expectation is still leftover, perhaps a legacy concept from the bull market from 2008 to 2021.

These are the bellwether stocks of the broader market that have single-handedly put the rest of their market on their back and carried it higher.

Everyone wants to know if they can still hack it?

Technology companies in the S&P 500 Index are projected to report revenue growth of roughly 19% for the third quarter such as Alphabet at 38% growth, followed by Facebook at 37% and Apple (AAPL) at 31%.

I do believe that they will achieve these lofty estimates but they won’t overperform to the point where buyers line up in spades.

We aren’t in that type of environment now.

These companies have pricing power, and combined with underlying growth drivers, they generate high returns and reinvest in the business and perpetuate that strength.

The price action backs up my concerns with 85% of tech companies having beaten profit estimates, but the stocks have fallen an average of 2.4% the following day.

The lack of response means we are long in the tooth.

If this does become a “buy the rumor, sell the news” type of event, this will give us plenty of discounts to cherry-pick the next day.

The challenge of justifying their valuations means these companies aren’t getting their “free pass” that they used to pocket and manipulate.

They aren’t the darlings of the business world anymore — that title goes to cryptocurrency and bitcoin.

Facebook will tell us how badly Apple’s privacy changes are affecting its ad revenue model.

Consensus is looking for revenue growth of nearly 40% this quarter in Alphabet which in a normal year wouldn’t be that hard to beat but it’s a new normal now.

Ongoing monetization improvements in search advertising through product/AI-driven updates, along with greater-than-expected contributions from businesses like YouTube and Google Cloud can seem them meet their forecasts.

Microsoft (MSFT) expects revenue to grow around 20% in the quarter and we need to look out for if their cloud-computing business maintains strong demand.

Year-over-year comparisons get progressively tougher throughout the year which is an obstacle for MSFT’s durable growth portfolio of Azure/Security/Teams.

Apple could deliver great iPhone sales, but semiconductor shortages are a limiting factor, and the China risk is another big quagmire.

At what point will the Chinese Communist Party stop giving Apple such an easy go of it in China?

Regulatory uncertainty is an overhang — implications of the App Store ruling remain a wild variable.

Amazon is dealing with supply-chain challenges and labor shortages.

Last quarter, revenue missed expectations for the first time since 2018, and the company warned of the reverse of the pandemic-related tailwind for online retail.

Revenue is expected to grow a little more than 16%, the slowest pace since 2015.

The stock has been dead weight this year, which is unlike Amazon.

I do believe we will get a sprinkling of fairy dust that includes margin expansion, but some of these companies will experience a pullback and I will be waiting to aggressively take advantage of these deals.

Global Market Comments

October 25, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TAKING A BREAK)

(MS), (GS), (BAC), (TLT), (TSLA), (AAPL), (AMZN), (GOOGL), (FB)

When I ran the international equity trading desk at Morgan Stanley during the 1980s, there was always one guy I was trying to recruit and that was David Tepper at Goldman Sachs. Whenever we did a trade with David, we lost money.

If we sold David a stock it usually took off like a rocket. If we bought a stock from him it plummeted like a stone. Eventually, unable to lure David over with a monster salary, I had to ban trading with him as it was such a loser for us.

David never did get pried away from Goldman until he left to start his own firm, Appaloosa Management, after he was mistakenly passed over for partner two years in a row. After that, he racked up an annualized return of over 40%, near my own results.

But David was doing it with $20 billion in real money, while I was doing it with newsletters. In 2012, David received a $2.2 billion performance bonus from his fund, one of the largest in history. I bet the partners at Goldman are kicking themselves.

So, I thought it timely to check in with David, now the owner of the Carolina Panthers football team, to see what he thought about the market. The S&P 500, the Dow, Ten-year bond yields, and Bitcoin all simultaneously hit all-time highs last week, and we were long all of them.

David was phlegmatic at best. “There are times to make money and there are times to not lose money, and this is definitely time to make money.” However, nothing is cheap. There are no screaming buys here or screaming shorts. He did expect stocks to keep rising through the end of 2021.

Keep in mind that David is a trader just like me and rarely has a view beyond six months. His last 13F filing on June 30 showed that his five largest positions were T-Mobile (TMUS), Amazon (AMZN), Facebook (FB), Google (GOOG), and Uber (UBER). Uber was the only new buy.

