Mad Hedge Technology Letter

September 5, 2018

Fiat Lux

Featured Trade:

(WARREN BUFFETT’S GREAT TECH FIND IN INDIA),

(BRK/B), (AAPL), (GOOGL), (MSFT), (BABA), (NFLX)

Mad Hedge Technology Letter

September 5, 2018

Fiat Lux

Featured Trade:

(WARREN BUFFETT’S GREAT TECH FIND IN INDIA),

(BRK/B), (AAPL), (GOOGL), (MSFT), (BABA), (NFLX)

Warren Buffett preaches searching among your “circle of competence” to find those gems of companies that will offer abundant value in the far future.

His time horizon has always been long – 10, 20, 30 years where a company has sufficient time to execute its business strategy.

The celebrated investor’s track record is unrivaled.

Another critical rule to his playbook of uncanny success is to invest in companies within your area of expertise to avoid erroneous investment decisions.

If an investor is uncertain if a company is within its “circle of competence,” then it is likely outside the circle and best to skip investing in the company for now.

The Oracle of Omaha has taken his investment playbook to the chicken tikka masala-loving country of India, dropping a few Benjamín’s on One97 Communications Ltd., the parent company of Paytm, an Indian fin-tech firm.

This disrupting digital payments company based in Noida, India, is the nation’s largest mobile-payments firm and quite an achievement in a country that loves paper cash.

It boasts a popular smartphone app used in daily lives, and mirrors digital payment businesses of the likes of China’s Alipay or Tencent’s WeChat payment platform.

When the Indian government laid down the heavy hand of fiscal regulation on the paper currency market with an eye toward the digital currency market, an outsized winner was Paytm.

The cost of printing paper money in India per year is more than $90 million by itself.

I am not saying that the Indian government is going into overdrive adopting bitcoin tomorrow, but its pivot toward fin-tech mobile payments and Buffett’s vote of approval show where all the deep lying tech value is marinating in the world.

It is not Silicon Valley that gets more expensive by the day.

Silicon Valley is largely saturated with venture capitalist firms cherry-picking the best firms before they go public and making many times their investment once they hit the New York public markets.

Well, we are still in the early stages of India’s rapidly developing tech scene. And 2018 has seen some blockbuster cash injections such as Walmart’s investment in e-commerce juggernaut Flipkart.

Buffett has championed investing into companies with a “margin of safety,” allowing him to buy stakes at levels he believes that are well below market value.

This allows him to sleep at night because even if the company tanks short-term, he knows that eventually it will pull it together.

India can now lay claim to more than 390 Internet users, and 300 million of those use Paytm.

When 77% of a country’s population is using an app, you know there is some staying power, as the first mover advantage in the tech world has a powerful and long-term network effect such as the AWS’s foray into the cloud business.

Paytm does have a crowded lineup of heavyweights breathing capital into its company in the form of investments from Masayoshi Son’s SoftBank Vision Fund and Jack Ma’s Alibaba (BABA).

China’s presence in the Indian tech scene is strong, but it has not doubled down there as it has in Southeast Asia, where it enjoys a healthier political connection that is largely void of border skirmishes.

India is the largest democracy in Asia and a strong ally of the United States. Although American tech companies won’t be welcomed with a pristine red carpet, they do have ample opportunity to invest in the burgeoning Indian tech scene.

Buffett’s stake amounts to a 3% to 4% stake in Paytm, and the valuation has spiked to more than $10 billion.

This comes on the heels of Buffett’s adding to his position in Apple (AAPL) that sees him now own 5%.

Apple’s services division is its new cash cow and is on track to eclipse $50 billion in annual revenue next year.

Apple’s services division surpassed $30 billion in the first three quarters of 2018. Its evolution comes at a timely period where smartphone growth has peaked while invaded by low-quality Chinese substitutes.

After sliding to annual low’s in April 2018 of $160, Apple has literally gone ballistic, powering past the $1 trillion valuation mark and is trading at all-time highs around $230.

Apple is another example of why this bull market is predominantly propped up by tech companies that continue to grow earnings at an insane pace.

Only a few companies have fallen into booby traps set forth by the regulatory hurdles first set by the Europeans and General Data Protection Regulation (GDPR).

