Mad Hedge Biotech & Healthcare Letter

March 4, 2021

Fiat Lux

FEATURED TRADE:

ARE WE THERE YET: HOW THE JNJ VACCINE COULD BE THE ANSWER

(JNJ), (MRNA), (PFE), (BNTX), (MRK), (SNY)

Mad Hedge Biotech & Healthcare Letter

March 4, 2021

Fiat Lux

FEATURED TRADE:

ARE WE THERE YET: HOW THE JNJ VACCINE COULD BE THE ANSWER

(JNJ), (MRNA), (PFE), (BNTX), (MRK), (SNY)

Since the pandemic started, we’ve had two extremely similar COVID-19 vaccines approved: the mRNA vaccines created by Moderna (MRNA) and Pfizer (PFE) / BioNTech (BNTX).

Now, there’s another coronavirus shot that gained FDA approval: Johnson & Johnson’s (JNJ) adenovirus jab.

In fact, JNJ’s candidate received a unanimous approval from the FDA—a first among the COVID-19 vaccine developers.

Results showed that JNJ’s shot has 66% effectivity at preventing coronavirus infections and 85% effective at blocking severe COVID-19 cases when allowed at least four weeks to take effect.

Taken at face value, the numbers from JNJ’s trials may not seem as impressive as the two-shot vaccines of Moderna or Pfizer, which both demonstrated efficacy results of over 94% in their 2020 reports.

However, it’s important to not make any conclusions based on incomplete data.

After all, drawing comparisons among different vaccine studies performed at different periods is practically comparing apples to oranges.

That’s why Dr. Anthony Fauci and other experts declared that they’ll just take whichever vaccine shot they could avail of.

Actually, the JNJ vaccine may be the ideal option for some people.

Since the JNJ vaccine shows less severe reactions compared to Pfizer and Moderna’s vaccines, this could be preferable for people who couldn’t tolerate the side effects.

Although the side effects of Pfizer and Moderna are temporary, some people need to take days off to recover. Sadly, not everyone has the luxury to do that.

The fact that it’s a single jab vaccine makes it an attractive option for young and healthy individuals, who can’t afford to go back to get a second shot.

It’s also less fragile and can be stored in a regular fridge for three months without the need for any hyper-cold storage system like the mRNA vaccines require. This would make it an attractive option for rural areas.

Plus, JNJ tested its candidate at the height of the pandemic. That means the numbers the company released could have been affected by the situation at the time.

Although JNJ’s vaccine does not completely get rid of the disease, it delivers on the promise of protecting the patients from the worst possible scenarios of COVID-19: hospitalization and death.

Basically, the JNJ vaccine is cheap to manufacture as well as pretty simple to administer and get.

People can get some dependable viral protection within a span of four weeks, without the need to return for a second jab.

As a bonus, the JNJ vaccine could even protect you better from the new variants that are starting to spread fast.

Despite the $410 billion market capitalization of JNJ though, it looks like the New-Jersey-based giant isn’t up for the massive rollout the world expects from its vaccine.

This is where Joe Biden steps in.

With the goal of having every American vaccinated by the end of May, Biden tapped Merck—a fierce rival of JNJ—to help out with the production.

While Merck’s own COVID-19 vaccine program was shut down, this company remains the leading vaccine developer across the globe.

This means it knows a thing or two about fast-moving mass production during outbreaks—and this is exactly the kind of expertise JNJ needs.

If things work out, JNJ should be able to produce 94 million doses by the end of May—roughly 7 million doses ahead of what’s stipulated in its contract—and the full 100 million by June.

This arrangement isn’t anything new. Since the COVID-19 pandemic, competitors have been joining forces to find ways to put an end to the crisis.

In January this year, Sanofi (SNY) announced that it would be collaborating with BioNTech to help manufacture additional doses of the COVID-19 vaccine it developed with Pfizer.

When JNJ receives authorization from the EU as well, Sanofi would also be there to help with the production.

The JNJ vaccine could just be the escape hatch we’ve all been waiting for since the pandemic started.

With this FDA authorization, we’d be able to vaccinate millions more at a breakneck speed.

Global Market Comments

March 4, 2021

Fiat Lux

Featured Trade:

(THE BARBELL PLAY WITH BERKSHIRE HATHAWAY),

(BRKA), (BRKA), (BAC), (KO), (AXP), (VZ), (BK) (USB),

(TLT), (AAPL), (MRK), (ABBV), (CVX), (GM), (PCC), (BNSF)

It’s time to give myself a dope slap.

I have been pounding the table all year about the merits of a barbell strategy, with equal weightings in technology and domestic recovery stocks. By owning both, you’ll always have something doing well as new cash flows bounce back and forth between the two sectors like a ping pong ball.