David is not alone in his views.

Up 89.20% so far in 2021, I am sitting here dazed, shocked, and pinching myself. This has been far and away my best year in a 53-year career. I know a lot of you made a lot more. I stared down every correction this year, loaded the boat, and won.

It’s not always like this.

So I think we are in for a few weeks of profit-taking, sideways chop, and minimal action. I call this the “counting your money” time. Traders have visions of Ferraris dancing in their eyes. Then once we form a new base, it will become the springboard for a new yearend rally.

I don’t think stocks will fall enough to justify selling here. And you might miss the next bottom.

Until then, I’m thinking of taking up the banjo.

That brings me to the foremost question in your collective minds. Can I top an astonishing 100% profit this year? Only if we get another great entry point with a 5% correction.

I’m sure that when the financial history of our era is written something in the future, this will be known as the week that Bitcoin went mainstream. That was prompted by the SEC approval of the first futures ETF, the ProShares Bitcoin Futures ETF (BITO).

By giving this approval, which had been sought for years, unlocks $40 trillion worth of assets owned by 100 million shareholders managed under the Investment Company Act of 1940 to go into Bitcoin. The possibilities boggle the mind. The consensus year-end target for Bitcoin is now $100,000, or up 65%.

It’s not too late to subscribe at the founder's rate of $995 a year for the Mad Hedge Bitcoin Letter by clicking here. After that, the price goes up….a lot.

Morgan Stanley (MS) Announces Stellar Earnings, with profits at $3.71 billion, up 36.4%. Morgan Stanley Asset Management sucked in an amazing $300 billion so far in 2021, bringing their total assets to $4.5 trillion.

Goldman Sachs (GS) announces blockbuster earnings, and we are laughing all the way to the bank. Profits soared an eye popping 63% to $5.28 billion.

Existing Home Sales soar by 7% in September to a seasonally adjusted 6.29 million units. First time buyers accounted for only 28%, the lowest since 2015. A brief drop in interest rates is the reason. There are only 1.29 million homes for sale, only a 2.4 month supply.

Housing Starts fall by 1.6% in September. Higher materials and labor costs, rising land expenses, and soaring energy costs are the culprit. A pop in interest rates may mean that the slowdown could last through the winter.

Single Family Rents are surging especially for the top end of the market. Nationally, rents rose 9.3% in August year over year, up from a 2.2% year-over-year increase in August 2020, according to CoreLogic. Buy homebuilders on dips like (KBH), (LEN), and (PHM)

If the Rescue Package passes in whatever size, it will trigger a massive new surge in risk prices, including stocks and Bitcoin. Don’t act surprised when it happens. $3.5 trillion, $1.5 trillion who cares? That’s a ton of money to be dumped into the economy ahead of the 2022 elections.

Tesla profits smash records in Q3, reporting a shocking $1.62 billion profit on $13.76 billion in revenues. A 30.5% profit margin blew people away. Imagine how much they’ll earn when they make 25 million cars a year in ten years. Buy (TSLA) on big dips.

Weekly Jobless Claims dive to 290,000, a new post-pandemic low. Delta is in fast retreat. A pre-pandemic normal level of 225,000 is coming within range.

Rising Interest rates are tagging the Real Estate Market, with the 30-year fixed rate hitting 3.23%. Refis are off 7% on the week. The Fed taper is looming large, especially if the 30-year hits 4.0%, which it should, taking affordability down.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a heroic +9.60% gain so far in October. My 2021 year-to-date performance soared to 89.20%. The Dow Average is up 16.60% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs and those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like having a rich uncle write you a check once a day.