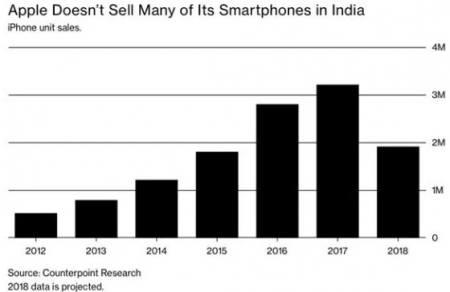

Apple is losing its smartphone battle in India, but Indians can’t afford iPhones yet and even Netflix (NFLX) is seen as an expensive streaming service.

The average Indian does not possess the purchasing power that North America and Europe have.

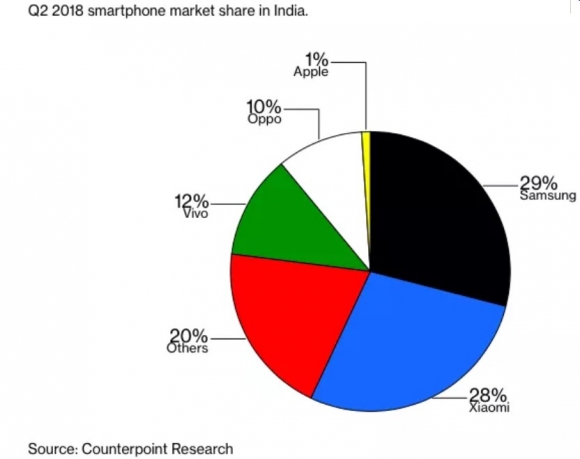

Apple has only extracted 1% of smartphone sales in India compared to leader Xiaomi, which leads the market with a 28% share. Further down-market Chinese phone maker Oppo lags with 10% and Vivo with 12%.

It doesn’t matter for Apple.

Apple continues to milk the North American and European markets to great effect padding profits with its high-quality services business.

China was the undeveloped market that launched Apple’s profits sky high. And American tech companies are ostensibly using this same strategy in India and hoping to cement the best strategy for revenue down the road.

Buffett’s investment is finally a green light for India if there ever was one, and every Silicon venture capitalist has to be licking their chops to squeeze value out of India.

The value is deep lying, but it will pay dividends within five to 10 years as India’s economy rises with its citizen’s discretionary income.

With every Tom, Dick, and Harry lusting after the India market, it will drive valuations firmly higher for the foreseeable future.

The fear of missing out (FOMO) will expedite the pivot toward India where many of the most conservative investors could ironically end up.

The tech relationship between America and India is demonstrably synergistic with Indian born CEOs heading Google (GOOGL) and Microsoft (MSFT) among other influential tech companies.

Berkshire’s (BRK/B) funds join the Chinese, Japanese, and Silicon Valley venture capitalist’s capital queuing at India’s front door awaiting to unlock value.

Buffett even opted out of investing in ride-sharing behemoth Uber, because apparently the “margin of safety” was not sufficient enough in the proposal.

Buffett was even quoted on a local Indian television station gushing about the country saying, “If you’ll tell me a wonderful company in India that might be available for sale, I’ll be there tomorrow.” That day has surfaced in the form of his investment in Paytm.

Apparently, Buffett’s expertise lies in India now and Indian-born Ajit Jain is one of four Berkshire executives running the company on a day-to-day basis.

This will pave the way for more tech investments in the swiftly evolving Indian tech scene, and Berkshire will ring in the profits of these Indian assets down the road.

________________________________________________________________________________________________

Quote of the Day

“Our favorite holding period is forever,” – said legendary American investor Warren Buffett.

Mad Hedge Technology Letter

September 4, 2018

Fiat Lux

Featured Trade:

(READY PLAYER ONE’S INSIGHT INTO THE FUTURE OF TECHNOLOGY),

(MSFT), (SQ), (TTWO), (AMD), (NVDA), (EA), (ATVI), (PYPL), (GOOGL), (FB)

The technology-laced film Ready Player One gives viewers a snapshot into the future where technology, income inequality, and society have run their course, and the year 2045 looks vastly different from the world of 2018.

Set in a semi-dystopian backdrop, the movie offers us a deeper insight into how certain technology trends will permeate into everyday life.

The first and most obvious future trend is the copious use of avatars.

Avatars will become the new normal. The first place that humans will find them is through the use of social media and entertainment, as children eventually becoming a part of us like our social media profiles today.

The Mad Hedge Technology Letter has incessantly hammered home about the phenomenon of gaming, and this will incorporate virtual reality allowing gamers access to a new digital world.

