Mad Hedge Technology Letter

May 15, 2019

Fiat Lux

Featured Trade:

(TRUE COST OF THE CHINA TRADE WAR)

(EXPE), (TRIP), (GOOGL), (CTRP)

Mad Hedge Technology Letter

May 15, 2019

Fiat Lux

Featured Trade:

(TRUE COST OF THE CHINA TRADE WAR)

(EXPE), (TRIP), (GOOGL), (CTRP)

As the trade misunderstanding escalates to a new stratum of ferociousness, certain parts of the economy are ripe to be battered.

Tourism and in particular, international travel, will be one of the first luxuries to be sliced off consumers' list.

China’s most popular online travel agent Ctrip.com (CTRP) has suffered a damaging drop in demand from would-be international travelers.

Jonathan Grella, spokesman at the US Travel Association said, “The US runs a US$28 billion travel and tourism trade surplus with China” and preliminary numbers appear that Chinese travel to the US in the past year has dropped around 20%.

Compounding the woes is the weakening of the Chinese yuan which could become collateral damage from the trade negotiations if American and Chinese corporations repurpose supply chains to other countries and stop sending dollars to the mainland.

The ball is already rolling with 93 percent of Chinese companies considering making some changes to their supply chains to mitigate the effects of trade tariffs in an ingenious way to circumvent extra costs.

Of these, 18% are open to a complete supply chain remake and production transformation, with 58% making meaningful changes.

A further 17% plan to make minor tweaks in response to the trade war, with only 7% making no changes at all.

Chinese and American companies are reconsidering their Chinese manufacturing bases to avoid the tariffs placed on US$250 billion of Chinese exports by US President Donald Trump.

The unintended consequence will be a powerful surge in economic activity in South East Asia with also India benefitting from the chaos.

Apart from the supply chain complexities, the worsening of Chinese yuan strength could put a massive damper on Chinese international travel plans.

The annual Chinese international travel growth rate of 5.5% would be in dire straits translating into current travel demand rerouted to lower margin Asian countries such as Thailand, Vietnam, and Malaysia which are quite popular for budget travelers.

If lower sales do not manifest itself because tourists opt to forego expensive western countries, this demand will correlate into fewer dollars per traveler because of cheaper destinations which might force companies to double down on promotions to lure higher volume.

The same goes for American consumers who will be on the hook for the tariff-loaded consumer items that trickle onto our shores.

Decaying relations have already poisoned the US tourism sector that’s seen its growth flatline for the first time in 10 years.

And while only a small percentage of the 80 million visitors to the US in 2018 were Chinese, the potential for that segment’s growth remains robust.

Only 6 percent of Chinese citizens have passports signaling an imminent rise in outbound Chinese tourists that will reach 220 million by 2025.

The opportunity cost of these dollars migrating to other locations will be a kick in the teeth.

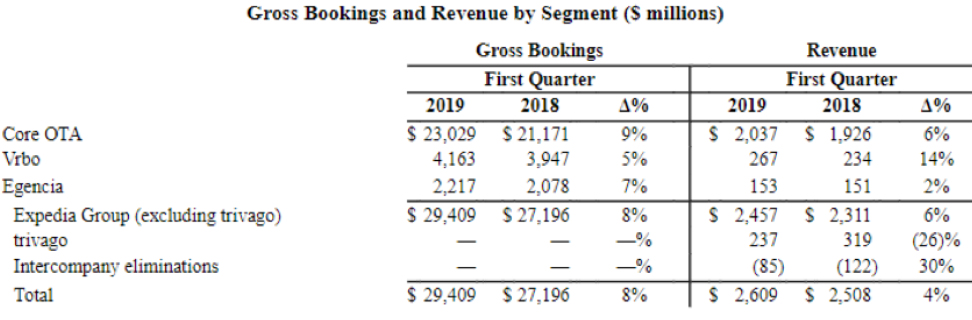

I reiterate my negative call for American online travel companies with recent damage control coming from TripAdvisor for last quarter’s debacle when the company reported dismal top-line results combined with a drop in monthly average unique visitors.