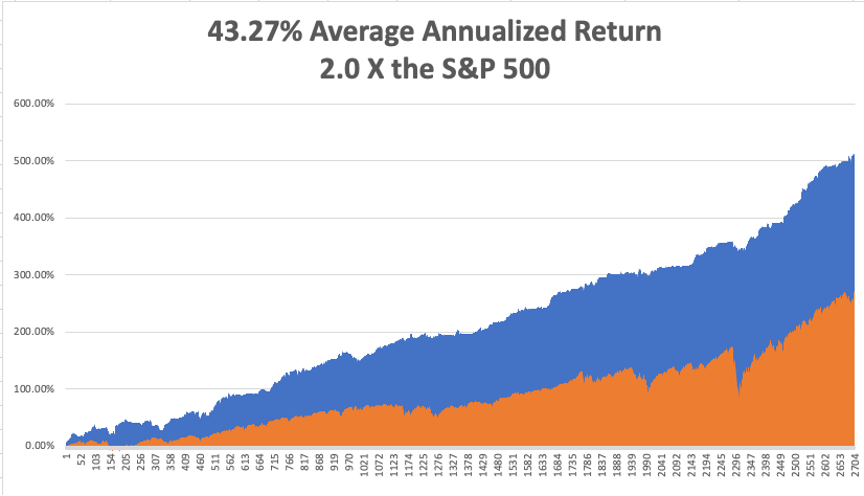

That brings my 12-year total return to 512.75%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 43.75%, easily the highest in the industry.

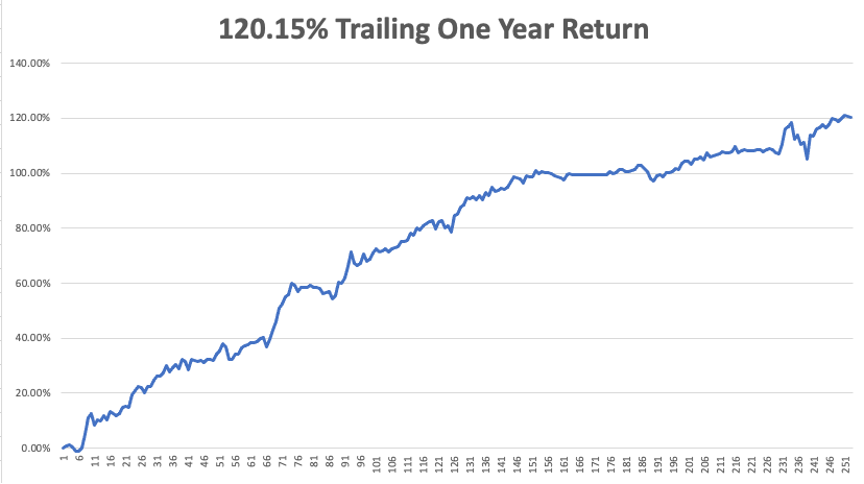

My trailing one-year return popped back to positively eye-popping 120.15%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases approaching 46 million and rising quickly and deaths topping 736,000, which you can find here.

The coming week will be slow on the data front.

On Monday, October 25 at 8:30 AM, the Chicago Fed National Activity Index is out. Facebook (FB) earnings are released.

On Tuesday, October 26 at 10:00 AM, the S&P Case-Shiller National Home Price for August Index is released. Alphabet (GOOGL) and Microsoft (MSFT) earnings are out at 5:00 PM.

On Wednesday, October 27 at 7:30 AM, Durable Goods Orders for September are printed. McDonald’s (MCD) earnings are out.

On Thursday, October 28 at 8:30 AM, Weekly Jobless Claims are announced. The first read on Q3 GDP is announced. Apple (AAPL) and Amazon (AMZN) earnings are out.

On Friday, October 29 at 8:45 AM, the US Personal Income & Spending for September is published. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, when I went to college in Los Angeles, the local rivalries between universities were intense.

UCLA and USC had a particularly intense rivalry, and I went to both. It was traditional to steal Tommy Trojan’s sword prior to each homecoming game and then paint the statue blue. USC had a mascot, a mixed breed dog called “Old Tire Biter.” Prior to one game, UCLA kidnapped the dog.

At halftime, the kidnappers appeared midfield, tied the dog to a helium-filled weather balloon, and let him waft away somewhere over the city. Enraged USC fans stormed the field only to find that the real dog was hidden in a nearby truck. The dog headed for the stratosphere was actually a stuffed one.

Of course, the greatest prank of all time was carried out by the California Institute of Technology in the 1961 Rose Bowl, which didn’t have a football team, on the Washington Huskies. Washington was famous for its elaborate card tricks, which spelled out team names and various corporate sponsors and images.

On the night before a game, imaginative mathematically-oriented Caltech students snuck into the stadium and changed the instructions on the back of each card packet sitting in the seats. When it came time to spell out an enormous “WASHINGTON”, “CALTECH: displayed instead. The incident was broadcast live on national TV ON NBC.