This was the on show in the film where the likes of protagonist Wade Watts, played by Tye Sheridan spent most of his life playing in the virtual world of Oasis using his character Parzival.

This could be your child in the future.

Wade Watts character is the new cool for Generation Z, as they are largely unconcerned about underage drinking and partying like the generations before them.

Gaming and hanging out on their preferred social media platforms are the new cool.

The companies dictating the current video game industry will have the first crack at it to realize profits and develop new businesses such as Microsoft (MSFT), Nvidia (NVDA), Advanced Micro Devices (AMD), Electronic Arts Inc. (EA), Take-Two Interactive Software, Inc. (TTWO), and Activision Blizzard, Inc. (ATVI).

Children just aren’t going outside like they used to and per most studies, they are addicted to the smartphone you bought them at age 10.

Most studies have found that once a child becomes hooked on technology, it is hard to reverse the habit, as once they enter into adult life and start their career, they become even more reliant on the technologies that got them to that point in the first place.

If your kid is already staring at tech devices three to four hours per day now for activities other than school work, expect that to grow to a minimum of six to seven hours per day once he hits puberty and smartphone time limits begin to fade away.

This all means that VR and gaming could be the handsome winner in all this, and the use of social media platforms will reap the benefits as well.

Generation Z just surpassed Millennials in terms of population comprising 25% of the American populace.

Neither of these generations have grown up with VR in their daily lives because the technology wasn’t advanced enough to really make a dent in their lives.

More than 75% of Generation Z has access to a smartphone, and they can truly be called the first generation of digital natives.

Avatars will push deeper into everyday life because the facial tracking technology has advanced by leaps and bounds.

Instead of cartoon-like avatars, lifelike avatars have replaced the less refined versions. It will be a tough time going forward distinguishing what is real and what is fake.

If you think fake news is a problem now, imagine how fake it will become in the future.

This could devastate the news industry as news organizations run the risk of melting down at any point, or just being completely taken over by tech companies and their algorithms, which is already happening now with Alphabet (GOOGL).

The future looks bleak for all newspaper assets, and the ones with the most advanced digital strategies will survive.

Newspapers only have so much time they can hang on with digital ad revenue, the reason they are still in business.

Viewers don’t want to see ads – period. And at some point, they will be disrupted as well.

Swashbuckling youth already have downloaded ad-blockers to completely remove ads from their lives, and refuse to open any website that forces them to white list a website.

There are children in Generation Z who might never have seen an ad before because their digital native capability allows them to navigate around ads with adept skill.

Or the easy solution for many Millennials is just watch Netflix because the platform is ad-less. The aversion to ads is so strong that traditional media giants such as Fox are experimenting with six-second ads because that is all a viewer can tolerate these days.

The traditional media giants were forced to adopt this new format after Alphabet’s YouTube rolled out micro-ads.

Popular browser Mozilla announced it will block all tracking scripts by default beginning in 2019, thwarting unregulated data collection and relentless ad pop-ups.

The reason why digital ads will have an existential crisis is because companies will be able to monetize the pure data, forcing companies with huge digital ad businesses such as Facebook (FB) to battle with the new competition that only wants your data and not hawk ads.

This is already happening in the e-brokerage space with disruptors such as Robinhood, which charges no commission and is more interested in collecting data and getting by with interest payment revenue.

Let’s face it, digital ads are not a high-quality business even though they are a high-margin business. As tech moves forward, the quality of tech will rise eliminating all low-grade tech that is still profiting in 2018.

On the business side of things, automation is replacing humans faster than humans realize, and the replacement will be an avatar representing the face of a company.

For lower-end services, an avatar chosen by the customer will populate to often give better service than a human can provide.

If this type of service is scaled, it would offer a massive cut in costs for American corporations saving on employee costs.

It will have the same effect that self-checkout kiosks have at supermarkets, wiping out another position at the low-end.

The front-end avatar that will service you is all possible because of the rapid advancement of artificial intelligence.

Every possible situation will be programmed in the software and executed briskly.

If customers desire the human touch, they will have to pay up.

Human interaction will command a premium price because human interaction cannot be automated.

The financial industry has a huge target on its back, and swaths of financial advisors could be sacked in favor of avatars with the functional software behind it to produce profits.

In fact, many financial advisors are instructed to refrain from recommendations now and urged to collect input to enter into a proprietary algorithm that will decide the customers’ portfolio.