After all, nobody gets sector rotation right, unless they have been practicing for 50 years, like me.

Full disclosure: I have to admit that after 50 years of following him, I love Buffet. He was one of the first subscribers to my newsletter when it started up in 2008. Some of his best ideas have come from the Mad Hedge Fund Trader, like buying Bank of America for $5 in 2008.

Oh, and he hates Wall Street for constantly fleecing people. Ditto here.

In reading Warren Buffet’s annual letter (click here for the link), it occurred to me that his Berkshire Hathaway (BRKB) shares were in effect a one-stop barbell investment.

For a start, Warren owns a serious slug of Apple (AAPL), some $120 billion worth, or 2.5% of the total fund. That gives (BRKB) some technology weighting. It cost him only $20 billion. The dividends he received entirely paid for the initial cost. So he owns 4% of Apple for free.

I remember the battle over the initial “BUY” five years ago. Warren fought it, insisting he didn’t understand the smart phone business. In the end, he bought Apple for its global brand value alone.

That is Warren Buffet to a tee.

The next five largest publicly listed holdings are Bank of America (BAC), Coca-Cola (KO), American Express (AXP), and Verizon Communications (VZ). These are your classic domestic recovery sectors. And with a heavy weighting in other banks (BK) (USB), Buffet is effectively short the bond market (TLT), another position I hugely favor.

Also included in the package is a liberal salting of pharmaceuticals, Merck (MRK) and AbbVie (ABBV). He has a small energy weighting with Chevron (CVX). He even has a position in old heavy metal America with General Motors (GM).

Berkshire is also one of the world’s largest property & casualty insurance owners. Its current “float” is $138 billion. You all know his flagship holding, GEICO. And the gecko mascot isn’t going anywhere as long as Warren lives. It was Warren’s idea.

It all seems to work for Warren. In 2020, he earned a staggering $42.5 billion. All told, Berkshire’s businesses employ 360,000, second to only Amazon (AMZN), and is the largest taxpayer in the United States, accounting for 3% of government revenues. Berkshire is also the largest owner of capital goods & equipment in the US worth $156 billion, topping (AT&T).

Many of Warrens's early 1956 $1,000 investors are millionaires many times over….and over 100 years old, prompting him to muse if ownership of his shares extended life.

Warren’s annual letter, which he spends practically the entire year working on, is always one of the best reads in the financial markets. There isn’t a better 50,000-foot view out there. He also admits to his mistakes, such as his disastrous purchase of Precision Castparts (PCC) in 2016 for $37 billion, which later suffered from the crash in the aerospace industry. In 2020, Buffet wrote off $11 billion of that acquisition.

He can do worse. In 1993, he bought the Dexter Shoe Company for $433 million worth of Berkshire stock. The company went under, but the Berkshire stock today is worth $8.7 billion.

Buffet’s letters always refer back to some of his “greatest hits,” today legends in the business history of the United States: GEICO, Furniture Mart, Berkshire Hathaway Energy, and See’s Candies, one of the largest employers of women in the US using 150-year-old recipes. Its peanut brittle is to die for.

In 2009, Buffet snatched away from me BNSF for a song, now the most profitable railroad in the country, an amalgamation of 360 railroads over 170 years. I say “snatched away” because it was my favorite railroad trading vehicle for decades until he bought the entire company. I hear its trains run by my home every night as a grim reminder.

Another benefit to owning (BRKB) is that Buffet is far and away the largest buyer of his own shares, soaking up $25 billion worth in 2020. And he is buying the shares of other companies that are also aggressively buying their own shares, like Apple ($200 billion with last year). It all sounds like the perfect money creation machine to me.

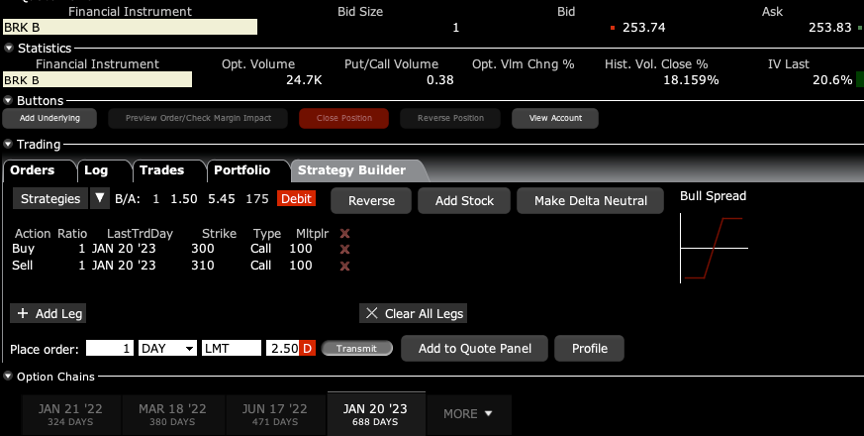

It gets better. Berkshires “B” shares trade options, meaning you can buy LEAPS (Long Term Equity Anticipation Securities), which by now, you all know and love. I’ll run some numbers for you.