At Caltech, where I studied math, they are still talking about it today.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 22, 2021

Fiat Lux

Featured Trade:

(BOMBSHELL HITS AD TECH)

(SNAP), (FB), (GOOGL), (AAPL)

So, first the good news — SNAP expanded revenue by 57% year-over-year.

It was only a few years ago that this tech company was the backwater of social media, but it’s done its bit to catch up with the crowd.

SNAP targets the 18–29-year-olds and although not minted, there are pathways for a lifetime of revenue generation from this cohort.

In a rough environment battling Google (GOOGL) and Facebook (FB) and despite these challenges, they crossed $1 billion in quarterly revenue for the first time.

That was the good news and now you might want to cover your ears so put on those earmuffs.

The reason SNAP missed guidance by $3 million was because there have been changes to advertising tracking in Apple’s iOS system.

These ongoing changes to digital advertising were introduced as part of iOS 14.5 and were announced ahead of time, and now that move is started to suppress the bottom line for the social media giants.

SNAP anticipated some degree of business disruption, and unfortunately, their provided measurement solution did not scale as expected.

Basically what’s happening is that it’s more difficult for advertising partners to measure and manage ad campaigns for iOS.

Advertisers are no longer able to understand the impact of their unique campaigns based on things like the time between viewing an ad and taking an action or the time spent viewing an ad.

Real-time campaigns and creative management are hindered by extended reporting delays and advertisers are unable to target advertising based on whether or not people have already installed an app.

Without these business analytics, SNAP’s platform is less attractive because sale conversions are a great deal lower.

This impact was compounded by the ongoing macroeconomic effects of the global pandemic with advertising partners facing a variety of supply chain interruptions and labor shortages.

The ongoing magnitude and duration of these global supply and labor disruptions are inherently unpredictable.

Also, businesses do not have the inventory or operational capacity to support incremental demand.

SNAP expect customers to cut marketing budget given the diminished need to drive incremental demand at a time when supply chains are not able to operate at peak capacity.

This in turn that reduces their short-term appetite to generate additional customer demand through advertising at a time when their businesses are already supply-constrained.

The big question is: how bad will the Apple changes impact SNAP in the future?

SNAP is down 25% in today’s trading and that’s just them.

Facebook is down around 6% and Google is also off 3%.

Apple has signaled that they aren’t willing to accommodate the tracking techniques of the social media companies.

Clearly, investors are worried about the magnitude of the drop in shares, and this does a great deal to kill the momentum in the stock.

This isn’t the end of the world because I would like to point out that these changes happened in June and July, yet SNAP was still able to grow revenue by 57% year over year.

But I will say this will crimp the growth elements in the business model and lower the ceiling.

Growth rates of high 50% could start trending towards the lower 40% and investors hate that.

The company is still quite small — less than $90 billion of market cap.

This is exactly what SNAP didn’t want because comparatively speaking, Google and Facebook will be able to absorb this better with their war chest of capital readying itself to plug in the gaps.

The stock essentially gave back a year of performance in one morning, but I do view this as a buying opportunity and readers who have a long-term view will certainly profit once SNAP work itself through this problem, but it will be closer to a crawl up than big gaps up in prices.

Mad Hedge Technology Letter

August 30, 2021

Fiat Lux

Featured Trade:

(A GREAT ALTERNATIVE IN THE AD TECH SPACE)

(SNAP), (AMZN), (FB), (GOOGL), (SDC)

I know many readers gripe about certain tech stocks being too expensive like Google (GOOGL), Facebook (FB), or even Amazon (AMZN), but that’s not the case for all high-quality tech names out there.

There are still deals to be had.

An undervalued tech name in the same industry, albeit more diminutive than the three I just mentioned, is ad revenue platform Snap Inc. (SNAP).

Their story is a good one and their revenue model appears to be maturing at an optimal time while still exhibiting many elements of explosive growth.

To see what I mean — Snap grew both revenue and daily active users at the highest rates they have achieved in the last four years.

Daily active users grew 23% year-over-year to 293 million — expanding revenue by 116% year-over-year to $982 million.

This outperformance reflects the momentum in SNAP's core advertising business and the positive results of their team serving ad partners helping them to generate a return on investment.

SNAP benefited from a favorable operating environment and continued success with both direct response and large brand advertisers — continue to leverage performant ad products to grow an advertiser base globally.