Big banks have enjoyed their time in the sun, but technology will disrupt them in the near future. This is why you have seen huge run-ups in innovative fintech companies such as Square (SQ) and PayPal (PYPL).

Many forms of outside entertainment are on the chopping block, as well as indoor entertainment such as Hollywood.

Hollywood A-list actors command hefty premiums to contract their services, and that could all crumble if younger audiences prefer avatar-based films with the human roles performed by unknowns.

Johnny Depp earns more than $50 million for one movie, and these insane amounts could deflate rapidly if human participation in films becomes marginalized.

Ready Player One was a test case for how much technology could be infused into a movie, and the audience easily absorbed it.

I could argue that audiences could argue even more in this VR format.

The movie had a budget of $175 million, and returned $582 million at the box office.

The resounding success will encourage more directors to inject technology into their movies, and they will have to, if they hope to tempt younger audiences to the movie theater.

Going to the movie theater is another activity that has struggled to cope against the rise of Netflix and technology.

Theaters have been forced to improve the overall experience of watching a film with prime seating, comfortable seats, and other extras that never existed.

Every industry is going through the same headache of competing with technological disruption.

Stagnation is akin to surrendering in 2018.

And it wasn’t just a fringe director creating Ready Player One, it was visionary director Steven Spielberg, one of the most famous movie directors to ever exist.

This will pave the way for other lesser-known movie directors relying on technology to pump out the profits.

They wouldn’t be the first people or the first industry to go down this road either.

________________________________________________________________________________________________

Quote of the Day

“The worst thing a kid can say about homework is that it is too hard. The worst thing a kid can say about a game is it's too easy,” – said American media scholar Henry Jenkins III.

Mad Hedge Technology Letter

August 30, 2018

Fiat Lux

Featured Trade:

(ON TRUMP’S TECHNOLOGY ATTACK),

(AMZN), (GOOGL), (FB), (AMD), (TWTR)

First Amazon (AMZN), now Alphabet.

In a strategic move to fortify his base ahead of critical midterm elections, the President of the United States Donald J. Trump has denounced tech behemoth Alphabet (GOOGL) describing search results using his name as “rigged.”

If Trump loses the midterm elections, it could open a can of worms and threaten his position.

It is no surprise that he plans to invest 40 days traveling around America campaigning for Republicans in November.

This is a big deal.

Silicon Valley has been a frequent bashing target for the White House.

The data privacy fiasco of 2018 has offered ample ammunition to pretty much anyone who wants to rain on big tech’s parade.

Big tech has experienced a wave of bad press shifting public opinion against them ruining future guidance for social media companies such as Facebook (FB).

How does the administration’s attack against Alphabet affect its stock price going forward?

It won’t even blink.

Alphabet’s stock barely budged after the President used his Twitter (TWTR) feed to sound off against the famous digital search engine company.

The stock closed down 0.83% on the day.

We have seen this story again and again with the administration lashing out at certain sectors or individuals, only for the stock market to shrug off any resemblance of weakness and power higher to new all-time highs.

Resiliency would be the best way to characterize this market.

Ironically, Trump found time yesterday to tweet that the Nasdaq had just surpassed 8,000 for the first time, showing off the tech strength underpinning the nine-year bull market.

The FANGs are front and center the stars of the show. Grumbling about a prominent member of this cohort will do nothing to stop the profit engines that tech companies have constructed.

Stellar corporate earnings are the secret sauce in this recipe and investors would be crazy to veer away from that.

Investors have no reason to panic because the tech narrative will not go away anytime soon, and the market knows that.

Political turbulence has been baked into the pie, and it would be eerie if the airwaves went silent.

Investors have largely avoided pinpointing non-economic issues and focused on the economy and its robust 4% growth rate.

It helps that the unemployment rate has fallen to 3.9%, and the full labor market is a net positive, even though inflation and wage growth has yet to contribute as much as initially hoped.

Of course, politics play a substantial role in influencing the stock market. But looking back at the past crisis, the stock market reacted the same as it will now and go much higher.

The market is still very much a tech story, and last week’s price action confirmed this.

The Mad Hedge Technology Letter is still net negative on chip stocks, but the two chip stocks that circumvent my negative calls are companies I recommended recently and that have seen a breathtaking leg up.

Not all chip companies are made equal and Advanced Micro Devices, Inc. (AMD) proved that by spiking 35% so far in August, 23% in the past week, and more than 140% this year.