With (BRKB) now trading at $254, you can buy the January 2023 $300-$310 call spread for $2.50. If the shares close anywhere over $310 by the 2023 expiration, the position will be worth $10.00, giving you a gain of 300%. And you only need an appreciation of $56, or 22% in the shares to capture this blockbuster profit, giving you upside leverage of an eye-popping 13.63X in the best run company in America.

See, I told you you’d like it.

This is how poor people become rich. In fact, my target for (BRKB) is $300 for end of 2021 and $400 for 2022, right when the two-year LEAPS expire.

One question I often get about Berkshire is what happens when Warren Buffet goes to his greater reward, not an impossible concept given that he is 90 years old.

I imagine the shares will have a bad day or two, and then recover. Buffet has been hiring his replacements for a decade or more, and he handed off day-to-day operation years ago (I didn’t want to move to Omaha, no mountains).

When that happens, it will be the best buying opportunity of the year. And another chance to load up on those LEAPS.

Mad Hedge Biotech & Healthcare Letter

February 23, 2021

Fiat Lux

FEATURED TRADE:

(IS THIS THE YEAR OF BIOTECH UPSTARTS?)

(PFE), (GSK), (MRK), (SNY), (MRNA), (BNTX), (NVAX), (AZN)

Vaccines have long been shoved to a sleepy little corner of the biopharmaceutical world, ruled over by a handful of companies that cater to billions of dollars’ worth of demand for vaccines every year, undisturbed by newcomers.

However, the COVID-19 pandemic has made this particular corner of the industry a tad more crowded.

While there’s still no clear picture of how the next stage of the efforts to vaccinate the majority of the human population against COVID-19 will work out, what’s evident is that the dominance of the “big four” publicly-traded vaccine developers will be challenged.

That means the battle for supremacy in the vaccine market will no longer be confined within Pfizer (PFE), GlaxoSmithKline (GSK), Merck (MRK), and Sanofi (SNY).

As we’ve witnessed, the COVID-19 pandemic has provided entry points for new names in the industry, such as Moderna (MRNA), BioNTech (BNTX), and Novavax (NVAX).

By the second half of 2021, Novavax and its partners are targeting to supply 150 million doses of their vaccine, while Moderna says it would be distributing at least 600 million doses this year alone—a number that could reach a billion given the right partners in the future.

Those numbers are on par with global-level vaccine production—with Novavax and Moderna quickly gaining steam and catching up with the big players in the industry.

For context, Sanofi made 250 million doses of its own flu vaccine for the 2021 flu season.

Given that Novavax also plans to release its own flu vaccine combined with the smaller company’s momentum, Sanofi is looking at a long-term rival in this sector.

Aside from offering these smaller biotechs opportunities for growth in terms of business, the pandemic has fast-tracked the advent of next-generation technologies in the industry.

Both Pfizer and Moderna have been approved to use the pioneering messenger RNA technology to develop their COVID-19 vaccine candidates.

Apart from mRNA technology, a similarly revolutionary approach is being explored by Johnson & Johnson (JNJ): viral vector technology.

Meanwhile, AstraZeneca (AZN) and its partner Oxford University came up with their own viral vector vaccine, which has been approved in Europe.

As for Novavax, this Maryland-based company has decided to use the more conventional approach utilizing a protein subunit vaccine.

Although the exact size of the COVID-19 market is difficult to predict, it’s safe to say that it will be massive.

In terms of who could eventually get the lion’s share of the market, Pfizer is currently leading at the moment based on the government contracts the company managed to secure.

Pfizer estimates $15 billion in revenue from the COVID-19 vaccine in 2021—a number that’s two and a half times higher than its best-selling drug in 2020.

Moderna projects at least $10 billion in COVID-19 vaccine sales, while Novavax anticipates roughly $3.4 billion this year.

In the future though, there’s strong indication that AstraZeneca and JNJ will be vying for dominance for mass-market contracts. This is primarily because of their one-dose vaccine promise and the convenient storage requirements their candidates offer.

Another massive growth prospect for this vaccine is if the need for yearly boosters sticks around. This market would not only be lucrative for smaller companies like Novavax and Moderna, but even for the bigger vaccine players.