The company’s first-quarter revenues of $376 million missed badly up against the consensus forecast of $386.8 million.

TripAdvisor’s quarterly revenues fell 1% YOY as a result of the core hotel business underperforming and revenues from TripAdvisor’s Hotels, Media & Platform (or HM&P) showing zero growth at $254 million.

Revenues from its fringe businesses, which includes rentals, Flights/Cruise, SmarterTravel, and Travel China, plunged 33% to $42.

The proof is in the pudding with the company’s falling unique visitor count putting the kibosh on TripAdvisor’s growth prospects.

The company’s average monthly unique visitors cratered 5% YOY to 411 million users in the first quarter, contrasting with TripAdvisor’s performance last year when it reported an 11% YOY unique visitor growth.

Google is the boogie man in the equation with the company rolling out a more holistic travel product to integrate flight and hotel search functions while organizing people’s travel plans and saving research.

Alphabet will also repurpose more travel data on Google Maps, and integrate hotel and restaurant reservations for customers who are logged on.

Linking the Google travel and map functions seem like a no brainer to me and will be the precursor before the company starts selling ads on Google Maps including travel ads.

Google’s pivot into online travel marks an existential crisis for the incumbents and will strengthen its position in travel by driving further searches and potential higher-qualified leads for its partner companies, such as airlines and hotels.

Consumers have already recognized Google as the go-to place where to do travel research.

In a zero-sum game, Expedia (EXPE) and TripAdvisor (TRIP) will directly lose out.

Highlighting the erosion was Expedia’s super growth asset Vrbo whose gross bookings totaled $4.16 billion, up a paltry 5 percent from a year earlier.

The growth rate was less than half of the main online travel agency business which should sound off alarm bells.

As it stands now, Google generates referral traffic although it does process some bookings on its own site for other travel merchants.

Unlike travel agencies such as Expedia or Priceline, Google doesn’t directly sell travel products such as hotel rooms or airline tickets but that could change quickly.

This ties back to my continuing thesis of the low-value proposition of broker apps in the tech ecosystem, either there will be one with a monopoly, or a bigger fish will hijack their business model and become the new monopolistic dominator.

Such is the high stakes of Silicon Valley in 2019.

“Failure can teach you something, and as long as you're moving very, very quickly, you're going to start piling up the wins. Speed gives you the luxury to be able to fail.” – Said Current CEO of Uber Dara Khosrowshahi

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Hot Tips

May 14, 2019

Fiat Lux

The Five Most Important Things That Happened Today

(and what to do about them)

1) Trump and Xi to Meet on June 22. That means we have five more weeks of trade war agony until markets have a chance to recover. Sell in May? Whoever said that? Click here.

2) Apple Cellphones Made in China on New Tariff List. This should set up the best entry point of the year for Steve Jobs’ creation. Stock will soar when the tariff is listed. Click here.

3) Uber Dives 20% from IPO Price, in one of the worst IPOs in market history. $15 billion in market cap lost in the first two days. You knew this deal was in trouble when they let the drivers in.

4) Bitcoin Soars $1,000 on Stock Panic. It seems investors prefer Ponzi schemes to blue chip tech stocks these days. What’s wrong with cash? Click here.

5) China Tariffs to Cost US Households $500 Each, in rising import costs. Don’t point at me! I buy all American with my Tesla. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

(CHINA’S COUNTERATTACK)

(AAPL), (MSFT), (ADBE), (PYPL), (QCOM), (MU), (JD), (BABA), (BIDU)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

May 14, 2019

Fiat Lux

Featured Trade:

(CHINA’S COUNTERATTACK)

(AAPL), (MSFT), (ADBE), (PYPL), (QCOM), (MU), (JD), (BABA), (BIDU)

Global Market Comments

May 14, 2019

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

Ratcheting up the trade tensions, China is pulling the trigger on retaliatory tariffs on $60 billion worth of U.S. goods, just days after the American administration said it would levy higher tariffs on $200 billion in Chinese goods.