The hockey stick move has seen (AMD) short sellers singed to a tune of $3 billion in 2018.

Chip stocks were supposed to get crushed by the weight of the trade war. However, these two stalwarts prove that if you are in the right names, you’ll avoid the carnage, which has beset many smaller chip companies that have the bulk of revenue tied to China.

Tech companies have bought back more than $1 trillion of their own stock since the beginning of 2009 because they have the money to do so.

Silicon Valley companies continue to purchase back their own stocks at a furious pace, putting a floor under many cash cow tech firms to the benefit of share prices.

Whether you want to believe or not, the market is metamorphizing into an all-tech story as every sector migrates to the cloud and the heavy use of big data.

Industrial giants are turning into industrial IoT companies.

Turn over any stone and you would be hard pressed to not find some sort of tech in new products.

Silicon Valley is on the cusp of rolling out its self-autonomous driving technology for commercial operations with Alphabet’s subsidiary Waymo.

If that wasn’t a good reason to buy Alphabet, then let’s review the other positive levers in their portfolio.

Alphabet is one member of a two-man team dominating digital advertising revenues with Facebook.

Global media spend is expanding at 13% YOY as the migration to mobile sees no end.

Google has the best search engine in the world. There are no competitors even close to supplanting its holy grail search engine business, unless you consider bing.com a worthy competitor, which it isn’t.

Data is the new oil, and Alphabet is able to douse itself in data because of the gobs it possesses.

This is the reason Google knows everything about most people in the world outside of China.

Alphabet will be able to leverage this enormous treasure trove of big data and monetize it using artificial intelligence technology.

Add it all up and Alphabet is massively profitable and positioned on the vanguard of every future groundbreaking technology in the world.

Picking on the big boys won’t do much, and the stock price will power on unabated for the foreseeable future.

As the midterm elections draw closer, Trump could also double down on his foreign exploits attempting to consolidate political capital.

That means virulently attacking China’s trade policy, which could go into overdrive as they could give him the source of expansive buffer for which he is looking.

However, it is a double-edge sword as many constituents in red states could be the recipient of higher costs that elevated tariffs would bring.

At the bare minimum, Trump has cast a light on China’s unfair trading policies that has tapped an uneasy nerve for many other countries quietly agreeing with the American president.

This could create a whack-a-mole scenario as China could experience growing problems with numerous undeveloped countries felt wronged, and these headaches could take on different forms such as the Forest City project in Malaysia.

Back in the equity world, the smaller chip companies are baring the brunt of the administration’s scathing rhetoric toward China, but the economy, stock market, and consumer health will hum along as if nothing happened.

The damage is limited, giving Trump sufficient leeway to speak out about side issues as the vital midterm elections roll around.

The bull market is not close to dying and there is still room to run.

________________________________________________________________________________________________

Quote of the Day

“Technology itself is neither good nor bad. People are good or bad,” – said former CEO of InfoSpace, Inc. and cofounder of Moon Express Naveen Jain.

Mad Hedge Technology Letter

August 29, 2018

Fiat Lux

Featured Trade:

(THE BEST TECH STOCK YOU’VE NEVER HEARD OF),

(TTD), (AMZN), (GOOGL), (NFLX), (BIDU), (BABA), (SPOT), (P), (FB)

If you asked me which is the best company that most people do not know about then there is one clear answer.

The Trade Desk (TTD).

This company was founded by one of the pioneers of the ad tech industry Jeff Green, and he has spent the past 20 years improving data-based digital advertising.

Green established AdECN in 2004 and its claim to fame was the world’s first online ad exchange.

After three years, Microsoft gobbled up this firm and Green stayed on until 2009 when he launched The Trade Desk. This is where he planned to infuse everything he learned about the digital ad agency into his own brainchild.

Green concluded that creating a self-service platform, avoiding privacy issues, and harnessing big data for digital ad campaigns was the best route at the time.

Green hoped to avoid the pitfalls that damaged the digital ad industry mainly bundling random ads together that diluted the quality and potency of the ad campaigns.

It did not make sense that a digital ad for baby diapers could be commingled with an ad for retirement homes.

Green created real-time bidding (RTB), which is a process in which an ad buyer bids on a digital ad and, if won, the buyer’s ad is instantly displayed on the selected site.

This revolutionary method allowed ad buyers to optimize ad inventory, prioritize ad channels, and boost the effectiveness of campaigns.