Considering the potential of this market, the current leaders of the COVID-19 vaccine race shouldn’t get too comfortable.

In fact, Sanofi and GlaxoSmithKline have already joined forces to create their own COVID-19 vaccine candidate.

So while Pfizer, Moderna, and AstraZeneca already have their products out the door, other vaccine developers still consider themselves in the running to topple them from their perch.

Mad Hedge Biotech & Healthcare Letter

February 18, 2021

Fiat Lux

FEATURED TRADE:

(WARREN BUFFETT’S BIOPHARMACEUTICAL BETS)

(MRK), (ABBV), (BMY), (PFE), (NKTR), (VZ), (CVX), (AAPL), (BRK.B)

Aside from the recent big moves involving Verizon Communications (VZ), Chevron (CVX), and Apple (AAPL), Warren Buffett has also been busy with biopharmaceutical stocks.

Just before 2020 ended, Berkshire Hathaway (BRK.B) made notable changes in its positions particularly in Merck (MRK), AbbVie (ABBV), Bristol-Myers Squibb (BMY), and Pfizer (PFE).

Berkshire boosted its investment in Merck by 28.1% to reach 28.7 million shares.

Meanwhile, its AbbVie holdings were increased by 20% to hit 25.5 million shares.

It also added 11.2% in its investments in Bristol, totaling to 33.3 million shares.

In contrast, the company cut 3.7 million shares from its Pfizer holdings.

In terms of growth potential, these biopharmaceutical companies hold the most promising prospects in the next decade.

Merck, hailed as a vaccine stalwart, is behind the blockbuster cancer treatment Keytruda.

For context, Keytruda generated $14.4 billion in sales in 2020 alone.

Despite fears over the expiring patent exclusivity of this drug, the company still trades at roughly 11.5 times earnings and is actually projected to achieve 11% long-term EPS growth rate.

Merck also continues to leverage Keytruda in the development of the next generation of treatments in its pipeline.

In fact, the company recently sealed a clinical collaboration with Nektar Therapeutics (NKTR) to assess the effectiveness of Keytruda when combined with Nektar’s own bempegaldesleukin in the treatment of squamous cell carcinoma.

Other than expanding its oncology sector, Merck has been developing its animal health business as well. So far, this particular segment has grown by 7% year over year, reaching $4.7 billion in 2020.

If things work out, then Merck could emerge as a huge competitor against Pfizer’s own animal healthcare spinoff, Zoetis (ZTS), in the future.

To date, Merck has at least 31 candidates in Phase 2 trials and 25 more undergoing Phase 3 studies.

Needless to say, these will be valuable in enriching the company’s lineup especially with the challenges that Keytruda will face in the next years.

As for AbbVie, this company trades at approximately 8.3 times the earnings estimated in the next 12 months. This is well below its five-year average of 10.4 times earnings.

However, the company is projected to show at least 13% EPS growth rate in the long term.

Despite the challenges of 2020, with the company going down 2.6%, the long-term prospects for AbbVie remain positive.

Although AbbVie broke through the dermatology market following its acquisition of Botox-maker Allergan in the past year, it still has to contend with a major problem: arthritis medication Humira.

Humira is not only AbbVie’s top-selling treatment but also the best selling drug in the world today.

In 2020 alone, this anti-inflammatory treatment raked in $19.8 billion in sales. However, AbbVie might soon lose this edge since its exclusive rights to Humira in the US will expire in 2023.

Amidst the anxiety over this issue though, AbbVie continues to defy expectations.

Last year, the company reported a 65.9% growth in its net revenue despite the overall slowdown caused by the pandemic.

As for 2021, AbbVie is anticipating an even better year thanks to its portfolio diversification efforts.

To date, the company’s lineup now spans neuroscience, immunology, eye care, women’s health, and of course, aesthetics.

Meanwhile, Bristol Myers has been pegged to achieve roughly 8% growth rate in the long term. Right now, the stock trade at 7.9 times earnings estimated over the next 12 months.

Like AbbVie and Merck, Bristol has been dealing with patent expiration issues—a problem that pushed its stock down by 4.1% so far this year.

One of the major updates involving Bristol is its massive $74 billion acquisition of Celgene in 2019.

While the deal raised a lot of eyebrows at the time, it brought cancer blockbuster Revlimid into the company’s fold.

Revlimid, which still enjoys protection from a flood of generics for a few more years, has been pumping up sales for Celgene nonstop for over a decade. The drug is expected to generate the same, if not higher, profits for Bristol.