Adjusted EBITDA improved by $213 million compared to last year, marking the third adjusted EBITDA profitable quarter in the last 12 months as SNAP continues to demonstrate the leverage in their business as they scale.

They are also fully absorbed in making progress against revenue and Average Revenue Per User (ARPU) opportunities, which I believe will be driven by three key priorities.

First, driving ROI through measurement, ranking, and optimization.

Second, investing in aggressive sales and marketing functions by continuing to train, hire, and build for scale.

And third, building innovative ad experiences around video and augmented reality, with a focus on shopping and commerce.

The commitment to these three priorities, along with a unique reach and large, engaged community, allows SNAP to drive performance at scale for businesses around the world.

They have proven through results in North America that with a robust team, surrounding resources, and a local focus, they can accelerate revenue.

They are now taking that model and replicating it in several markets that they have identified as having a large digital advertising market and significant levels of existing Snapchat adoption.

It’s true to say they still have a lot of room to grow in some of the world's most established ad markets outside of North America, especially in Europe.

For example, in the UK, France, and the Netherlands, SNAP reaches over 90% of 13- to 24-year-olds — 75% of 13- to 34-year-olds.

SNAP continues to invest heavily in video advertising, with the goal of driving results for advertising partners and connecting them to the Snapchat Generation.

For example, SNAP worked with Nielsen to help U.S. advertisers understand how to more efficiently reach their target audiences via Snap Ads.

The Total Ad Ratings study analyzed how over 30 cross-platform advertising campaigns reached people on both Snapchat and television.

The analysis showed that Snapchat campaigns contributed an average of 16% incremental reach to advertisers' target audiences, and over 70% of the Gen Z audience that was reached by Snapchat was not reached by TV-only campaigns.

This is especially important as people are increasingly cutting the cord, and mobile content consumption continues to grow, presenting SNAP with a large opportunity to help advertisers reach the Snapchat Generation at scale.

Augmented reality advertising is delivering a return on investment that is measurable and repeatable, which is encouraging the incremental businesses to invest in AR.

For example, Smile Direct Club (SDC) leveraged a Goal-Based Bidding Click optimization for Augmented Reality (AR), which drove 49% of Snap customer leads in Q2 and was the most effective ad unit at driving traffic for their business compared to other social channels.

The success of the Lens ultimately encouraged Smile Direct Club to include AR Lenses as part of their long-term business strategy.

SNAP is betting the ranch on efforts to help advertisers improve conversions and ROI, and recently launched optimization for AR, which allows advertisers to optimize their AR campaigns for down-funnel purchases and fits well into the broader shopping strategy.

SNAPs bread and butter region of North America is hitting on all cylinders with revenue growing 129% year-over-year in Q2, while ARPU grew 116% year-over-year as they continue to benefit from significant investments made in sales teams and sales support in the prior year.

At a 30-thousand-foot level, the global internet services market was valued at over $450 billion in 2020, the year in which the pandemic fundamentally altered how society functions, accelerating a push towards digital offerings.

The internet market is expected to grow at a compound annual growth rate of 5% through 2027 and reach a value of $652 billion. US-based equities presently control close to 30% of the total global market share in the industry.

My takeaway from this is that even though there is GOOGL and FB in this space, the pie is growing so fast that there is easily room for others like SNAP.

One must believe that if SNAP keeps operating anywhere close to its pandemic performance relative to other companies, they are surely guaranteed to be a buy-the-dip company.

In terms of price action, that’s exactly what we have witnessed as the price has zig-zagged up by 300% — the stock price goes two levels up and retraces back one — rinse and repeat.

Just view the big down days as optimal entry points into a burgeoning social media platform and deploy capital.

In the short term, on the monetization side, I have to note that the fiscal comparisons will be more challenging in the second half as SNAP begins to lap the acceleration in top-line growth that they experienced in the prior year.

Once that sell-off gets baked into the equation via a 3-5% sell-off, readers should jump back into SNAP.

Global Market Comments

August 26, 2021

Fiat Lux

Featured Trade:

(GOOGLE’S MAJOR BREAKTHROUGH IN QUANTUM COMPUTING),

(GOOGL), (IBM)

Global Market Comments

August 19, 2021

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (MS), (GS), (BABA), (EEM), (FXA), (FCX), (GLD), (SLV), (TLT)