(RTB) is a far better way to optimize digital ad campaigns than static auctions, which group ads by the thousand.

In real time, advertisers are able to determine a bespoke ad for the user to display on a website. Green used this model to develop his company by building a platform tailor-made to execute (RTB).

Naturally, he won over many naysayers and his company took off like a rocket.

Results, in a results-based business, were seen right away by ad buyers.

A poignant example was aiding a performance-based ad agency in trimming ad waste by more than 50% for a national fast food chain with thousands of locations across America.

It took just one year for The Trade Desk to carve out a profitable business as ad agencies flocked to its platform desiring to take advantage of (RTB) or also commonly known as programmatic advertising.

Customer satisfaction is evident in its client retention rate of 95% for the past few years highlighting the dominating position The Trade Desk possesses in the digital ad industry.

The Trade Desk has not raised fees for ad buyers lately, but the value added from The Trade Desk to customers is accelerating at a brisk pace.

A great value proposition for potential clients.

The vigor of the business was highlighted when Green cited that each second his company is “considering over 9 million ad opportunities” for their ad inventory shows how The Trade Desk is up to date on almost every single ad permutation out there.

This speaks volume of the ad tech, which is the main engine powering the bottom lines at Google search and rogue ad seller Facebook (FB).

Google only gets 63,000 searches per second and shows that The Trade Desk has pushed the envelope in providing the best platform for ad buyers to seek its perfect audience.

Green’s mission of supporting big ad buyers optimize their ad budget has really caught fire and in a way that is completely transparent and objective.

The foundations that Green has assembled became even more valuable when Alphabet (GOOGL) chose to remove DoubleClick IDs, which would now prevent ad buyers from cross-platform reporting and measurement.

Previously, DoubleClick ID could cull data from assorted ads and online products based on a unique user ID named DoubleClick ID.

Ad purchasers then would data transfer to pull DoubleClick log files and measure them against impressions served from other ad servers across the web.

Effectively, ad buyers could track the user through the whole ad process and determine how useful an ad would be to that specific user.

In an utter conservative move to satisfy Europe’s General Data Protection Regulation (GDPR), DoubleClick IDs are no longer available for use, and tracking the ad inventory performance from start to finish became much harder.

Cutting off the visibility of the DoubleClick ID in the DoubleClick ecosystem was a huge victory for The Trade Desk because DoubleClick ID measured 75% of the global ad inventory.

Ad buyers would be forced to find other measurement systems to help calculate ad performance.

Branding and executing as the transparent and fair ad platform helping ad agencies was a great idea in hindsight with the world becoming a great deal more sensitive to data privacy.

The Trade Desk is perfectly placed to reap all the benefits and boast excellent technology to capitalize on this changing big data landscape. It is already seeing this happen with new business wins including large global brands such as a major food company, a global airline, and another large beverage company.

The global digital ad market is a $700 billion market today and trending toward $1 trillion in the next five to seven years

The generational shift to mobile and online platforms will invigorate The Trade Desk’s bottom line as more big ad buyers will make use of its proprietary platform to place programmatic ads.

Content distribution systems are fragmenting into skinny bundles hyper-targeting niche content users such as Sling TV, FuboTV, and Hulu.

There are probably 30 different ways to watch ESPN now, and these 30 platforms all require ad placement and optimization.

Some of the names The Trade Desk is working with are the who’s who of digital content ownership or distribution including Baidu (BIDU), Google, Alibaba (BABA), Pandora (P), and Spotify (SPOT) -- and the names are almost endless.

It’s the Wild West of ads and content these days because TV distribution has never been more fragmented.

Content creation avenues are desperate to boost ad income and are increasingly attempting to go direct to consumers.

Ad-funded Internet TV barely existed a few years ago. And ad inventory is all up for grabs benefitting The Trade Desk.

All of this explains why the stock is up more than 180% in 2018, and this is just the beginning.

The growth numbers put Amazon (AMZN) and Netflix (NFLX) to shame.

The Trade Desk scale on inventory has spiked by more than 700% YOY.

The option to hyper-target increases as more ad inventory is stocked.

Management mentioned in its second-quarter performance that “nearly everything went right. We executed well and one of the most dynamic environments we've seen.”

It is one of the most bullish statements I have heard from a public company.

Quarterly revenue ballooned 54% YOY to a record $112 million, and the 54% YOY growth equaled the 54% YOY growth in Q2 2017.