Two more blockbuster drugs in Bristol’s lineup are facing impending patent exclusivity issues, Opdivo, which would expire in 2028, and Eliquis in 2026.

Nonetheless, the positives outweigh the negatives for Bristol. After all, this company invested so much in diversification.

Sales of Opdivo, Revlimid, and Eliquis continued to trend upwards last year.

Opdivo alone managed to generate $7 billion in annual revenue, prompting Bristol to expand the indications for this product.

However, the more promising news lies in the updates that the recently launched products, like multiple sclerosis drug Zeposia and anemia treatment Reblozyl, are gaining traction in the market.

Thanks to the development of its pipeline, the company expects that its new product lineup would account for roughly 27% of its total revenues by 2025.

Overall, Berkshire’s choice of biopharmaceutical companies are offering promising growths in the next several years despite the setbacks they are facing today.

While some investors get alarmed over negative updates, it looks like the Oracle of Omaha is following his own advice: “Whether we're talking about socks or stocks, I like buying quality merchandise, when it is marked down.”

Mad Hedge Biotech & Healthcare Letter

February 2, 2021

Fiat Lux

FEATURED TRADE:

(2021: GILEAD SCIENCES’ YEAR OF MILESTONES)

(GILD), (NVAX), (JNJ), (MRK)

Stocks are tumbling on the back of substandard vaccine updates, with investors growing more wary of the whole COVID-19 vaccine narrative.

January ended with Novavax (NVAX) announcing that its COVID-19 vaccine candidate is roughly 90% effective, but doesn’t work as well against other more contagious strains in South Africa.

Johnson & Johnson (JNJ) reported that its candidate is only 66% effective at stopping moderate to severe strains of the coronavirus, but is 100% effective in preventing hospitalizations and even death 28 days after it gets administered.

However, the real kicker is Merck’s (MRK) decision to completely drop out of the COVID-19 vaccine race when both its candidates showed disappointing results in the early stages.

This is disappointing news considering that Merck is one of the biggest vaccine developers in the world today.

Nonetheless, Merck’s still not out of the COVID-19 race yet as it appears to be following the lead of Gilead Sciences (GILD) instead.

That is, it plans to focus on developing COVID-19 treatments in the hopes of benefiting from it the same way Gilead did in the past months.

Since the pandemic started, Gilead has been at the forefront of the fight – so much that its COVID-19 treatment, Remdesivir, is evidently having a major impact on the company’s top line.

In its third-quarter earnings report in 2020, Gilead reported $6.6 billion in total revenue, showing off a 17% jump from its performance during the same period last year.

If you exclude its COVID-19 sales, Gilead would have only earned $5.6 billion, with the increase in its year over year performance changing from 17% to just 2%.

As for its overall performance in 2020, Gilead announced that it’s raising its previous guidance from the $23 billion and $23.35 billion range to be somewhere between $24.3 billion and $24.35 billion.

This new guidance indicates a 10% year over year growth, but without Remdesivir, its product sales would actually show a slight decline compared to 2019.

Outside Remdesivir, Gilead has been active in searching for additional growth drivers.

So far, the most promising segment is its HIV lineup led by its top-selling product, Biktarvy, also known as "the gold standard in HIV treatment."

In the third quarter of 2020, sales of Gilead’s HIV line climbed by 8% to reach $4.5 billion.

While generic competition has entered the market, Biktarvy is expected to continue to gain steam in 2021.

Another catalyst in its HIV line is the drug Lenacapavir, which can either be developed as a twice-a-year injection or a weekly pill.

If successful, Lenacapavir can bring an additional $9 billion in revenue for Gilead.

Aside from HIV, Gilead has also been working toward becoming a leader in the oncology sector.

To achieve this, the company spent $21 billion for the acquisition of Immunomedics.

Specifically, Gilead bought the New Jersey-based company for its new breast cancer treatment, Trodelvy.

Gilead’s massive bet on Trodelvy raised a lot of eyebrows, but the product offers a very real chance for an enormous payoff for its shareholders.

Trodelvy lowers the risk of death among breast cancer patients by an impressive 52% when compared to those who receive standard care.

Annually, Trodelvy is estimated to rake in at least $1.8 billion in revenue for Gilead --- and that’s only for breast cancer application.

Gilead also intends to expand Trodelvy’s application to include more complex fields of oncology and even for some viral diseases.

Beyond its COVID-19 program, Gilead has an impressive portfolio of diverse assets that the company is focused on developing.

It currently has 42 clinical programs queued in its pipeline and at least a handful of these are anticipated to become steady sources of revenue.

As expected, it spent 2020 acquiring the necessary partners for its big picture plans, making 2021 a year of milestones for the company.