American President Donald Trump accused China of reneging on a “great deal.”

The mushrooming friction between the two superpowers gives even more credence to my premise that hardware stocks should be avoided like the plague.

I have stood out on my perch in 2019 and proclaimed to buy software stocks and if you need one name to hide out in then I would confidently choose Microsoft (MSFT).

Microsoft has little exposure to China and will be rewarded the most on a relative basis.

The last place you want to get caught out is buying hardware stocks exposed to China and Apple is quickly turning into the largest piece of collateral damage along with airplane manufacturer Boeing.

Remember that 20% of Apple’s revenue comes from China and Apple bet big to solidify a complex supply chain through Foxconn Technology Group in China.

When history is recorded, CEO of Apple Tim Cook not hedging his bets exposing Apple’s revenue machine could go down as one of the worst ever managerial decisions by tech management.

The forced intellectual property transfers in China from western corporations was the worst kept secret in corporate America.

Being an operational guru as he is, and the hordes of data that Apple have access to, this was a no brainer and Cook should have mitigated his risks by investing in a supply chain that was partially outside of China, and not incrementally spreading out the supply chain through other parts of Asia is coming back to bite him.

China's most recent tariffs will come into effect on June 1, adding up to 25% to the cost of U.S. goods that are covered by the new policy from China's State Council Customs Tariff Commission.

The result of these newly minted tariffs is that importers will probably elect to avoid absorbing the costs themselves and pass the price hikes to the consumer sapping demand.

The American consumer still retains its place as the holy grail of the American economic bull case, but this will test the thesis.

For the short term, it would be foolish to hang out to Chinese companies listed in New York through American depository receipts (ADR) such as JD.com (JD), Alibaba (BABA).

Baidu (BIDU) is a company that I am flat out bearish on because of a weakening strategic position versus Alibaba and Tencent in China.

Even with no trade war, I would tell investors to short Baidu, and the chart is nothing short of disgusting.

Wei Jianguo, a former vice-minister at the Chinese Ministry of Commerce who handled foreign trade, said to the South China Morning Post that “China will not only act as a kung fu master in response to U.S. tricks but also as an experienced boxer and can deliver a deadly punch at the end.”

It is clear that any goodwill between the two heavyweight powers has evaporated and the hardliners inside the communist party pulled all the levers possible to back out at the last second.

Many of us do not understand, but there is a complicated political game perpetuating inside the Chinese communist party pitting reformists against staunch traditionalists.

This is not only Chairman Xi’s decision and appearing weak on the global stage is the last concession the communist government will subscribe to.

Along with the iPhone company, semiconductor stocks will be ones to avoid.

The list starts out with the chip companies leveraged the most to Chinese revenue as a proportion of total sales including Qualcomm (QCOM) with 65% of revenue in China, Micron (MU) who has 57% of sales in China, Qorvo who has half of sales from China, Broadcom who has 48% of sales from China, and Texas Instruments rounding out the list with 43% of total revenue from China.

The first 5 months of the year saw constant chatter that the two sides would kiss and makeup and chip stocks benefitted from that tsunami of positive momentum.

The picture isn’t as pretty when you flip the script, and chip stocks could suffer a gut-wrenching summer if the two sides drift further apart.

After Microsoft, other software names I would take comfort in with the added bonus of strong balance sheets are Veeva Systems (VEEV), PayPal (PYPL), and Adobe (ADBE).

The new tariffs will burden American households to up to $2 billion per month going forward, and new purchases for discretionary items like extra electronics will be put on the back burner extending the refresh cycle and saddling chip companies and Apple with a glut of iPhone and chip inventory.

Buy software companies on the dip.