Ad Age's top 50 worldwide advertisers doubled ad spend in the past year positioning The Trade Desk for continued hyper-growth, not only for 2018 but in 2019 and beyond.

Mobile spend jumped nearly 100% YOY, accounting for 45% of ad spend on the platform, which is 400% higher than the industry average for mobile ad spend according to eMarketer.

Data spend was also a huge winner rising by nearly 100% smashing another record.

In the meantime, the overseas business continued its robust growth in Europe and Asia, up 85% YOY.

The Trade Desk confidence in its performance chose to increase guidance to $456 million for the year, a 48% YOY improvement.

When upper management says “when we see surprises, they typically are to the upside” you take notice, because this tech company is perfectly placed in a growth sweet spot.

Massive developing markets are just starting to dabble with programmatic advertising. Markets such as China will see it become the new normal soon, opening up even more business for The Trade Desk.

The Trade Desk is also rolling out new products that will automate more of the process and reduce the number of clicks.

Wait for the pullback to get into this ad tech stock because even though it is up big this year, we are still in the early innings, and shares will march even higher.

________________________________________________________________________________________________

Quote of the Day

“I have a deep respect for the fundamentals of television, the traditions of it, even, but I don't have any reverence for it,” – said Netflix chief content officer Ted Sarandos.

Mad Hedge Technology Letter

August 27, 2018

Fiat Lux

Featured Trade:

(WHY ALIBABA IS THE FIRST STOCK TO BUY WITH THE OUTBREAK OF TRADE PEACE),

(BABA), (GOOGL), (AMZN), (YELP), (MSFT), (MU), (ZTE), (HUAWEI)

According to the government agency, China Internet Network Information Center, the Chinese Internet community has surpassed 802 million, which only represents a 57.7% penetration rate, miles behind the 89% penetration rate in America.

The gargantuan scale of the Chinese Internet world means China has three times as many Internet users than America, and this is a big deal.

The additional 30 million added to the Chinese Internet ecosphere in the first half of 2018 shows the scale in which local Chinese tech companies are playing with and use to their clear-cut advantage.

Ostensibly, most business strategies in China revolve around scaled tactics as the backbone to operations.

There is even more room to expand in the Middle Kingdom and one clear victor sits atop the parapet looking at the riffraff below and that is Chinese Internet conglomerate Alibaba (BABA).

Alibaba, led by Chinese Internet pioneer Jack Ma, posted its highest-performing growth quarter in the past four years.

Total quarterly revenue ballooned an incredible 61% YOY to $11.8 billion, highlighting the dominant position Alibaba possesses in the Chinese e-commerce landscape.

If you want to know what Amazon (AMZN) is going to do next watch Alibaba.

Profit margins were somewhat sacrificed in the process because of M&A activity that saw Alibaba move into the physical supermarket business snapping up 35 Hema supermarket locations then reinvesting into the business. Echoes of Whole Foods?

Alibaba did not stop there, funneling another $3 billion into food delivery app ele.me, which plans to merge its operations with Yelp (YELP) lookalike app Koubei.

If you thought Silicon Valley moves at a rapid pace, the Chinese Internet space moves faster than lighting.

Alibaba last year dipped into the retail segment as well pocketing a department store chain with 29 stores along with 17 shopping malls.

Alibaba is the closest replica the world has to Amazon and thus is an ideal barometer of the health of the overall Chinese consumer and a peek under the complicated hood that is the Chinese economy.

Alibaba also provides onlookers at how China and its Internet behemoths are coping with the global trading war that has invaded the news headlines from its outset.

The short answer to all this is that China is coping quite well and by no means is ready to back down.

Indeed, there will be peripheral pressures exerted from the fringes, but the core engines remain intact and Chairman Xi can fall asleep in his Beijing abode more than peacefully.

A reason for the stalemate between the two governments is that both are quietly confident they have the levers in place to absorb whatever Molotov cocktails the other has to throw at them.

Investors would be mad to dismiss China’s capabilities after experiencing a mesmerizing economic rise enriching hundreds of millions of Chinese nationals that can be found comfortably living in western megacities in luxury real estate often with a real estate portfolio dotted around the world.

Alibaba’s management made it known on the earnings report that it is not worried much about the trade war because it is largely focused on the domestic Chinese consumer, which has been one of the best economic stories of the past decade.

The overseas expansion unfolding under Alibaba’s tutelage is away from the western world and predominantly focused on Southeast Asia and Eastern Europe where cheap, value-for-money hardware and software allows citizens at these income levels to participate in the e-commerce game.

These individuals can’t afford iPhones on a salary of peanuts. And Alibaba has targeted the undeveloped world as a potential lever of substantial growth.

The regulatory harshness of the west has shut out Huawei and ZTE from its shores. Australia followed suit as well, banning the two telecom companies even though it enjoys a better relationship with Beijing than Europe or North America.

China has already planned a workaround because the engines driving the Chinese tech miracle are semiconductor companies such as Micron (MU), which sells boatloads of DRAM memory chips to Chinese tech companies that flood the world with smartphones and other gadgets.

Beijing has already formulated a plan to circumvent American chips by tapping Korean, European, and Japanese chips to replace the current American supply that could vanish at any time.

Shenzhen-based chip company HiSilicon fully owned by Huawei is responsible for supplying Huawei with chips and is the biggest local designer of integrated circuits in China.

This is what the future of China looks like when China can finally build up the adequate supply necessary to achieve its plans to dominate global technology, America, and the world.

But the plan is still in the process of playing out. The awkwardness was highly visible when the administration’s ban of selling U.S. manufactured components to telecommunications company ZTE resulted in the company almost shutting down until a last-second change of heart by the administration.

The near-death experience will invigorate ZTE to muster its own local supply of chips to avoid the unreliable foreign supply and a deja vu feeling.

American chip companies won’t be able to enjoy the Chinese market for long as all these negative experiences for Chinese companies has forced Chinese tech companies to search and secure a guaranteed chip supply.

At the same time, Chinese local smartphone players have gone from 0 to 60 in no time with companies that barely existed a few years ago, such as Oppo, Vivo coming into the fore along with Huawei picking up 43% of the global smartphone market.

This is bad news for Apple as local competitors are learning fast and furious how to build premium smartphones via re-engineering the current technology or through forced technology transfers.

These companies subsequently offer these phones at the lowest possible price point. And at some point in the near future Apple could be expendable if Chinese smartphones start to display the type of quality the best phones show.

Chinese domestic consumption and investment comprise 90% of the GDP growth in China and are propped up by three robust trends including real wage growth boosting the middle-class population, high savings rate that of which Americans would be jealous, and easy access to credit vehicles.

When I was recently in the Middle Kingdom, it was highly evident that as the generations became younger, their quality of life was higher than their parents.

The opposite is happening in America with millennials earning demonstrably less than their parents’ generation while the American middle class is shrinking at an accelerated pace.

Beijing knows this and hopes to wait things out as it feels time is a positive variable for China and not America.

It is true that if this trade war took place in 20 years in the future, China would be in a stronger strategic position to extract whatever concessions it desires because even though Chinese growth is slowing, it is still growing at 6.5%.

And if you don’t believe what I just said then just look at Alibaba’s cloud division, which grew 93% YOY opening artificial intelligence-based data centers around Europe to battle Amazon (AMZN) and Microsoft (MSFT).

Europe was once Elysian Fields for American tech companies, but with European regulators going after American tech and China encroaching on European turf, the future looks a lot less certain for the FANGs there than ever before.

Alibaba’s operating margins dipped 10% YOY but the slide will be returned to shareholders in the future in the form of high-quality revenue and is worth the investment into the most innovative ideas of tomorrow.

I did not even mention the large stake Alibaba has in Ant Financial, which operates the ubiquitous digital payment app Alipay.

It would be analogous to Amazon if it owned Visa.

Alibaba is one of the best tech companies in the world headed by a former Chinese English language teacher in Hangzhou.

If America becomes too difficult or expensive with which to do business, Alibaba and Chinese tech will just recalibrate their strategy to deeper infiltrate the confines of Southeast Asia and the rest of the undeveloped world.

Any price war on undeveloped soil favors the Chinese as they have mastered scale better than anyone on the planet.

The stellar Alibaba numbers also mean the trade war has no end in sight as each player thinks they have the upper hand. But it also means the tech giants from both countries will come out unscathed and will lead their country’s respective equity markets higher for the foreseeable future.

________________________________________________________________________________________________

Quote of the Day

“Technology is nothing. What's important is that you have a faith in people, that they're basically good and smart, and if you give them tools, they'll do wonderful things with them,” – said Apple cofounder and former CEO Steve Jobs.